Census data delivers growth opportunities for canny investors

There are 20 areas that buyers need to look at if they want to get in on the ground floor of the next real estate boom.

Which towns on the Australian continent offer the best opportunities for property investors and developers and also for retailers and financial institutions?

Such towns must have critical mass, they must be growing, and they must contain a population base that is predisposed to household formation and consumption. But do such places exist? Most surely they do exist and now thanks to the results of the 2016 census it’s possible to identify these ‘‘perfect storm’’ consumer-spending markets.

We have accessed demographic data for the 100 largest towns in Australia from the 2016 and 2011 censuses. These towns range from Sydney with 4.5 million residents to Swan Hill with 9000. The dataset is known as the statistical urban area or SUA which considers only the contiguous built up areas. This definition of Sydney is tighter than the metropolitan definition which includes satellite settlements like the central coast and Blue Mountains and which push the city beyond the 5 million mark.

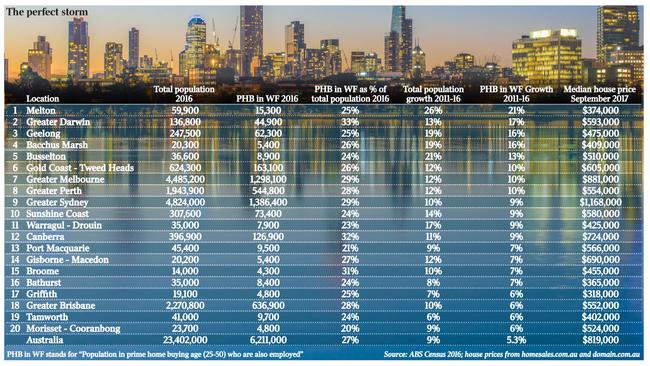

We have identified 20 cities and towns that we think present the perfect conditions underpinning housing and household demand. These cities range in scale from Broome with 14,000 residents to Sydney. Towns have been selected on the basis of the increase in the number of people in the workforce aged 25-50 between the last two censuses. It is argued that this 25-year age bracket represents the peak in household formation, in housing uplift and in household demand. This methodology delivers a large and growing segment of the workforce in the prime of the working life cycle that should create a perfect storm for spending.

At the national level about 27 per cent of the population falls within the 25-50 age bracket and is also within the workforce. In Canberra, where female workforce participation is unusually high, this proportion was 32 per cent at the 2016 census. In the lifestyle town of Port Macquarie on the other hand this proportion was 21 per cent. But it is growth in the number of workers within the 25-50 bracket that really drives spending. Whereas Australia’s total population jumped 9 per cent over the five years to 2016 the growth rate for workers aged 25-50 was 5 per cent.

The 20 perfect-storm consumer-spending markets each recorded more than 5 per cent growth in the key-worker population over this period.

The clear winner using this methodology to identify Australia’s best consumer-spending and household-formation town is Melton (population 60,000) on the western edge of Melbourne. Melton’s worker population aged 25-50 increased by 21 per cent between 2011 and 2016 which is four times the national average. This growth derives from the arrival of new householders with a job, from existing householders getting a job, and/or from young workers tipping into the spending zone aged 25-50.

Whatever the source the effect remains the same. The commuter town of Melton where house and land packages can be had for less than $400,000 is arguably Australia’s best household formation town. There may be parts of capital cities where growth in the ‘‘spending cohort’’ is greater but such markets merge and mesh with other adjacent markets. It gets all very messy to service. If you want a self-contained growing market in the household formation stage of the life cycle then look no further than Melton.

The table on this page sets out the 20 leading consumer-spending growth markets. They include all the capitals except Adelaide and Hobart in addition to a series of lifestyle cities and towns scattered across Australia. These include well known lifestyle cities like the Gold Coast and the Sunshine Coast but also Port Macquarie and Busselton. And then there are other growing towns that could be viewed as capital-city overspill communities such as Geelong, Bacchus Marsh, Warragul-Drouin and Gisborne-Macedon outside Melbourne, and Bathurst and Morisset-Cooranbong outside Sydney. Beyond these communities there are special towns that seem to be growing strongly within distinct regions such as Tamworth in New England, Griffith in the Riverina and Broome in the Kimberley.

There are no top-20 consumer-spending growth towns in South Australia or Tasmania and none in Queensland north of Noosa (Sunshine Coast). The figures that I do find surprising in this analysis relate to Perth in what is effectively the post-mining boom era. The number of 25 to 50-year-olds with a job in Perth increased by 9.7 per cent between 2011 and 2016, which is almost double the national average.

The Perth market may be subdued but there is no lack of growth in the cohorts that deliver consumer and household demand. The same logic applies to Darwin. The conventional wisdom is that house prices have fallen mightily since the peak of the boom in these cities but in both instances there has been strong growth in the key workforce cohort and at a rate that is double if not triple the national average.

If more and more 25 to 50-year-olds are pumping into the Perth and Darwin workforce and at nationally significant rates, then why is this not converting into a ratcheting up of housing demand? Or is this a case of these markets allowing recent spending growth to soak up excess capacity that was developed during the boom? And in which case the question is, when will a shortage of housing supply in these cities drive up prices? Either way it seems logical that the first signs of recovery from the collapse of the mining boom in the resources states will probably be a rise in median house prices.

In the meantime the main focuses of household formation and an uptick in consumer spending remain our biggest capital cities and selected commuter and lifestyle cities located on the seachange coast or within the tree-change zone. Troubled cities and regions do not make the list and nor do many “retirement towns’’ along the coast. Outside the capital cities and the Gold Coast and the Sunshine Coast the market offering most growth in the workforce population aged 25-50 between the last two censuses are Geelong (up 8500 net extra workers), Darwin (up 6400) and Melton (up 2700). But even in places like Bacchus Marsh and Warragul the increase in the key worker population between 2011 and 2016 ranged between 600 and 800, which would translate directly into housing and household accoutrement demand.

Australia is a vast continent with a series of pistons that never seem to all work in unison. But then neither do these pistons all completely stop. That’s the beauty and the frustration of doing business in Australia. You really do need to be across where the market is rising and falling.

Bernard Salt is managing director of The Demographics Group. Research by Simon Kuestenmacher.

bernard@tdgp.com.au

Add your comment to this story

Prosperity built on small biz

Nowhere is the small business sector the ‘backbone’ to the economy more so than in the construction industry.

Imported workers add tax value

Statistics prove our capital cities could not have functioned efficiently without the contribution of foreign-born workers.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout