Evergrande is an economic time bomb for China and potentially Australia

China is potentially facing their Lehman Brothers moment – and the consequences could be huge for Australian house prices.

Companies

Don't miss out on the headlines from Companies. Followed categories will be added to My News.

In the years since the Global Financial Crisis (GFC), the issues within China’s financial system and property market have become increasingly apparent.

From the infamous ghost cities to the estimated 80 million homes that sit completely empty, the writing has been on the wall detailing the risks for years. Yet despite predictions that it would all come crashing down in one spectacular heap, the Chinese property sector has not only survived but evolved into an even greater driver of China’s economic growth.

But behind this apparent success story lurks a far more complex and challenging reality. For years whenever a large property developer or construction company got into a level of trouble that threatened systemic stability, Beijing would generally step in and bail them out in one way or another.

Given the level of control the Chinese government wields over the financial system and the corporate world in China, these bailouts and de facto rescues have taken on many different forms over the years.

But each time the core of the issue was maintaining the strong economic growth that Beijing has become reliant upon and protecting the wealth of existing property holders.

With Chinese households holding more than 60 per cent of their wealth in the form of property, allowing prices to fall and the construction sector to be impacted by rising bad debts was a bitter pill for Beijing to swallow.

As President Xi Jinping’s push to prepare China for a global black swan event continues, it’s becoming increasingly clear that Beijing may no longer have the will to step in so overtly.

Without Beijing’s ongoing intervention, the already gaping cracks in the Chinese financial system and property sector have become clear for the world to see.

Evergrande: super Chinese property developer, with a super problem

In recent days Chinese mega developer Evergrande has been making headlines, as it heads for a corporate restructuring that could see investors lose tens of billions of dollars.

To put Evergrande’s immense size and importance to the Chinese economy into perspective, its debts amount to around $US315 billion ($A432 billion).

That is more than three times the entire debt load of the New Zealand government and around two-thirds of all outstanding Australian federal debt.

As Evergrande struggles to pay its creditors, mum and dad investors have stormed the company’s headquarters to demand their money back, after payments to retail investors were stopped.

Evergrande protesters chanting "還錢". "Return our money." pic.twitter.com/MJqIytkK8L

— mhar4 述而ä¸ä½œ (@mhar4) September 14, 2021

Evergrande is not the only Chinese property developer in major distress. Across a long list of China’s biggest property developers, a significant number are in similar financial trouble, with their collective debts in a distressed state exceeding more than $US500 billion ($A686 billion).

1/3 While the collective world thinks Evergrande is the only Chinese developer at risk, they are wrong - i.e., Evergrande is not unique nor is it the first. That is, looking at the 10 Chinese developers below, interestingly, combined, the names (each in default or significant... pic.twitter.com/WKylM2Nwj7

— Gordon Johnson (@GordonJohnson19) September 14, 2021

China’s Lehman Brothers moment?

As speculation over Evergrande’s fate continues to build, there are concerns that a disorderly default on its obligations could trigger a financial crisis in China that could spread throughout the rest of the world.

In an announcement on Wednesday, the Chinese Housing Ministry confirmed that Evergrande would not be making interest payments to banks scheduled for Monday. This has raised the uncomfortable possibility that Evergrande’s woes could spread into the Chinese banking system, with potentially far-reaching consequences.

As it stands investors in the Chinese high yield bond market is already pricing in the strong possibility of trouble ahead, with borrowing costs for companies with lower credit ratings rocketing towards the highs recorded during last year’s initial lockdowns.

Going forward markets expect that eventually the Chinese government will step in, ensuring that Evergrande’s woes don’t lead to a risk of contagion throughout the Chinese financial system.

But exactly how this bailout or backdoor rescue package could play out remains to be seen, particularly if Beijing wants to hold investors’ feet to the fire to send a message they will no longer so readily step in.

However, there is increasingly speculation that the holders of US dollar denominated Evergrande bonds and those holding Chinese yuan denominated ones will be treated quite differently in the event of a default or restructuring.

In a recent interview with Bloomberg, Nomura International Hong Kong credit analyst Iris Chen shared her prediction that Beijing will ensure that Evergrande delivers homes to buyers and pays suppliers, but that dollar denominated investors would get only 25 per cent of their money back.

Implications for Australia

Whether Evergrande’s restructuring will end in a whimper or a bang on the global stage remains to be seen. But even if the consequences are largely contained within the Chinese property sector, there could be potentially significant knock-on effects.

In a scenario where a protracted crisis unfolds within the Chinese property sector, the Australian property market and economy could end up feeling the heat.

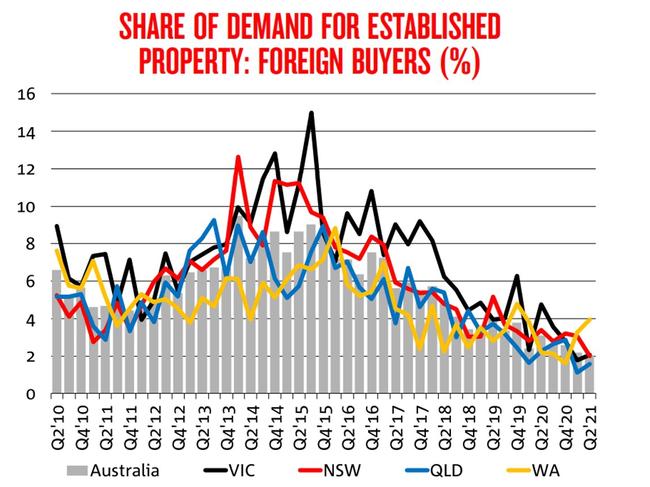

If Chinese investors who own Australian property are forced to liquidate their assets in order to cover bad debts, some suburbs with a high proportion of Chinese ownership could see a significant increase in the number of properties on the market.

There are also Chinese property developers who have large holdings of Australian real estate, who could be forced to liquidate their foreign asset holdings as they attempt to keep their businesses afloat.

But perhaps the most immediate blow to result from a crisis in the Chinese property sector would be the reduction in demand for Australian iron ore.

As by far the world’s largest importer of iron ore by an enormous margin, any significant reduction in Chinese demand would have major implications for the economy and the federal budget.

According to the 2021-22 federal budget, every $US10 the price of iron ore falls nominal GDP decreases by $6.5 billion and the budget coffers are drained of $1.3 billion.

Ultimately Evergrande’s fate and that of the Chinese property sector lies in the hands of Chinese President Xi Jinping and the Chinese Communist Party leadership.

They may well swerve in this game of chicken with the property sector and bond market, effectively restoring the status quo after some painful but isolated blows to investors’ hip pockets.

But if Xi is willing to roll the dice on truly reigning in excess in the property sector and Chinese financial markets, Evergrande’s woes could be just the beginning of a more protracted crisis with consequences that could echo throughout the world.

Tarric Brooker is a freelance journalist and social commentator | @AvidCommentator

Originally published as Evergrande is an economic time bomb for China and potentially Australia

Qantas sets up secret line to hackers

Qantas has been forced to set up its own version of the bat signal to serve papers on the cyber criminal behind an unnerving database hack.

Qantas reclaims punctuality crown from Virgin

Qantas has outperformed Virgin Australia for the first time this year in June, to be the most punctual airline, as partner Jetstar clocked the least cancellations.