HomeCo eyes expansion after IPO

The billionaire consortium behind HomeCo is eyeing expansion as it races to a $637m IPO.

The former Masters property empire, now known as HomeCo, is set to list on the ASX in October after raising $300m from investors keen to back the company’s growth alongside some of the country’s wealthiest families.

The group has flagged ambitions to expand in the resilient large-format sector that is holding up even as discretionary consumer spending falters and will see company chase out-of-the-box property deals while many listed real estate trusts veer away from the sector.

It will have former UBS investment banker David Di Pilla as its executive chairman and he will likely take a proprietorial approach as he holds an interest in about 30.6m shares, valued at about $102m, due to his majority ownership of the company’s major backer, Aurrum Group.

Mr Di Pilla will remain as executive chairman after leading the business for two years and, while he declined to comment on Monday, is heavily invested in the concept of hyper-convenience focused retail and services companies coming through the current retail onslaught in a stronger position.

HomeCo’s near $1bn portfolio comprises three types of centres split between daily needs, leisure and lifestyle, and homewares and electrical.

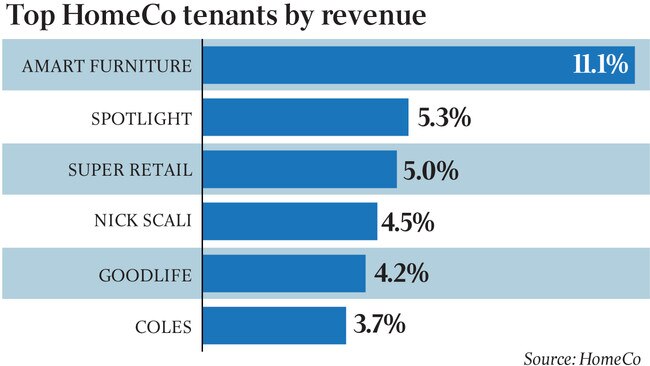

The areas are holding up even as department store and fashion sales slow with major tenants including Amart Furniture, IGA and Woolworths supermarkets, Decathlon, Super Retail Group, Spudshed, Nick Scali and PETstock, as well as Greenlit Brands, performing well.

The listing will pit some of Australia’s highest profile investors, including Chemist Warehouse millionaire Jack Gance and Melbourne billionaire Marc Besen, as well as retiring UBS boss Matthew Grounds who has a smaller stake, against the listed Aventus, backed by billionaire Brett Blundy, that is a major homewares landlord with a $2bn portfolio.

HomeCo had an offer price of $3.35 per share, giving it a market capitalisation of about $637m when it lists after a raising via joint lead managers Credit Suisse, Goldman Sachs and JPMorgan closed early.

The HomeCo consortium includes some of Australia’s top development and retail companies, with shareholders including Spotlight, Chemist Warehouse, Primewest and Aurrum.

The wealthy families, who were behind HomeCo when it bought the Masters’ property assets in 2017, after Woolworths won a legal stoush with Lowe’s, will retain their holdings after the float, giving them close to 49 per cent of the register.

Woolworths sold Masters’ 61 big box hardware stores and 21 development sites to HomeCo for $835m two years ago. The consortium sold off some assets, including to Bunnings, and turned the bulk of the sites retail centres.

By the end of 2019, HomeCo’s $925m portfolio will span 21 retail and services centres. A further nine centres will be redeveloped across Victoria, Queensland, NSW and WA.

All up, the group has land holding of about 1.14 million sqm, with two thirds of that area in growth suburbs in Brisbane, Sydney, Melbourne and Perth. The balance is in major regional centres.

The $300m raising and a debt refinancing will give HomeCo a war chest to expand via developing its existing sites, turning some leasehold properties into freeholds, and growing in the still buoyant convenience retail sector.

HomeCo also set out ambitions for acquisitions in corridors around major cities and is on the hunt for new sites. It is also looking at more lucrative uses at some sites, including town centre style developments, as well as funds management.

There is about 370,000 sqm of gross lettable area, showing a site coverage ratio of just 32 per cent, providing for future expansion opportunities. The group will start with firepower of about $150m available for its strategy, essentially funding it for the next three years.

Most rental income is underpinned by leases to national tenants and there is a long lease expiry of 8.8 years. HomeCo has forecast a fully franked dividend yield of 6 per cent until the end of next June.

Add your comment to this story

Robin Khuda lands site overlooking Balmoral Beach for $32m

The data centre billionaire behind AirTrunk is stepping up his high-end residential development on Sydney’s north shore. Khuda is expected to submit plans for a six-storey block with residences that will sport panoramic harbour views.

Take in valleys of vineyards from this Yarra Valley home

Built in 1975 and inspired by the bow of a ship this beautiful home includes four bedrooms, Miele-appointed kitchen, sheltered courtyard with pizza oven, and an 11,000-bottle cellar.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout