‘We cannot stress enough the fragility of supply’: Canaccord says uranium stocks will run higher

Canaccord Genuity says it ‘cannot stress enough’ the fragility of uranium supply, predicting another surge in prices – and the value of stocks in the sector.

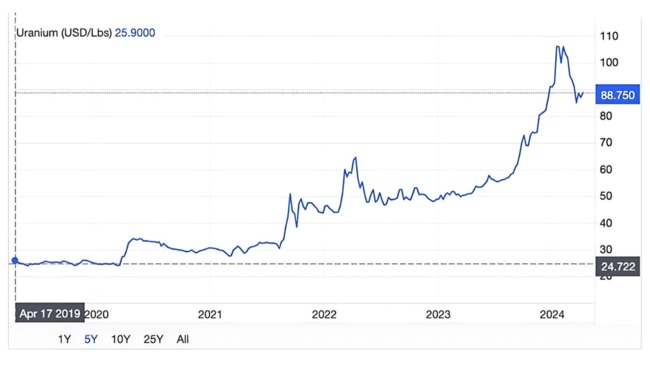

The uranium spot price is taking a breather in the high $US80s a pound, following a scorching run through the psychologically important $100/lb mark in late 2023, early 2024.

The equities trade has also died off somewhat alongside prices, and perhaps as shinier prospects, like gold, take centre stage.

For the latest resources news, sign up here for free Stockhead daily newsletters

Still, Canaccord Genuity says the structural supply deficit which triggered this long-awaited, +200 per cent spot price run in the first place – from $US28/lb in August 2021 to $US88/lb currently – has not gone away.

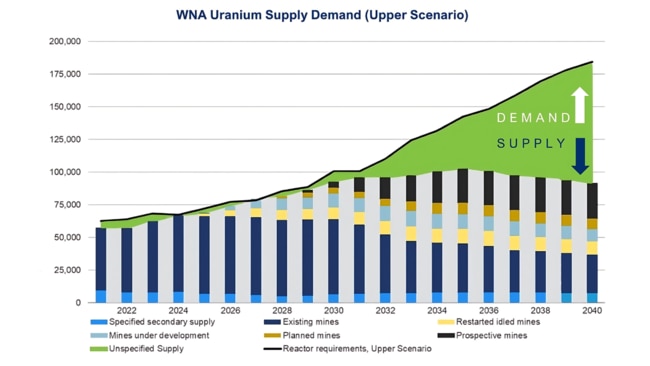

Nuclear power, seen as critical to global decarbonisation, is becoming mainstream again. Conservatively, CG expects capacity to expand at a compound annual growth rate of about 3.5 per cent to 2035, versus 3.2 per cent previously.

More power plants = increased uranium demand, which supply will struggle to meet.

Here’s why.

MORE FROM STOCKHEAD: Trinex’s Canadian adventure | Gold juniors wake up | Perfect timing for new REE projects

Supply is ‘fragile’

It is difficult to bring additional mine supply online at the best of times (an average of more than10 years from discovery to production, the experts reckon).

As it turns out, it’s also difficult for current miners to hit production targets.

“We cannot stress enough the fragility of primary mine supply,” CG says.

“This has become particularly clear in the past 12 months, which have been marked by several production downgrades from incumbent producers (Kazatomprom (LSE:KAP) and Cameco (NYSE: CCJ)).

“The most notable downgrade was KAP’s FY24 guide in early February, where it announced a 9Mlb downgrade due to acid supply constraints and delays at some of its newly developed deposits.”

That 9Mlbs a year is a lot; about 6 per cent of global production.

For context, fledgling producer Boss (ASX:BOE) will produce an initial 2.45Mlbs a year, while Paladin (ASX:PDN) is looking at peak production of 6Mlbs from the Langer Heinrich mine.

“We will be closely watching for a revision to KAP’s 2025 production target in August as the company has already flagged its 2025 target of 81Mlbs as ‘at risk’; we expect a material downgrade,” CG says.

Even mine restarts in 2024 – which CG expects to push supply up about 7 per cent to 150Mlbs per annum – won’t be enough to balance the market.

CG estimates a structural deficit of 22mlbs in 2024 and 16mlbs in 2025.

“’Difficult pounds will need to be developed,” it says.

Visit Stockhead, where ASX small caps are big deals

But the only greenfields (new) projects under construction are KAP’s Budenovskoye and Global Atomic Corp’s (TSX:GLO) Dasa.

And CG say both are facing delays.

“Other notable projects are still several years away from production when considering hurdles such permitting and financing.”

The biggest greenfields project on the horizon is Nexgen Energy’s (NYSE, TSX:NXE; ASX:NXG) large, high-grade Rook I operation in Canada’s Athabasca Basin, one of the world’s top uranium jurisdictions.

NXE is also a favourite of Argonaut’s fund manager extraordinaire David Franklyn and many other professional stock pickers.

Rook I – which Terra Capital’s Jeremy Bond calls “a geological freak”- will be the largest and lowest-cost uranium mine in the world, pumping out 30Mlbs a year.

Rook I will cost $C1.3 billion to build, but because of it’s high margins the payback period is expected to be only ~0.6 years — and that’s at $US50/lb.

At a $US100/lb uranium price, NXE could be making a monstrous $C3.4 billion each year in EBITDA.

But even this won’t be enough to touch the supply deficit, says the company, which requires “over five new Rook I sized projects to be found, permitted, financed and constructed over the next 20 years”.

Spot prices, uranium stocks to lift

Given extreme tightness in the spot market, CG “continues to believe that spot prices could trend higher over 2024 and model an average price of $US105/1b (+15 per cent versus previous)”.

“A re-evaluation of the cost curve has also driven us to increase our long term price assumption to $US90/lb, from $US75/lb-$80/lb previously.”

This mean CG’s favoured uranium equities have price targets that are, on average, 13 per cent higher.

“Our preferred equity exposures are NexGen Energy and EU in North America; Paladin and Lotus (ASX:LOT) in Australia; and KAP in the UK,” it says.

“For pure spot price exposure, we like U.UN (SPUT) and YCA.”

This content first appeared on stockhead.com.au

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

SUBSCRIBE

Get the latest Stockhead news delivered free to your inbox. Click here

Investor Guide: Energy FY2025 featuring Peter Strachan

In this special investor guide, capital markets veteran and resources analyst Peter Strachan leads Stockhead’s drill down into the ASX energy sector.

Investor Guide: Health & Biotech FY2025

In this special investor guide, health and biotech guru Tim Boreham leads Stockhead’s deep dive into the most cutting edge sector on the ASX.