Trading Day: ASX drop wipes $56bn off market amid global growth fears

Investors wiped $56bn off the stock exchange in what was the worst one-day fall since February last year.

- Employment jump spurs $A rise

- Chinese slowdown hits Blackmores

- Pluto shutdown dents Woodside profit

- Telstra profit down 40pc

- Wall St plunges on recession fears

That’s it for the Trading Day blog for Thursday, August 15. The Australian market clocked its worst fall since February 2018, with more than $56 billion in value wiped off the bourse after a warning sign on the US economy.

Disappointing results from Telstra, Orora and Woodside added to the pressure, while reports from QBE, Super Retail, Treasury and Blackmores were also in focus.

Here’s how they were faring in lunchtime trading. Meanwhile the ABS has released better than expected unemployment data for July, spurring a rise in the Aussie dollar.

Samantha Bailey 4.29pm: ASX clocks worst fall in 18 months

Investors wiped $56 billion off the stock exchange on Thursday in what was the worst one-day fall since February last year, as markets reacted to warnings signs of a US recession.

An early drop was extended after stronger-than-expected July employment data dampened hopes of another rate cut this year.

Weakness in markets globally followed an inversion of the US Treasury yield curve, a possible warning sign of a recession, which spooked US markets overnight.

The Dow Jones Industrial Average fell 3.05 per cent in its biggest one-day drop since October, while the S&P 500 dropped 2.93 per cent and the Nasdaq lost 3.02 per cent.

The ASX was the worst-performing index in the Asia-Pacific, with the Shanghai Composite down only 0.38 per cent, and the Hang Seng actually edging up 0.2 per cent as the ASX ended the day. Japan’s Nikkei ended the session down 1.08 per cent

Stocks fell across all sectors but energy stocks suffered the heaviest falls, dropping 5.3 per cent, followed by tech stocks, which were down 4.9 per cent, and industrials, which fell 3.1 per cent.

BHP lost 2.8 per cent to $36.39 while Rio Tinto turned down 2.7 per cent to $85.60. Fortescue lost 0.8 per cent to $7.50.

In financials, Westpac fell 3.2 per cent to $27.61 while NAB gave back 3.1 per cent to $26.80. Commonwealth Bank slid 3 per cent to $74.34 while ANZ weakened 3 per cent to $26.23.

AUDUSD finished 0.5pc higher to US67.81c.

Bridget Carter 4.28pm: More staff departures at Deutsche

Dataroom | Fresh from mass redundancies due to the closure of its global equities business, further staff departures have been made at Deutsche Bank in Australia and Hong Kong in recent days, with a significant number of executives in its corporate finance team said to be staging an exit.

It comes with the bank believed to be planning to recut the size of its corporate finance team in Australia.

Up to six staff investment bankers within the Australian corporate finance team have left in the past week, while the number departing the corporate finance division in Hong Kong is said to be as many as 20 staff.

It comes after last month, Deutsche unveiled a dramatic global downsizing that is understood to have cost the jobs of about 50 Australian workers at the bank that became the fourth large bank to quit the domestic share trading market in six years.

Affected in the last round of cuts were the areas of equities trading, sales, research and those managing equity capital markets deals including floats of the Australian Securities Exchange.

The bank says it remains committed to corporate finance and the Australian market.

4.14pm: Stock slide extends at close

The Australian market has logged its worst day since February 2018, as fears of stalling global growth prompted a $57 billion sell-off.

A weak lead from the US prompted an early 2 per cent drop, while better-than-expected labour data dialled back rate cut bets and prompted further selling in the market.

At the close of trade, the benchmark ASX200 was 187.8 points or 2.85 per cent lower to 6408, just shy of its intra-day lows of 6405.6.

Meanwhile, the All Ords shed 187 points or 2.8pc to 6490.8.

Ben Wilmot 3.54pm: Vicinity REIT far from safe haven status

The Australian real estate investment trust sector is sometimes seen as a safe haven during periods of market volatility but the tough times for shopping centre landlords mean there is little respite in the area.

Vicinity dipped yesterday after turning in a below consensus result with funds from operations at the lower end of its guidance range and dumping plans for a $1 billion wholesale fund.

Today, the trust’s units were off by 1.4 per cent to $2.445, as part of the market rout.

Citi said the result highlighted a number of the headwinds facing retail landlords. With an overhang of about $11 billion worth of assets potentially for sale it said the decision not to pursue disposals was not overly surprising.

Citi expects retail to continue to surprise the market on the downside, as it has offshore, and has a neutral on Vicinity and sells on all the other retail REITs.

Eli Greenblat 3.31pm: Target restructure to cut 80 jobs

Target will make 80 positions at its head office redundant as part of a new strategy that will see it move upmarket by offering better quality clothing, fashion and home furnishings to put some distance between it and the discount department store sector.

Target will be repositioned over the next two to three years to represent a more quality product offer that offers value rather than simply heavy discounting and bargain-basement prices.

Staff at Target began to attend briefings this morning, The Australian can report, where they were informed about the corporate restructure that will see large changes across key management roles in buying, sourcing, marketing and other head office roles.

It will see 80 corporate roles made redundant. There will be an attempt to redeploy staff to other parts of the retailer and its parent company, Wesfarmers.

WES last down 3.33pc to $37.70.

3.27pm: IPH completes Xenith IP buy

IPH has completed its $192 million acquisition of Xenith IP Group, creating an intellectual property goliath comprising 1,000 people across 27 offices in eight Asia-Pacific countries.

The acquisition of Xenith means Glasshouse Advisory, Griffith Hack, Shelston IP and Watermark are now part of IPH, joining Spruson & Ferguson, Pizzeys, AJ Park and Practice Insight.

The combined brands account for 40 per cent of all patent filings in Australia, including about 25,500 in 2018.

IPH successfully wrestled Xenith away from suitor QANTM Intellectual Property with what was initially a hostile takeover.

It was IPH’s eighth and biggest acquisition since Spruson & Ferguson created the holding company to list on the ASX in late 2014.

IPH chief executive Andrew Blattman said “IPH’s unique scale, experience and presence across Asia-Pacific” would serve clients across the region and provide enhanced career opportunities for staff.

As part of the acquisition, Xenith chief executive Craig Dower is leaving the business, effective on Thursday.

IPH shares are down 1.89 per cent to $8.29 in afternoon trade, outperforming the market’s 2.7pc slump.

Sarah-Jane Tasker 2.54pm: Blackmores profit hit by China fail

Blackmores’ chief financial officer Aaron Canning says the company’s fall in profit is disappointing, blaming a failure to execute on its China strategy.

The Australian-listed vitamin maker reported today that its full-year profit fell 23.6 per cent to $53.5 million, driven by a drop in sales to China.

Shares in the company are down 7.5 per cent at $76.99 following the release of the results.

Mr Canning, who reported the results today following former CEO Richard Henfrey’s shock departure in March, said sales in the China segment were down 15 per cent as regulatory changes meant Chinese consumers shifted from Australian retailers to local sellers.

He said the changes to Chinese e-commerce laws, which came into effect from January 1, saw Blackmores’ export channel via daigous shrink by about 40 per cent.

Ben Wilmot 2.43pm: Analysts mixed on Dexus results

Office property specialist Dexus turned in strong results yesterday, flagging a near $10 billion pipeline of projects to set it up for coming years.

JPMorgan analysts said the business was in good shape, but the prospect of lower demand as the economy slowed increased the risks to the office cycle in Sydney and Melbourne.

The analyst warned there was the potential for net effective rents to decline as it kept its neutral rating and trimmed its price target by 90c to $12.75.

Dexus was down by 1.36 per cent to $13.04 in early afternoon trade.

But UBS analysts liked the result, saying that they viewed the trust’s guidance for this year as conservative as office markets were strong, the group had locked in trading profits and low debt costs would continue to provide a tail wind.

UBS lifted its price target by 7 per cent to $12.90.

2.32pm: Jobs jump won’t delay RBA: AMP

The sharemarket is fretting but the strong July jobs data won’t delay RBA rate cuts according to AMP Capital’s Shane Oliver.

While the RBA’s back-to-back rate cuts, tax refunds and strong infrastructure investment should help limit the rise in unemployment to around 5.5 per cent, Dr Oliver says they are unlikely to be enough get unemployment down to the 4.5 per cent or less needed to see stronger wages growth and higher inflation.

In the meantime the risks of even slower global growth on the back of the escalating US-China trade war are rising as indicated by falling share markets and bond yields racing to zero and below.

“As a result we remain of the view that the RBA will have to cut rates further and see the next 0.25pc cut coming next month followed by another cut in November ultimately taking the cash rate down to 0.5 per cent,” he says.

The Australian dollar rose and shares fell as the jobs data reduced the market-implied chance of further RBA cuts this year.

Aust jobs +41.1k in July with 34.5k full time, but rising participation keep unemployment rate at 5.2%... pic.twitter.com/zTdqsiwI0P

— Shane Oliver (@ShaneOliverAMP) August 15, 2019

Eli Greenblat 2.29pm: Super Retail leads market gainers

Super Retail Group, whose chains include Supercheap Auto, BCF, Macpac and Rebel, is the best performing stock on the S&P/ASX 200 this afternoon with the retailer’s shares up more than 6 per cent on a day when most shares are slumping.

Super Retail was up 6.2 per cent this afternoon at $9.22 after it released its full-year result that showed strong sales and profits at a time when the retail sector is hurting from a downturn in spending and some of the worst trading conditions in decades.

The company posted an 8.6 per cent rise in full-year net profit to $128.3 million as sales lifted 5.4 per cent to $2.57 billion. Pre-tax earnings increased 7 per cent to $314.7m.

On its trading outlook and performance for the first six weeks of fiscal 2020, analysts said same store sales growth for the BCF business was very strong at 5 per cent, although EBIT conversion is unclear.

Meanwhile, Auto division sales growth of 3 per cent, cycling a comparable of 5 per cent, indicates the resilience of that Supercheap Auto business.

Andrew White 2.19pm: Volatility a boon for ASX

Rising geo-political tensions and financial market volatility have been a boon for the ASX, fuelling trading volumes across its products and highlighting the relatively positive image of Australia volatility.

ASX chief executive Dominic Stevens said the economy was benefiting from looming surpluses in trade, the Federal Budget and the current account, as well as having low rates, high commodity prices and accommodating exchange rate. That contrasted with protracted Brexit negotiations, US-China trade tensions and protests in the regional financial centre of Hong Kong.

“So if you put Australia in the context of the world it is feeling at the better end of that,” Mr Stevens said.

The ASX has been spruiking its credentials for both foreign and technology-oriented listings, bringing with it a “export market” of professional services such as investment banking, accounting and auditing”

Mr Stevens said that is proving successful, but a slow burn in the results.

ASX last down 0.49pc to $87.15.

1.58pm: Stocks extend slide to 2.6pc

Australian shares are having a $51bn wipe-out as the benchmark falls further after lunch, now on track for the biggest one-day fall since October.

The S&P/ASX 200 index fell as much as 2.6 per cent to a 2-month low of 6423.7 and is now well below its August 6 low of 6444.4 that followed the restart of the US-China trade war this month.

It’s likely to close below its 100-day moving average at 6478 for the first time since January.

Somewhat perversely, the Australian bourse is underperforming versus Asian markets due to strong domestic jobs data today.

A bigger-than-expected rise in employment has lessened the chance of another RBA rate cut in the near term.

ASX last at 6426.5.

Sellers remain with the upper hand as the ASX 200 continues to make new lows in afternoon trade. There was no discernible fillip for the Index after the better than expected employment numbers this morning #ausbiz Iress pic.twitter.com/mlpMTR3zIP

— CommSec (@CommSec) August 15, 2019

Bridget Carter 1.50pm: Soprano IPO could be on the cards

Plans could be revised to float the technology company Soprano Design, according to analysts, after attempts were made to list the business in 2016.

In a research note on HT&E, analysts from the Credit Suisse New Zealand affiliate Jarden questioned whether an initial public offering of the Soprano business could be again on the cards.

Soprano is also 25 per cent owned by HT&E, which has launched a strategic review of its non-radio assets.

The analysts questioned whether an IPO could be on the cards with greater disclosure provided on the business.

Soprano is a Sydney-based mobile messaging software solutions provider for enterprises and governments internationally.

The revenue for the business increased 22 per cent for the 2019 financial year and a 13 per cent lift in its earnings before interest, tax, depreciation and amortisation.

It counts Telstra, Vodafone National Australia Bank, Accor, Transurban, Visa and Qantas as among its clients and its technology has been used for television shows such as Australian Idol to support inbound SMS mass voting.

1.43pm: Woodside warns of global recession

Energy giant Woodside Petroleum has warned the world is facing recession with ongoing tensions between the US and China threatening global economic growth.

“I think many people would say technically we’re entering a recession globally and in West Australia we’ve been in that place for a little while,” Woodside chief executive Coleman said after delivering first-half earnings.

While the US-China trade war benefits local LNG producers like Woodside in the short-term by boosting the appeal of Australian exports, the effect of a drawn out spat would crimp growth and lower demand for commodities.

“In the long-term I am concerned that a sustained trade war will actually suppress demand. So I worry about that demand growth running out in the long-term and what effect a trade war would have given that about half of that growth is driven by China.”

China bought 36 per cent of Australia’s LNG in the last financial year, according to consultancy EnergyQuest, second only to Japan at 39 per cent.

The Woodside chief is facing pressure to pull off an ambitious LNG expansion in West Australia involving piping gas from the long delayed Browse gas field to the North West Shelf plant in Karratha.

However, partners in the two joint ventures are yet to agree on tolling deals with Mr Coleman wary it may be leapfrogged by rival suppliers to meet a forecast LNG demand ‘window’ from about 2024 should a deal not be sealed soon.

Woodside last down 6 per cent at $31.40.

Supratim Adhikari 1.32pm: Telstra unfazed by market jitters

Telstra boss Andrew Penn says the telco isn’t overly worried about the current market jitters, with the importance of connectivity insulating Telstra from adverse economic conditions.

Speaking to media after the release of its full year 2019 results, Mr Penn said telecommunications services were now as important as any basic utility.

“Telecommunications is a very fundamental service, a utility for customers and if anything is increasing in importance given how much we are dependent on our telecommunications networks.”

“In the context of an economically challenged market, telecommunications is always going to be an important, safe and in-demand product,” he said.

TLS shares last down 1.4pc at $3.89.

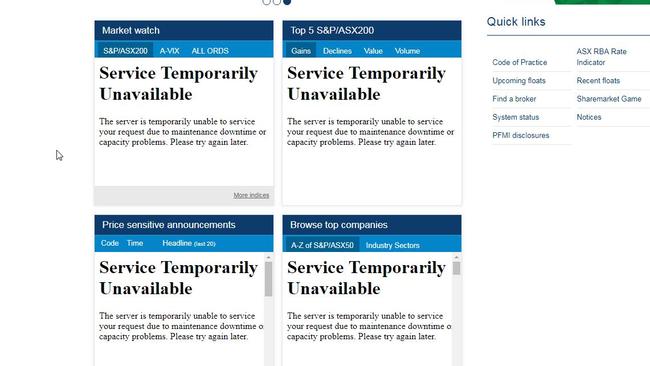

1.27pm: ASX website crashes

As if a drop on the market wasn’t enough, it seems the ASX website itself has crashed.

Punters hoping to check their portfolio declines were left with a “service temporarily unavailable” message at lunch.

“The server is temporarily unable to service your request due to maintenance downtime or capacity problems,” the message reads.

It comes as the market continues to trade lower by 2.3pc to 6446.9.

Bridget Carter 1.14pm: Caltex chief could revive retail sale: MS

Dataroom | The newly appointed chief executive of Caltex could revive plans for a sale of its retail properties, as the company is expected to keep a close focus on costs, according to Morgan Stanley analysts.

In a research note, analysts from Morgan Stanley say that the announced departure of current Caltex boss Julian Segal will likely add some near term uncertainty to the medium term strategy, although this will depend on who next leads the organisation.

However, the analysts say that the sale of its properties could be back on the agenda.

“In the nearer term we expect the company to focus on costs and potentially look

to start divesting some retail property or at least set a process in place for this to

happen,” the analysts said.

Caltex explored a potential sale of its property portfolio a year ago where it could divest between 15 and 25 per cent of its existing freehold site portfolio.

CTX shares last down 3.25pc at $25.88.

1.07pm: Risk of further NAB payout cut: MS

Risk of another dividend cut are rising at National Australia Bank, according to Morgan Stanley.

Following the bank’s third quarter results yesterday, equity analyst Richard Wiles says he expects cash profit ex notable items to be up 1pc for the full year, but forecast a 5pc fall for FY20 as the revenue outlook is more challenging.

He says volume growth has slowed, and RBA rate cuts are driving margin decline with continuing pressure on other income, which accounts for roughly 26pc of group revenue.

“We don’t think the dividend can grow and further initiatives to top up capital are possible given our forecast of a CET1 ratio of just ~10.7pc at FY20E,” Mr Wiles notes.

“All else equal, if the margin declines by >10bp and loan losses reach ~25bp next year, the underlying payout ratio would again rise to ~85pc, leading to risk of another dividend cut.

NAB last down 2.4pc at $27.

12.56pm: CBA tips two more RBA cuts

Commonwealth Bank now sees two more RBA rate cuts on the horizon, lowering the cash rate to 0.5pc by February.

Previously the bank had expected just one more rate cut in November.

“Progress in reducing labour market slack has stalled, global risks have increased to the downside and the RBA’s forecast profile for GDP, inflation and unemployment incorporate two further 25bp rate cuts,” senior economist Gareth Aird says.

But he expects economic activity to lift from here and considers the chance of a domestic recession as “low”.

AUDUSD last at US67.82c.

12.44pm: Xero reaffirms outlook, scoping M&A

Accounting software Xero has reaffirmed its outlook for the year ahead at its AGM as it told shareholders it was cashed up and scoping out acquisition opportunities.

Talking to shareholders in Aukland, chief executive Steve Vamos said its core accounting offering was its biggest immediate opportunity, in existing markets as well as other geographies.

That said, he noted the company had $US300m in the bank after issuing convertible notes last October, giving it financial flexibility.

“We’re evaluating a range of potential M&A opportunities that we screen based on how they support our strategic priorities,” Mr Vamos said.

“Also, as Xero continues to grow, investing to build capabilities that support global scale and innovation include significant focus on growing our talent, and improving all our business processes for operational excellence.”

XRO shares last down 2.6pc to $60.96.

12.30pm: Stocks dive to 2-month low

The Australian sharemarket has continued to dive with the S&P/ASX 200 down 2.3pc at a 2-month low of 6443.0, below the recent low of 6444.4.

It comes after stronger-than-expected July employment data dampened hopes of the RBA cutting rates next month.

The market implied chance of a September rate cut fell to 33pc from 48pc before the data, although the RBA is still expected cut rates before year end.

That has seen the S&P/ASX 200 ignore a 0.5pc rise in S&P 500 futures after the physical market tumbled 2.9pc overnight.

From a purely technical standpoint the tentative break of 6444.4 is concerning as it suggests the index could close below its 100-day moving average at 6478.

The 100-day moving average hasn’t been broken is sustained fashion since January. The 50-DMA had been very good support on dips until this month.

If the ASX200 does close near its low today, it could well be heading for the 200-DMA at 6180, which would mark a 10pc fall from the record high of 6875 it last month.

The chart also shows some potential support at 6380, which marks the 38.2 per cent Fibonacci retracement of the December-July rise.

12.10pm: The session so far …

The Australian market is holding near intraday lows at lunch, as $40 billion is wiped off the market amid fears of a US recession.

Overnight, inversion of the US Treasury yield curve — often seen as a warning of an imminent recession — spooked US markets and prompted the Dow to clock its biggest one-day drop since October.

That same fear is brushing off locally, with the benchmark ASX200 lower by 2.2 per cent or 143 point drop to 6452 and wiping $40 billion off the market’s value.

All sectors are in the red, but energy stocks are the worst performing — down 4.7 per cent after oil dropped 3pc on weak data overnight.

A worse-than-expected result from key producer Woodside, is also weighing on the sector — down 5.5pc.

Results are exacerbating the market weakness, after heavyweight Telstra posted a 40 per cent drop in profit.

Its shares are lower by 1.27 per cent while waste management group Cleanaway leads the losses with a 9.66pc rise after it cut its outlook.

Packing group Orora has been belted by 15.31pc after citing challenging market conditions and cost headwinds this year.

Blackmores has dropped by 5.2 per cent as it cut its dividend and warned of weakness in its key market of China.

But it hasn’t all been bad news — Super Retail is higher by 3.8pc on in-line results, Treasury Wines is up by 3.75pc on news it is acquiring a French vineyard and its Asian demand is holding up.

Gold stocks are in favour as investors flock to safe haven assets — St Barbara, Evolution and Newcrest are rounding out the rest of the top five best performers.

ASX200 last at 6453.1.

12.05pm: Strong jobs don’t rule out stimulus: NAB

A stronger-than-expected 41,000 rise in jobs last month doesn’t preclude further monetary and fiscal stimulus, according to NAB.

“Given the RBA’s focus on reducing spare capacity, NAB continues to believe further stimulus will be needed,” says NAB economist Kaixin Owyong.

“We forecast the next cut to the cash rate to occur by November, to 0.75 per cent. We also expect additional fiscal stimulus to be announced later this year.”

She argues that while the ongoing strength in employment will be reassuring for the RBA, the unemployment rate remains well above the RBA ‘s estimate that the non-accelerating rate of unemployment is around 4.5pc.

“Notably, overall underutilisation rose as underemployment ticked up 0.2 percentage points to 8.4 pc as more part-time workers wanted longer hours of work.”

David Swan 12.01pm: Accenture swoops on Analytics8

Privately held Australian data and analytics consulting firm Analytics8 has been acquired by global consultancy giant Accenture for an undisclosed sum.

Analytics8’s 70 staff, based across Sydney and Melbourne, will joined Accenture’s AI specialist team, Accenture Applied Intelligence.

“We are excited about joining Accenture,” Analytics8 co-owner Hedde Schuitemaker said in a statement.

“Our data scientists and data analytics expertise will complement Accenture’s applied intelligence capabilities and industry knowledge, allowing us to help customers further leverage data and analytics to transform their businesses.”

Accenture has been busy acquiring Australian businesses in the last 12 months, acquiring cybersecurity specialists BCT Solutions in June 2019 and Oracle provider PrimeQ last December.

11.44am: ASX extends loss on Asia weakness

Chinese and Hong Kong markets have added to the global sell-off, both tracking steep losses at the open.

The Shanghai Composite dropped 1.61pc at the open, while the Hang Seng dropped as much as 1.42pc early and is now trading lower by 0.76pc.

That weakness has pulled the ASX lower, last down 2.1 per cent at 6460.1 after touching an intraday low of 6457.5.

11.31am: Employment jump spurs $A rise

A boost in jobs for the month has surpassed expectations, and fuelled a 33 points jump in the Aussie dollar.

The unemployment rate remained at 5.2 per cent for the fourth month running but employment surged 41,100 vs 14,000 expected.

Full time jobs rose 34,500 and part time rose 6,700.

Significantly, the labour force participation rate rose to a record high of 66.1pc.

AUDUSD last at US67.87c.

Interesting - strong employment change still no unemployment movement as participation is BOOMING! #ausbiz pic.twitter.com/B4AiqknBCV

— Evan Lucas (@EvanLucas_INV) August 15, 2019

Sarah-Jane Tasker 11.20am: InvoCare slips despite 97pc profit jump

Funeral services provider InvoCare has posted what it calls “promising” first-half results as the number of deaths reverts to the long-term trend.

The company’s half-year results, released today, show that its operating sales revenue increased 7 per cent to $241.5m, while its operating EBITDA was 16.9 per cent higher at $53.7m.

InvoCare, the largest provider of funeral services in Australia, New Zealand and Singapore, also reported a 97 per cent lift in its net profit after tax to $41.4m. The company said that figure was driven mainly by the over-performance of the funds under management for prepaid funerals.

Despite the positive numbers, shares in the company are down 7 per cent to $14.13 in a market that is following the negative lead set by Wall Street on fears of a US recession.

Perry Williams 11.13am: Orora downbeat on US, Aus economy

Packaging producer Orora has delivered a downbeat assessment of the US and Australian economies, amid heightened market volatility and growing recession fears.

With its shares belted 11 per cent after citing challenging market conditions and cost headwinds this year, Orora chief Nigel Garrard conceded it was a tough operating environment particularly in North America.

“From what we see the US economy has come off a bit,” Mr Garrard said, noting its position servicing manufacturing, food, FMCG and the industrial sectors in the US. “Volumes are flat to declining. Ours have not declined fortunately but they are certainly flat.”

The tepid conditions were due to a range of factors from the government shutdown in January to market tensions from the US China trade war.

“In January we had the government shutdown and that shouldn’t be under estimated,” Mr Garrard said. “There’s no doubt there are cost pressures on products that are imported from China and we have had to deal with that. And I think there’s just a general uncertainty that perhaps we didn’t see 12 months ago in North America.”

Orora shares last down 11 per cent to $2.84.

11.12am: What to expect in jobs data

Australia’s monthly employment data for July are due at 1130 AEST.

The unemployment rate is expected to stay at 5.2 per cent for the fourth month running, based on consensus estimates of a 14,000 rise in employment and an unchanged labour force participation rate of 66pc.

NAB predicts a 15,000 rise in jobs and a 5.3pc jobless rate, implying a higher participation rate.

“The weaker labour market is consistent with the deterioration in our labour market index, which summarises the demand for labour from business surveys, job vacancies and expectations of unemployment,” NAB says.

Samantha Bailey 11.09am: Breville flags US price hike after tariffs

Shares in Breville have lost ground in early trade despite the kitchen appliance maker unveiling a full-year result in line with consensus estimates.

In its full-year results announcement this morning, the company said that adverse changes to the general global economic and geopolitical conditions will impact its financial results in the year ahead.

The company also flagged a price hike on products in its key US market as a result of the latest round of tariffs which are due to come into effect next month.

“Geopolitical tension such as Sino-American tariff escalation and threat of Brexit may specifically impact consumer demand as well as our ability to supply markets,” the company said.

Breville shares fell as much as 3.9 per cent this morning, last down 2.22pc at $18.95.

Eli Greenblat 11.08am: Super Retail bucks market sell-off

A result that was within expectations was enough to help shares in Super Retail Group buck the widespread trend of falling retail shares, with Super Retail up 3.1 per cent to $8.95 this morning.

Elsewhere in retail it was mostly red ink, with Wesfarmers down 2.1 per cent, Woolworths down 1.3 per cent, Coles down 1.85 per cent, Myer down 3.7 per cent and Premier Investments weaker by 2.16 per cent.

Harvey Norman was down by just under 1 per cent while JB Hi-Fi which reported a stellar full-year result on Monday was also down by just under 1 per cent.

11.03am: Cleanaway slumps on results miss

Cleanaway is the worst performing stock on the market after delivering below consensus results and outlook.

The waste manager reported earnings of $461.6 million up 36 per cent on the prior corresponding period, but slightly below Ord Minnett’s $473.5m forecast.

“Surprisingly, the company downgraded the outlook, guiding to EBITDA growth to moderate slightly from currently market expectations (consensus FY20 EBITDA currently $513m),” analysts said.

CWY last down 9.24pc to $2.16.

10.56am: Soft LNG to hit Woodside earnings: Citi

Citi’s James Byrne keeps his Sell rating and $29.13 target on Woodside after its first half results.

Underlying profit of $US419m was 14pc below his estimate, with higher than expected production costs but operating cash flow of $US1,485 was 19pc better than Citi expected on lower cash tax.

“We don’t think the market has priced in the extent to which a soft LNG market will affect earnings from price reviews and valuations for growth projects,” Mr Byrne says.

WPL last down 5pc at $31.71.

Supratim Adhikari 10.51am: Telstra slips on profit tumble

Telstra shares have opened 1.4 per cent weaker after the telco posted a 40 per cent drop in net profit for full year 2019.

Telstra shares started Thursday’s session at $3.88, with the telco warning shareholders that the National Broadband Network will strip up to a billion dollars from its books over financial year 2020.

Net profit for the year ended June 30 decreased 39.6 per cent to $2.1 billion, while total full year income for the period slipped 3.6 per cent to $27.8 billion, landing right in the middle of the forecast range of $26.2bn to $28.1bn.

Chief Andy Penn said that the latest numbers highlight the damage the NBN has caused to the incumbent telco and how the compensation Telstra receives from NBN Co doesn’t go far enough.

“I want to make two points on comments that often come up in relation to the commercial agreements we have with NBN Co.”

“Firstly, the notion that the payments we receive from NBN Co for access to our network leave us better off or somehow give us an advantage. This is not the case as our results clearly show.”

10.44am: Debelle downplays US yield curve fear

RBA Governor Guy Debelle has played down the latest recession signal from the US yield curve.

“It’s obviously a risk out there,” he said in response to question at a speech in Sydney.

“I’m not sure I’d be relying on the yield curve as the best signal of that risk given the yield curve has not obviously got the same sort of structure that it’s had historically.’’

The 2-10 year US Treasury spread turned briefly negative last night as the long end fell more after weak data in China and Germany.

Inversions of the normally positive US yield curve have preceded each of the last 5 US recessions with a lag of 11-23 months, according to NAB.

Lilly Vitorovich 10.40am: HT&E forecasts cut on weak ad market

Macquarie has cut its underlying EPS forecasts on HT&E by 5.4 per cent and 3.4 per cent for 2019 and 2020, respectively, to account for “continued weak ad markets” and the adoption of new accounting rules.

It also trimmed the media group’s target price by 10c to $1.75 a share following its first half results yesterday, which showed that ARN, home of KIIS and Pure Gold radio stations, revenue fell 3.8 per cent and slight EBITDA growth of 0.3 per cent, in a radio ad market that fell 2.4 per cent.

“HT1 is a cash-generative radio business and is a potential takeover target in a consolidating media environment. Additional capital management is likely and the tax issue appears priced in,” Macquarie said in a research report.

HT1 shares last up 0.29pc to $1.72.

10.27am: US futures gain limiting sell-off

US futures gains are limiting the sell-off in the Australian sharemarket so far today, with the benchmark ASX200 down 2pc.

US index futures are currently up about 0.3pc, helping to trim some of the 2.1pc fall implied by overnight futures.

The S&P/ASX 200 has dived to 6465 but is basically still holding the 100-day moving average at 6478.

If it cracks the recent low of 6444.4 for any reason today there could be some panic selling.

China’s yuan fixing at 1115 AEST may show whether the PBoC is willing to help global sentiment.

The market will also be looking at domestic jobs and China’s sharemarket open at 1130 AEST.

10.16am: How todays reports fared at the open

- Telstra shares are lower by 1.9pc to $3.87 after profit plunged 40pc

- ASX shares are lower by 0.64pc to $87.02 despite declaring a bumper special dividend

- Woodside is lower by 4.37pc to $31.97 after maintenance at its Pluto LNG plant and cyclones hit profit by 23pc

- QBE is up 2.48 per cent to $12.38 after lifting profit

- Evolution up 4.65pc to $5.4 as it tipped more payouts to come

- Orora lower by 7.81pc to $2.95

- Super Retail slipping by 0.92pc to $8.60

- Blackmores down 6.8pc to $77.61

- Treasury higher by 0.64pc to $17.19 as it unveiled a French winery acquisition and amid continued strength in Asia

- Cleanaway lower by 11.77pc to $2.10 after delivering a below consensus result and downgrading its outlook

- Breville down 2.43pc to $18.91

- Sydney Airport is lower by 2.1pc to $8.20 on its half year results, as an EU tax bill slashed its profit

9.45am: High Treasury hopes already priced in: Citi

While Treasury Wine’s results were strong this morning, the challenge for the stock is that lofty expectations are already built into forecasts, according to Citi.

They say the winemaker beat consensus with earnings of $663m, and growth of 25pc alongside constrained costs and better ash flow.

But, it keeps the stock at a Sell, saying the beat was already priced in:

“We expect little change to forecasts. There may be excitement about the French acquisition, but depends on size. It looks to be in the order of $30-50 million.”

TWE last traded at $17.08.

Samantha Bailey 9.31am: Euro expansion a winner for Breville

Kitchen appliance maker Breville has delivered a full-year revenue spike partly on the back of a rapid expansion in its European business and a strong performance in the US, which offset weaker export sales to Russia.

Unveiling net profit after tax for the year attributable to shareholders up 15.2 per cent to $67.4 million for the year through June 30, Breville said its rapidly expanding geographic footprint in Europe was already two thirds the size of the Australia and New Zealand business.

“We continued to deliver double digit earnings before interest and tax growth while successfully executing on our acceleration program, increasing our investment in product development and marketing, and geographically expanding in Germany, Austria, Benelux and Switzerland,” chief executive Jim Clayton said.

Breville said that Germany posted a successful first full-year and delivered a stronger revenue in its first year than the UK did in its fourth year of operations.

Earnings before interest and tax growth accelerated to 12 per cent, up from 10 per cent a year ago, though margins were slightly lower, reflecting the strengthening US dollar, as well as an increase in marketing and product development investment.

Earnings before interest, tax, depreciation and amortisation up 13.7 per cent to nearly $114m.

The company will pay a final dividend of 18.5 cents per share 30 per cent franked, up from 16.5c a year ago.

9.29am: Stocks to dive amid recession fears

Australia’s sharemarket looks set to dive with global markets amid growing fears of recession.

Overnight futures imply the S&P/ASX 200 will open down 2.1 per cent at 6457 points — near the two-month low 6444.4 it hit early this month.

That follows a 3pc plunge in the S&P 500 as weak data from China and Germany caused a flight to safety.

The US 10-year bond yield fell 12 basis points to a 3-year low of 1.57 and the 2-10 spread turned negative intraday, fuelling recession talk.

If the S&P/ASX 200 breaks the recent low or closes below the 100-day moving average at 6476, the index could dive to the 200-DMA at 6175.

That would mark a 10pc correction from the record high of 6875 but after a correction in global markets, investors will anticipate stronger central bank easing, a greater US backdown on trade and possibly fiscal stimulus from China.

It’s also a massive day for earnings with 13 ASX200 companies including Woodside, Telstra, QBE, Treasury Wine, Sydney Airport, Blackmores and ASX reporting.

Domestic employment data for July are due at 1130 AEST with the market expecting an unchanged 5.2pc unemployment rate and a 14,000 rise in Jobs.

ASX200 last at 6595.9.

9.27am: What’s impressing analysts, what’s not

- AP Eagers raised to Outperform — Credit Suisse

- Aveo raised to Neutral — Macquarie

- Aveo price target raised 19pc to $2.15 — Morgans

- CSL raised to Outperform, price target raised 25pc to $249 — Credit Suisse

- CSL price target raised 11pc to $220.30 — Morgans

- CSL raised to Hold — Morningstar

- CSL cut to Neutral — UBS

- Fortescue raised to Neutral — UBS

- Genworth raised to Outperform — Macquarie

- NAB price target raised 5.1pc to $29 — Bell Potter

- Pact Group target price cut 16pc to $2.39 — Morgans

- Regis Resources raised to Neutral — JP Morgan

- Service Stream price target raised 20pc to $2.95 — Cannaccord

Robyn Ironside 9.19am: Tax bill bites Syd Airport profit

Sydney Airport has posted a drastically reduced half-year profit of $17.3 million down from $173 million in the previous corresponding period.

The dramatic fall was the result of a $181.7m tax bill issued by the European Union Court of Justice, in relation to the 2011 sale of Sydney Airport’s stake in Copenhagen Airport.

The one-off expense had no bearing on distribution which would be paid immediately at 19.5 cents a share.

Sydney chief executive officer Geoff Culbert described the half-year result as “solid” and reflective of continuing international passenger growth, robust retail performance and a deliberate and disciplined approach to cost control.

Although international passengers grew 1.9 per cent in the six months to 8.3m, domestic passengers were down 1.5 per cent which reduced total passenger numbers by 0.2 per cent to 26.1m.

The downturn in domestic travellers, blamed on capacity reductions and subdued demand, took its toll on car parking and ground transport revenue, which fell 1.4 per cent to $77.6m.

On a more positive note for the airport, aeronautical revenue, collected from airlines was up 4.7 per cent to $361.3m due to international passenger growth, and retail revenue improved 4 per cent to $184.2m.

Andrew White 9.16am: Market boom prompts ASX special div

Financial markets operator ASX will pay a special dividend on top of an increased regular payout after booming equity and futures market volumes pushed statutory net profit up 10.5 per cent.

ASX returned $492.0 million after tax, up $46.9 million with each of ASX’s four main businesses growing and interest earnings on settlement deposits. Chief executive Dominic Stevens said there was also an increasing appetite from customers for technical connections and information services.

Revenue rose 5 per cent to $863 million, which was half the rate of growth in expenses — up 9.9 per cent to $214.8 million.

“ASX’s diversified business model continues to deliver attractive earnings across different business cycles without compromising our commitment to operating markets of high quality,” Mr Stevens said.

ASX will pay a final dividend of 114.3 cents per share, a rise of 4.8 per cent and making 228.7 cents a share for the year at a payout ratio of 90 per cent of profits.

Shareholders will also receive a 129.1 cents a share special dividend from the proceeds of the sale of its stake in market information business IRESS.

ASX shares are up 46 per cent since January and touched a record high of $89.20 last week. They are trading on a heady multiple of 34 times earnings.

9.00am: Chinese slowdown hits Blackmores

Vitamin maker Blackmores says Chinese consumers are turning off Australian products, a key factor behind its 24 per cent profit drop for the year, with sales to the market dropping 15 per cent.

The company posted net profit after tax of $53 million, down 24 per cent on the prior year, but a slight uptick in revenue to $610m.

Excluding one-off costs to streamline the business, underlying net profit was $55m.

It said China eCommerce changes, effective from January 2019, had prompted a shift in consumption patterns away from Australian retailers to more direct purchasing from e-commerce platforms in China.

The board declared a final dividend of 70 cents per share, taking total dividends for the year to 220cps.

It said challenging conditions in China were expected to continue during the first part of FY20, but that the second half was likely to benefit from operational efficiencies from recent business improvement initiatives.

Samantha Bailey 8.57am: Super Retail flags ‘subdued’ trade

Super Retail Group has flagged “subdued” trading for the first six weeks of the new financial year as it unveiled a full-year normalised net profit after tax up 5 per cent on the prior year.

The company, which owns retail stores such as Supercheap Auto, Ray’s, Macpac, Rebel and BCF, said that sales across the group had lifted 5.4 per cent to $2.71bn.

Super retail will pay a fully franked final dividend of 28.5 cents per share, up from 27.5c a year ago.

While trading conditions had been weak for the beginning of the new financial year, the group’s largest three businesses — Supercheap Auto, Rebel and BCF — were delivering positive like-for-like sales growth.

8.55am: Evolution profit slips, boosts payout

Gold producer Evolution Mining recorded a 17 per cent fall in annual profit mainly because higher operating costs and taxes combined with lower revenue from the copper and silver by-products it sells.

The Australian miner on Thursday reported a net profit of $218.2 for the 12 months through June. That was down from $263.4 million a year earlier.

Still, directors declared a year-end payout of 6 cents a share, up from 4 cents a year ago. That reflected a new policy aimed at paying shareholders roughly 50pc of free cash flow, the company said.

“With the current spot price around $450 higher than the $1,760 per ounce gold price achieved in FY19, we remain focused on maintaining our low cost base to bank every additional dollar and return excess funds to our shareholders,” said Executive Chairman Jake Klein.

Dow Jones Newswires

Perry Williams 8.47am: Pluto shut down dents Woodside profit

Oil and gas producer Woodside Petroleum has suffered a 23 per cent fall in first half profit after taking a hit from maintenance at its flagship Pluto LNG plant and the impact from cyclones.

Net profit after tax for the six months ended June 30 fell to $US419 million ($620m) from $US541m as revenue eased five per cent to $US2.26 billion.

The Perth producer retained its guidance for production this year at the lower end of 88 million to 94m barrels of oil equivalent and says it remains on track to achieve annual production of 100m boe in 2020.

Woodside declared an interim dividend about a third lower on last year at US36c per share compared with US53c per share.

The energy operator is preparing for final investment decisions on its Browse gas field in Western Australia next year.

The latest development plans for Browse, where gas was found in the early 1970s, focus on a 900km-long pipeline south to the nation’s original LNG plant, the North West Shelf. The gas would be used to backfill the plant as its existing gas fields decline, with Browse eventually producing up to 11.4 million tonnes of LNG a year.

Supratim Adhikari 8.42am: Telstra sells data centres in overhaul

Telstra boss Andrew Penn said the full year numbers highlight why the telco has had to embark on the ‘Telstra 2022’ strategic overhaul.

“Notwithstanding the intense competitive environment and the challenging structural dynamics of our industry, it is a year in which I believe we can start to see the turning point in the fortunes of the company from the changes we have embraced,” Mr Penn said.

Part of the turnaround has seen Telstra seen sell three international data centres in Europe and Asia for $160m to global private equity firm I-Squared Capital, the owners of Hutchison Global Communications.

The three data centres predominantly provide services to Telstra’s International Enterprise customers. The agreement is subject to conditions and is expected to be completed in first half of full year 2020.

8.35am: First earnings drop for Orora

Packaging company Orora reported its first fall in statutory earnings since listing on the ASX in late 2013 as it absorbed extra decommissioning charges tied to its Petrie Mill site, restructuring and other impairment charges.

Orora reported a net profit of $161.2 million for the 12 months through June, down from $212.2 million a year earlier.

Directors declared a final dividend of 6.5 cents a share, bringing the full-year payout to 13.0 cents, up 4pc on fiscal 2018.

Stripping out one-time charges, Orora’s annual profit rose by 4pc to $217.0 million and earnings per share lifted by 3.7pc to 18.0 cents.

Chief Executive Nigel Garrard said growth in annual underlying earnings was achieved despite “challenging economic and market conditions, particularly in North America.”

“Orora has been proactive in responding to the challenging market conditions by completing a group wide restructuring initiative which resulted in recording a significant item expense after tax of A$20.8 million,” Mr. Garrard said.

Dow Jones Newswires

8.32am: Treasury profits boosted by Asia

Australian winemaker Treasury Wine Estates said net profit rose about 16 per cent in the year through June, reflecting strong growth in Asia and the company’s continued focus on the higher end of the market.

Annual net profit was 4419.5 million, while revenue also rose about 16pc to nearly $2.9 billion. Earnings before interest, tax and other items rose by 25pc to $662.7 million.

The company declared a final dividend of 20 cents per share, bringing the full-year payout to 38c, up 19pc.

Looking forward, Treasury reiterated guidance for 15pc to 20pc growth in earnings before interest, tax and other items for the current fiscal year.

The company on Thursday also confirmed the acquisition of French production and vineyard assets in the Bordeaux region in France, and announced a future expansion of its luxury winemaking infrastructure in South Australia.

Those initiatives underscore Treasury’s focus on the higher end of the wine market, which is known as “premiumization”, and comes as consumers are increasingly willing to pay for higher-quality wine.

Dow Jones Newswires

8.22am: Telstra profit down 40pc

Telstra says its full year net profit has dropped 40 per cent to $2.15 billion.

The telco says total income was down 3.6 per cent to $27.81bn.

It will pay a final dividend of eight cents per share.

Telstra says its results are in line with guidance and market expectations.

But it said the largest reason for the decline in earnings was the impact of the NBN, with Telstra absorbing “around $600 million of negative recurring EBITDA headwind” in the period.

“To date we estimate the NBN has adversely impacted EBITDA by approximately $US1.7

billion, and estimate we are around 50 per cent of the way through the recurring financial impact of the NBN,” Telstra said.

8.15am: QBE profit rises 29pc

Insurance Group QBE said its half-year profit rose strongly, bolstered by a decline in claims losses and a strong improvement in investment returns.

Net profit rose by 29 per cent to $US463 million in the first six months of the year from $US358 million in the first half of 2018.

Gross written premium was up about 1 per cent to $US7.64 billion and the net investment return widened appreciably to 6.8 per cent from 2.1 per cent a year earlier, which QBE said reflected strong returns across most asset classes.

The Sydney-based insurer exited a number of businesses and portfolios last year, which cumulatively generated underwriting losses in 2017 of about $US200 million. They included its entire division in Latin America, operations in Thailand, the Philippines and Indonesia and travel-insurance in Australia.

Dow Jones

8.05am: Copper falls

Copper prices fell overnight after industrial output growth in China — the largest metals consumer — fell to a more than 17-year low, weakening the outlook for demand.

Benchmark copper on the London Metal Exchange (LME) ended down 1.1 per cent at $US5,765 a tonne, nearing a two-year low of $US5,640 reached earlier this month. Copper had risen on Tuesday after US President Donald Trump said he would delay new tariffs on Chinese imports, raising hopes that an economically damaging trade dispute could de-escalate.

But the Chinese data, a downbeat assessment of the state of US-China negotiations by US Commerce Secretary Wilbur Ross and figures showing Germany’s economy contracted in the second quarter revived the bearish mood. “The global economic outlook is still negative,” said Saxo Bank analyst Ole Hansen.

Reuters

7.30am: Oil drops 3pc

Oil prices shed 3.0 per cent overnight after Chinese and European economic data revived global demand fears and US crude inventories rose unexpectedly for the second week in a row.

Brent crude settled at $US59.48 a barrel, shedding $US1.82, or 3.0 per cent, losing some of the previous session’s sharp gains after the United States moved to delay tariffs on some Chinese products.

The global benchmark rose 4.7 per cent on Tuesday, its biggest daily percentage gain since December.

US West Texas Intermediate (WTI) crude futures settled at $US55.23 a barrel, falling $US1.87, or 3.3 per cent, after having risen 4.0 per cent in the previous session — the most in just over a month.

Reuters

7.10am: ASX to dive after Wall St rout

The Australian share market is expected to open sharply lower after a major sell-off on Wall Street.

At 7am (AEST) the SPI200 futures contract was down 131 points, or 2.00 per cent, at 6,404.0, suggesting an early slump for the benchmark S&P/ASX200.

On Wall Street overnight, the Dow Jones Industrial Average finished down 3.05 per cent- its biggest one-day point drop since October — while the S&P 500 was down 2.93 per cent and the tech-heavy Nasdaq Composite was down 3.02 per cent.

The US Treasury yield curve temporarily inverted for the first time since June 2007 overnight — with two-year Treasury yields surpassing those of 10-year bonds — in a development that has often preceded recessions.

The Aussie dollar is buying US67.47 cents from US67.82 cents on Wednesday.

AAP

7.00am: Dow plunges 3.1pc in stocks rout

It was an ugly day for Wall Street, as stocks plummeted amid worsening economic fears after US Treasury yields briefly inverted, flashing a warning sign for a coming recession.

But President Donald Trump once again blamed the Fed for the economic woes and the yield curve inversion, saying the US central bank is a bigger threat than China and is “clueless.” The Dow Jones Industrial Average fell 3.1 per cent to finish at 25,479.42, a loss of about 800 points — its worst day of 2019.

The broadbased S&P 500 slumped 2.9 per cent to 2,840.60, while the tech-rich Nasdaq Composite Index dropped 3.0 per cent to 7,773.94.

Australian stocks are set to follow the US lower. At 7am (AEST) the SPI futures index was down 131 points, or 2 per cent.

The sell-off came shortly after the yield on the 10-year US Treasury note briefly dipped below the yield on the two-year, a dynamic that has been a reliable harbinger of past recessions.

The rout followed the latest stream of poor economic data from overseas, including the weakest Chinese factory output data in 17 years and German data showing the economy contracted in the second quarter.

The intensifying US trade war with China has been a key factor in the concerns about the slowing global economy, but shortly after the Dow hit bottom, Trump renewed his attacks on the Federal Reserve and its Chairman Jay Powell, whom Trump appointed.

“China is not our problem … Our problem is with the Fed,” Trump tweeted, blaming “clueless Jay Powell and the Federal Reserve.” The Fed “Raised too much & too fast. Now too slow to cut … Germany, and many others, are playing the game! CRAZY INVERTED YIELD CURVE! We should easily be reaping big Rewards & Gains, but the Fed is holding us back,” he said.

A note from Oxford Economics said the research firm’s recession models as on “high alert.”

AFP

..Spread is way too much as other countries say THANK YOU to clueless Jay Powell and the Federal Reserve. Germany, and many others, are playing the game! CRAZY INVERTED YIELD CURVE! We should easily be reaping big Rewards & Gains, but the Fed is holding us back. We will Win!

— Donald J. Trump (@realDonaldTrump) August 14, 2019

6.45am: Capital One suspect may have hacked others

Federal prosecutors say a woman charged in a massive data breach at Capital One may have hacked more than 30 other organisations.

Paige Thompson, of Seattle, was arrested last month after the FBI said she obtained personal information from more than 100 million Capital One credit applications. There is no evidence the data was sold or distributed to others.

In a memorandum filed ahead of a court hearing Thursday, the US Attorney’s Office in Seattle said servers found in Thompson’s bedroom contained data stolen from more than 30 unnamed companies, educational institutions and other entities.

Prosecutors said much of that data did not appear to contain personal identifying information.

AP

6.42am: Ford recalls 108K cars

Ford is recalling over 108,000 midsize cars in North America to fix a problem that could stop the seat belts from holding people in a crash. The recall covers certain Ford Fusion and Lincoln MKZ cars from the 2015 model year. The company says the cars’ front seat belt cables can lose strength due to heat build-up and may not adequately restrain passengers.

Ford says it’s aware of one injury from the problem.

AP

6.40am: Facebook paid to transcribe audio clips

Facebook has paid contractors to transcribe audio clips from users of its Messenger service, raising privacy concerns for a company with a history of privacy lapses.

The practice was, until recently, common in the tech industry. Companies say the practice helps improve their services. But users aren’t typically aware that humans and not just computers are reviewing audio.

Transcriptions done by humans raise bigger concerns because of the potential of rogue employees or contractors leaking details. The practice at Google emerged after some of its Dutch language audio snippets were leaked.

AP

6.38am: Markets slump on growth fears

Stock markets on both sides of the Atlantic saw hefty losses Wednesday, gripped by fears for the global economy only a day after enthusiasm over possible détente in an ongoing US-China trade war had given them a dizzying lift.

A German GDP contraction in the second quarter, weak Chinese industrial output and an inversion of the US yield curve all seemed to cement fears of a global slowdown.

“The joyous reaction in the markets to the news that the US would delay increasing tariffs on some Chinese consumer products appears to have been short-lived,” said David Cheetham at XTB.

Eurozone indices were more than two per cent down by the close.

The yield on the 10-year US Treasury bond, meanwhile, briefly slid below the yield on two-year debt Wednesday, a rare phenomenon that has often been a harbinger of recession.

“On the economics dashboard of doom, we have another flashing warning light,” said analysts at ING economics. “The market is worried about a recession. For now we don’t see it, but there is a chance the fear becomes self-fulfilling,” they said.

Bond yields have gyrated in recent weeks, with analysts warning that sinking rates are a sign of a worsening medium-term and near-term economic outlook.

XTB’s Cheetham noted, however, that stocks were not usually in immediate trouble from bond yield inversions.

Whenever yields inverted in the past 60 years, it took US stocks at least three months, or even up to 22 months, before they peaked, he said.

“Sinking yields are the bond market’s way of pressuring the Fed to step on the monetary gas pedal and cut interest rates,” Joe Manimbo, senior market analyst at Western Union Business Solutions, said in a note.

European and US stocks had risen across the board on Tuesday on news that the United States had delayed tariffs on a swath of Chinese goods easing tensions in their bitter trade war, an upward trend that was mirrored by Asian stocks Wednesday.

Shanghai managed gains despite data showing Chinese factory output expanded last month at its slowest pace in 17 years.

But in European trading, Frankfurt slumped to its lowest level since March after data showed Germany’s economy contracted in the second quarter, highlighting its vulnerability to trade tensions and stoking debate on higher government spending.

Germany actually lagged Italy’s standstill economy — and France which posted 0.2 per cent growth.

London closed down 1.4 per cent, Frankfurt ended down 2.2 per cent and Paris finished down 2.1 per cent.

AFP

6.35am: Argentine leader AIDS poor

A walloping at the polls has led President Mauricio Macri to decree economic relief for poor and working-class Argentines. The measures include an increased minimum wage, reduced payroll taxes, a bonus for informal workers and a freeze in gasoline prices — at least temporarily.

The conservative leader said he’s acting in recognition of the “anger” Argentines expressed in Sunday’s primary election, when Macri trailed his leftist rivals by 15 percentage points. The general election is in October.

Investors frightened by leftist gains sent Argentina’s stocks, bonds and currency tumbling.

The currency continued to slip after Wednesday’s announcement.

AP

6.30am: NBN lifts revenue 43pc

The NBN has lifted full-year revenue 43 per cent to $2.83 billion, $200 million above guidance.

NBN Co, the builder and operator of the national broadband network, says the number of customers on the network rose 37 per cent to 5.53 million over the 12 months to June 30 and average revenue per user grew to $46 from $44 a year earlier.

The network is now 85 per cent complete and on track to be fully built by the end of the next financial year.

AAP

6.25am: Tencent earnings beat estimates

Chinese internet giant Tencent said its net profit jumped 35 per cent in the second quarter, as the company continued to wriggle out of Beijing’s crackdown on online gaming and build mobile game growth.

Shenzhen-based Tencent said net profit was 24.1 billion yuan ($US3.5 billion) in the three months ending June 30, beating an average estimate from Bloomberg analysts of 21.1 billion yuan.

Total revenues were up 21 per cent at 88.8 billion yuan, primarily driven by mobile game growth, commercial payment services, and digital content businesses.

Tencent’s smartphone games revenues climbed 26 per cent in the three months. But Tencent was hammered by a Chinese government crackdown on gaming which launched last year and led to a months-long licence approval freeze.

AFP

6.20am: Banks dragging feet on Brexit: ECB

Lenders have fallen behind in preparations for a possible no-deal Brexit and must pick up the pace, the European Central Bank warned, as the rhetoric over a possible chaotic departure escalated in London.

“So far, banks have transferred significantly fewer activities, critical functions and staff to euro area entities than originally foreseen as part of their plans for Brexit Day 1,” the ECB said in a monthly newsletter.

The eurozone’s top supervisor “now expects banks to speed up the implementation of their plans,” it added.

Charged with keeping an eye on 119 of the biggest and most important banks in the single currency bloc since 2014, the ECB has long urged financial firms to get their houses in order before Brexit.

Banks had to submit plans “in particular regarding the build-up of local risk management capabilities and governance structures” in the eurozone to be able to continue serving eurozone clients with the supervisor’s blessing.

AFP

6.15am: Treasury yields signal possible recession

An economic alarm bell has sounded in the US, sending warnings of a possible recession ahead.

Yields on 2-year and 10-year Treasury notes inverted early Wednesday, a market phenomenon that shows investors want more in return for short-term government bonds than they are for long-term bonds.

It’s the first time that has happened since the Great Recession and it can be an indication that investors have lost faith in the soundness of the US economy. What appeared to be a slight thaw in trade relations between the US and China that had sent markets sharply higher Tuesday was quickly forgotten Wednesday. At the opening bell the Dow tumbled 400 points.

The yield on the benchmark 10-year Treasury note hit 1.622 per cent, falling below the yield of a 2-year, which was 1.634 per cent. The last inversion of this part of the yield curve was in December 2005, two years before a recession brought on by the financial crisis hit.

An inversion like the one taking place Wednesday has preceded the last nine recessions dating back to 1955, though it doesn’t always mean recession is imminent.

And when a recession might hit, if it does, is tricky. Months or even years have passed after an inversion takes place, and before economists can connect the two.

AP

6.10am: German economy shrinks

The German economy shrank by 0.1 per cent in the second quarter from the previous three-month period as global trade conflicts and troubles in the auto industry weighed on Europe’s largest economy.

The state statistics agency Destatis said falling exports held back output while demand from consumers and government spending at home supported the economy. In comparison to the same quarter a year ago, the economy grew 0.4 per cent.

Germany’s economy is facing headwinds as its auto industry, a key employer and pillar of growth, faces challenges adjusting to tougher emissions standards in Europe and China and to technological change.

Uncertainty over the terms of Britain’s planned exit from the EU has also weighed on confidence more generally — British Prime Minister Boris Johnson has said his country will leave the EU on October 31, with or without a divorce deal to smooth the path to the new trading relationship.

AP

Add your comment to this story

Fortescue rises; Macquarie down on profit dip as first strike looms

Fortescue cans hydrogen projects, ships more iron in FY25. Macquarie AGM strike vote 'close' after flagging profit dip, CFO exit. Aus lifts US beef ban. Bapcor top loser on profit warning amid board exodus.

ASX hits 3-day high led by miners, resurgent banks

Glencore preps for Queensland smelter closure. Ampol flags lower earnings. Woodside's US hydrogen hit. Quarterly updates weigh on Telix, Paladin.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout