How high will interest rates go and what will your mortgage be?

Australia is in a precarious position as inflation expectations soar and forecasts predict a very worrying sign for mortgages. It’s not all bad news though.

ANALYSIS

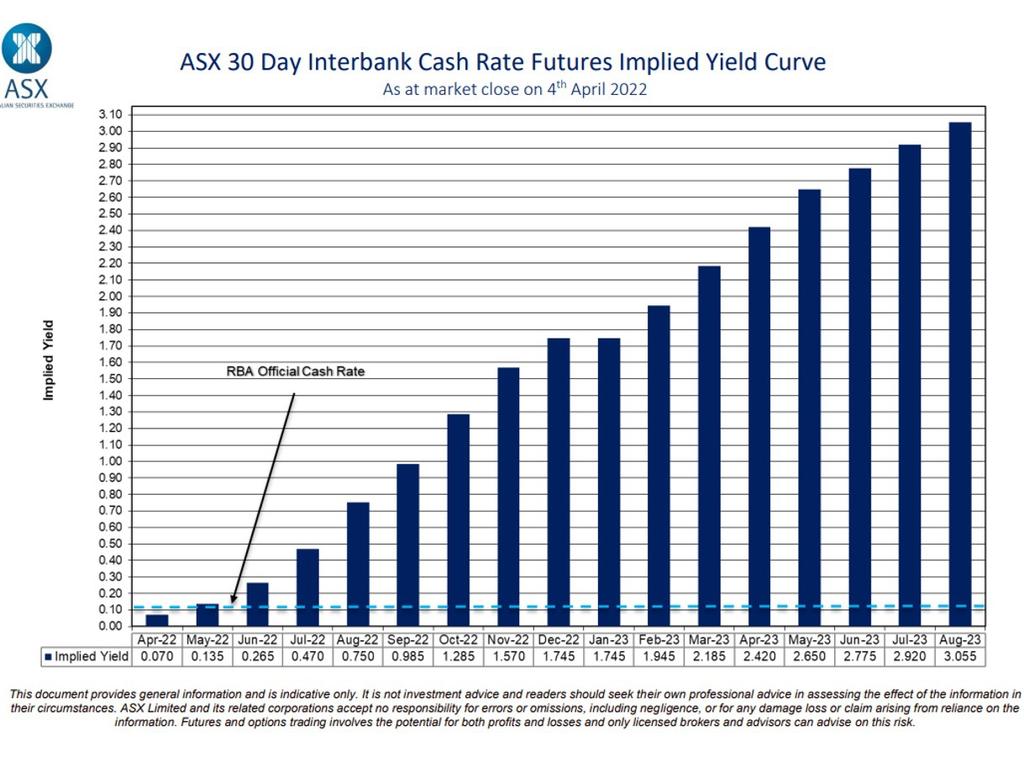

With Australian inflation expectations soaring on the back of higher petrol prices, futures markets have ramped up their forecasts for Australian interest rates.

The latest futures market forecast has the Reserve Bank of Australia (RBA) lifting the official cash rate (OCR) from June 2022, with the cash rate to rise to 1.75 per cent by the end of this year and 3 per cent by August 2023.

The OCR is currently at a record low 0.1 per cent. Therefore, a 2.9 per cent increase by August 2023 would be the equivalent of 12 interest hikes in only 16 months.

Read tips to help assess your home loan payment capability on Compare Money >

Interest rate forecast would devastate household finances

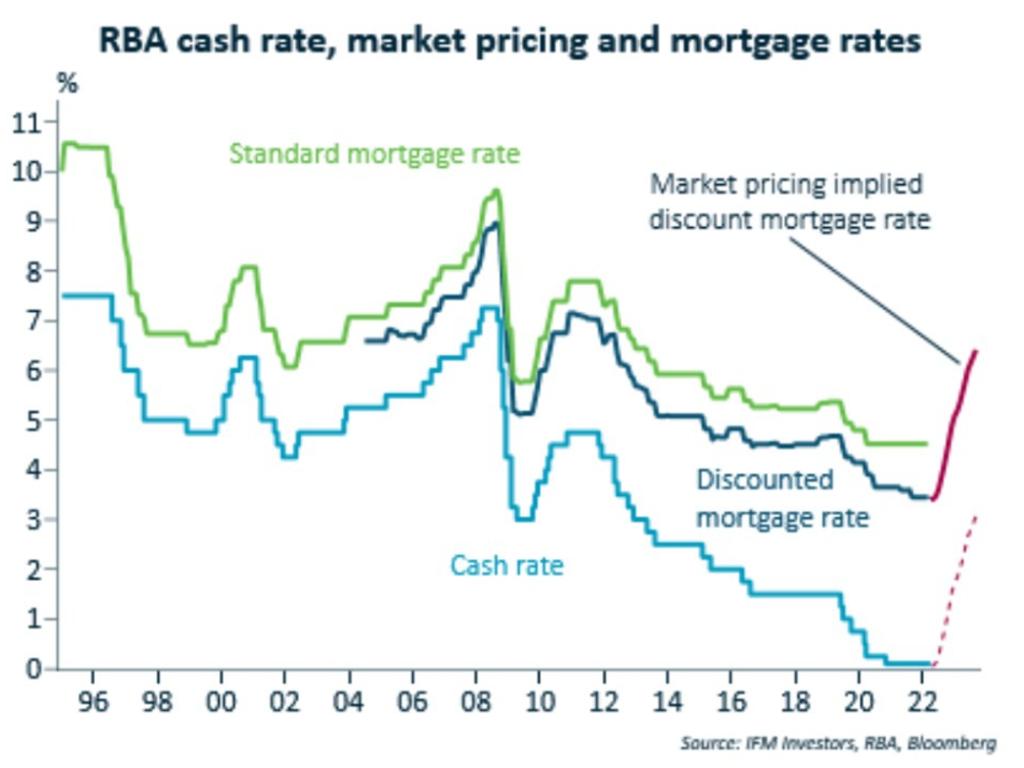

Assuming the futures market’s OCR projection was passed on in full to mortgage holders, the average discount variable mortgage rate would soar from 3.6 per cent currently to around 6.5 per cent by August 2023.

Such a large and sharp increase in mortgage rates would devastate household finances, potentially crashing the housing market and pushing the economy into recession.

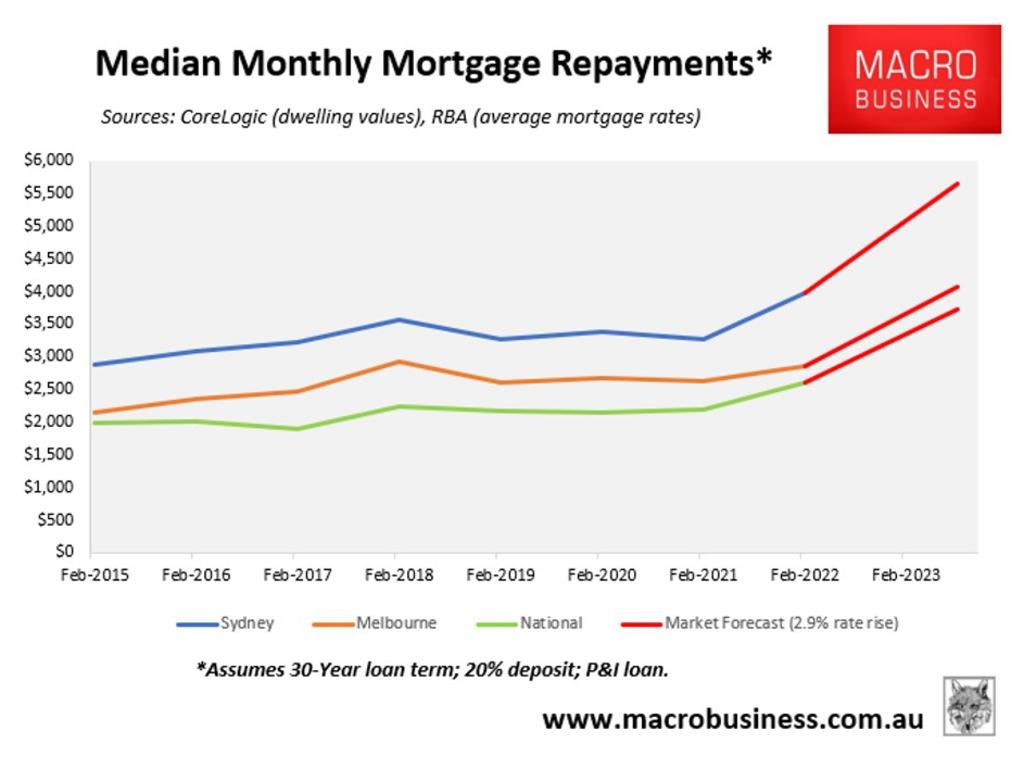

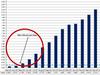

To illustrate why, consider the next chart showing the average monthly repayment on a median-priced dwelling across Sydney, Melbourne and nationally, assuming a 30-year principal and interest mortgage and a 20 per cent deposit.

If the discount variable mortgage rate was to rise by 2.9 per cent to 6.5 per cent, as predicted by the futures market, then mortgage repayments would lift by 39 per cent from their current level.

This would see monthly mortgage repayments on the median priced Australian home rise from $2688 in March 2022 to $3737 – an increase of $1049.

For the median Sydney buyer, median monthly repayments would rise by a whopping $1585, whereas they would rise by $1143 in Melbourne.

I doubt the typical Australian borrower could cope with $12,500 of extra mortgage repayments a year without experiencing severe financial distress.

Luckily the futures market is wrong on interest rates

The good news is that the lever for interest rates is held by the RBA, not the markets. And there is little reason why the RBA would lift rates as aggressively, thereby engineering an unnecessary house price crash or recession.

My prediction is that the tightening cycle will be far shallower – i.e. circa 1 per cent – for the simple fact that Australian households are so indebted and sensitive to small rate rises.

Even a 1 per cent lift in mortgage rates would see median monthly mortgage repayments rise by 13 per cent or $343, with Sydney buyers facing a larger $518 per month increase in median mortgage repayments.

It is also worth pointing out that interest rates are a demand management tool. Given Australia’s current inflationary pressures are mostly imported, including via petrol prices, there is little sense in the RBA hiking rates aggressively to counter imported (cost-push) inflation. Such a strategy would hammer the economy without relieving the very forces driving the inflation problem in the first place.

For these reasons, the market’s latest interest rate projections are far too heroic and detached from reality.

Such a rapid increase in mortgage repayments would crash the housing market and economy, which is exactly why the RBA is unlikely to raise rates as swiftly nor as far as the market is predicting.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

‘Rush of blood’: Gloves off in election debate

The two men battling for control over Tasmania have taken the gloves off immediately in a furious Sky News election debate.

Aussie shares crack fresh record high

The Australian sharemarket lifted to a fresh record high on Tuesday as investors followed gains on Wall St.

Aussies’ confidence rocked by shock RBA call

The country’s major banks say Australian consumer confidence was rocked after the RBA decided against cutting the official cash rate in July.