Homeowners face nightmare 2023 as property market remains unstable

Circumstances look set to conspire to create a nightmare scenario for homeowners in 2023 – but there could be a solution.

Economy

Don't miss out on the headlines from Economy. Followed categories will be added to My News.

ANALYSIS

In the life and times of Australian households, there are turning points after which things are irrevocably changed for decades to come.

On February 23, 1990, the RBA cut the cash rate from 17.5 per cent to 17.0 per cent. Over the next three-and-a-half years the cash rate would be slashed again and again, until finally coming to rest at 4.75 per cent, a small fraction of what it was at its peak.

Over the following two decades, sleepless nights over the possibility of rising rates slowly became a thing of the past for many Australians, after rate rises effectively went extinct as a force in late 2010. The psyche of households and the landscape of homeownership were forever changed by this turning point.

But now, as Australians stare down the fastest relative rise in mortgage rates in the nation’s history, we may be looking at another turning point, after which things will never be the same again. It wouldn’t be the first time this happened – in the past, mortgage rates have stayed range bound for a decade only to set off to new heights.

The year it all changed

In order to understand what’s happening today we need to look to the past.

Back in 1968, when The Beatles song Hey Jude was the number one track on the radio and Australians were turning into the news each night for the latest developments in Vietnam, a period of relatively stable mortgage rates that had persisted for almost a decade was drawing to a close.

Between the start of comparable records in January 1959 and July 1968, the standard variable mortgage rate ranged between 5 per cent and 5.5 per cent, offering a sense of stability and certainty for mortgage holders and prospective homebuyers.

But as the inflationary pressures experienced by the United States and others, resulting from the Vietnam War and other factors began to feed through into Australian consumer prices, things began to change.

Between July 1968 and June 1989, an entire generation of Australians saw a trend of rising interest rates, with the standard variable mortgage rate increasing from 5.38 per cent to 17 per cent.

In the same way that most of the last 32 years saw Australians come to see rate rises largely as a thing of the past, this 21-year period taught a different lesson – that it was possible that interest rates could always go higher.

The big question in 2022 is: Are we experiencing a similar moment to Australians in 1968? Have we seen the bottom of mortgage rates for potentially decades to come?

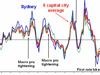

RBA distortion

During 2020 and 2021, the RBA’s $188 billion Term Funding Facility (TFF) helped suppress fixed-term mortgage rates to the lowest level in history. During 2021, the average new fixed-rate loan for an owner occupier was written at just 2.05 per cent.

During that time, the prevailing variable rate payable on owner occupier mortgages was 3.05 per cent.

Unless the RBA throws another enormous support package at the banking system or we see another market meltdown comparable to 2008, it’s hard to see how mortgage rates would return to the record lows seen on fixed-rate loans in 2021.

Housing’s importance to the economy

In the year to June 2021, Australians withdrew $93 billion (4.65 per cent of GDP) in home equity to do with as they pleased – whether it was for a new car, a home renovation or something else entirely.

During the era of the Global Financial Crisis (GFC), Americans copped a great deal of criticism for using home equity in the same way. But it never rose to the same degree of economic importance as it has in Australia, with US home equity withdrawals peaking at 2.6 per cent of GDP.

If home equity withdrawals were to evaporate in the same way they did in the US following the GFC, it would eventually be equivalent to roughly five Rudd-era cash handout stimulus packages being pulled out of the economy each year (relative to GDP).

While this is a risky state of affairs for the economy to operate in, there is little appetite from policymakers to shift from the current course.

The outlook

While the future of inflationary pressures and interest rates impact everything from business borrowing costs to the returns on our superannuation, perhaps the most outsized impact would be on housing prices.

If the game has changed and we’ve seen a generational low in interest rates in the same way as 1968, then housing prices face a very different set of circumstances to the ones faced over the past 30 years.

Between 1991 and 2012, household incomes grew strongly and significantly outstripped inflation, as the Australian economic growth story hit its zenith. But in 2022, things are far less positive.

The RBA estimates inflation will continue to outstrip wages for another year and that by the time wages growth resumes in inflation-adjusted terms, the gains made in real wages over the past 14 years would have largely evaporated.

Households being forced to pay a greater proportion of their incomes on providing the basics is not a terribly positive scenario for the housing market, with people left with less each month to pay their housing costs.

On the other hand, if we see a set of circumstances where inflation moderates in a big way or some form of economic meltdown, we may see interest rates get cut aggressively back towards their early 2022 lows.

Whether the RBA would be willing to act this aggressively in this type of scenario, despite the risks of reigniting inflation, is an open question. We could see them be more conservative and maintain higher than Covid emergency low rates, or they could throw caution to the wind, slashing rates in an attempt to support the economy and housing market.

Tarric Brooker is a freelance journalist and social commentator | @AvidCommentator

Originally published as Homeowners face nightmare 2023 as property market remains unstable

Act that hurt Keno owner’s bottom line

Less people are gambling on lotteries, and a move introduced on one of Australia’s most popular games has hurt one company’s bottom line.

Why rate cut ‘doesn’t help anyone’

An economist has issued a scathing assessment of the RBA’s interest rate cut saying it will only make the cost-of-living crisis worse.

Wild Trump move ‘scaring the RBA’

David “Kochie” Koch has weighed in on the state of play for Australia, throwing a few jabs at Donald Trump in the process.

ASX tumbles on big bank, Woodside woes

A slump in the big banks and energy stocks pushed the Aussie market into the red on Tuesday, as the RBA struck a note of caution following its long-awaited rate cut.

Aussie response to big RBA move says it all

After four gruelling years, the RBA has finally handed down a much-needed rate cut, but the response from everyday Aussies says it all.

Question Treasurer won’t answer after cuts

Boosting expectations that the Prime Minister will call an April federal election within weeks, the decision is a huge relief for the Albanese Government with the Treasurer declaring it was the rate cut families “need and deserve”.