This was published 3 years ago

The central bank under fire: Has the RBA failed Australians?

The role and importance of the central bank is little understood, but a number of economists and experts are claiming it has failed the country.

By Shane Wright

Credit:

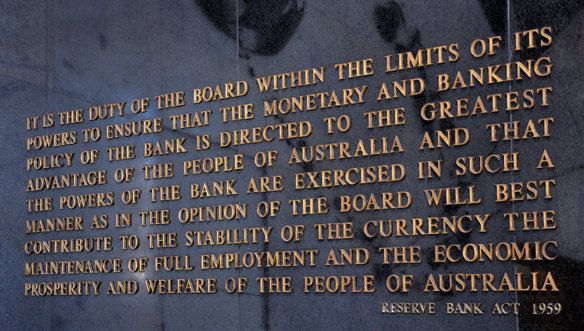

Struck in bronze and attached to a dominating piece of stone in the foyer of the Reserve Bank’s headquarters in Sydney’s Martin Place is the bank’s charter.

Every day, as bank staff enter the building, they are reminded of the central bank’s critical functions.

Those functions are to direct bank policy to the “greatest advantage of the people of Australia”. It is to do that through three key actions: maintaining the stability of the currency, ensuring full employment and furthering the “economic prosperity and welfare of the people of Australia”.

Staff are reminded of the RBA’s critical functions via a plaque quoting the bank’s charter in the foyer of the bank’s Martin Place headquarters.Credit: RBA

Upholding these objectives has a tremendous impact on the economy, from a family trying to afford their mortgage, to a business considering a pay rise for their staff.

As Australia enjoyed a near 30-year stretch of unbroken economic growth before last year’s recession, the bank and its policy settings were often overlooked by politicians of all persuasions looking to take credit.

Apart from when it changes official interest rates, the role and importance of the RBA is little understood or even acknowledged. But the bank is now facing rare criticisms by leading economists, former treasurers and monetary policy experts who believe the bank failed the country and hundreds of thousands of people by holding interest rates too high for too long ahead of the pandemic.

Some experts even believe bank governor Philip Lowe should resign and the RBA board should be overhauled. They warn the economy could be undermined long term by poor monetary policy settings even as Australia continues to stun the world with its post-pandemic economic performance.

The RBA is facing rare criticisms from economists, some of whom believe RBA governor Philip Lowe should resign over what they say are recent failures.Credit: Dominic Lorrimer

But defenders of the bank and of Dr Lowe say the attacks are unfair and ignore problems central banks across the world faced before the advent of COVID-19. They argue the policy prescriptions of critics would fail to deliver their desired outcomes.

The Sydney Morning Herald and The Age today begin a special series on the Reserve Bank, monetary policy and the state of the economy. The series focuses on the bank’s pre-pandemic policy stance and the challenges it faces in the pandemic’s wake. It is based on interviews with former bank governors, former treasurers, former board members and respected monetary policy experts. The RBA declined a formal interview but answered questions based on public statements made by senior staff over recent years.

Missing key targets

Since the early 1990s, the bank has set official interest rates with an eye to meeting its charter of holding the rate of inflation between 2 and 3 per cent, on average, over time. But even before last year’s pandemic, the bank had failed to meet its own target each year since 2014. Based on its current forecasts, inflation will still be short of the 2 to 3 per cent band when Dr Lowe’s term as governor is due to end in 2023.

Economic growth through the second half of the 2010s slowed. GDP per capita averaged less than 1 per cent a year and wages growth edged down to a then-record low. The country enjoyed near-record jobs growth but unemployment only fell from 6.3 per cent to 5.1 per cent. The last time under-employment, which measures the proportion of people wanting more hours, was under 8 per cent was in January 2014.

Between August 4, 2016 and June 4, 2019, the bank held official interest rates at 1.5 per cent. It became the longest period of time the bank held rates unchanged on record. As late as the end of 2018 it was signalling its next move would be an interest rate increase, before it decided to cut rates in June 2019 after that year’s federal election.

It went into the pandemic recession with official interest rates at 0.75 per cent while calling on all levels of government to increase spending on infrastructure projects to help boost economic activity and lift wages.

Soon after the June interest rate cut, Labor frontbencher and economist Andrew Leigh used a parliamentary committee hearing to ask Dr Lowe if the bank had “comprehensively failed” to meet its inflation target. Dr Lowe rejected the claim, but admitted the bank had faced some “difficult challenges” in setting monetary policy, and pointed to a global slowdown in the second half of 2018.

That was attributable in large part to the trade war started by then-US President Donald Trump with China, which caught central banks around the world off-guard.

Locally, the RBA was also surprised by one of the more startling economic trends of the decade. Jobs growth was exceptionally strong between 2016 and 2019, driven by a huge step up in the number of both women and older Australians entering the workforce.

Between mid-2016 and mid-2019, the number of Australians in work increased 7 per cent or 892,000 people. Among women aged between 55 and 64, the increase was 11 per cent. Among women aged 65 or above, the increase was 29 per cent.

The jump in employment meant employers did not have to offer higher wages to entice people into the workforce and a key element to the RBA’s plans - wages growth driven by a tight jobs market - failed to materialise.

Another issue, which was not mentioned at the time by the bank, was the drop in house values across 2018 after they soared the year before.

In the year to the end of July 2017, Sydney’s house values had climbed by 14.9 per cent. Melbourne’s had lifted by 14.4 per cent. Twelve months later, Sydney’s house values had fallen by 6.3 per cent while Melbourne’s were down by 0.9 per cent.

Tighter lending standards imposed on commercial banks had slowed the nation’s two largest property markets. What was important for the stability of the financial sector, however, had come at the price of the “wealth effect” that accompanies ever-increasing house values.

When looser mortgage serviceability buffers on banks were put in place by the Australian Prudential Regulation Authority in mid-July 2019, the impact on prices was immediate. Values in Sydney and Melbourne, as measured by CoreLogic, jumped by 2 per cent inside a month.

The low-interest rate environment hasn’t just helped push up house prices. Other asset classes such as shares have boomed. This has led to criticism that monetary policy is contributing to inequality because the benefits of these higher asset values tend to flow to the wealthier people who own multiple houses and share portfolios.

The bank’s core argument is that these three issues – Trump’s trade war, the surge in workforce participation, the drop in house values – meant its expectations of a lift in inflation and wages growth did not eventuate. They were on top of “structural” issues that were hitting the economy and wages, including technological developments, the ageing population and reduced power for unions and workers.

By June 2019, it had decided on a new course of action that would ultimately result in three quarter percentage point rate cuts that took the cash rate to a then-record low of 0.75 per cent.

But to critics, the explanations are excuses. And they fail to explain how the bank was failing to meet its own inflation target before 2016. Former prime minister Paul Keating, who has likened the RBA to a monastery, says the bank failed working Australians.

“The failure of monetary policy was its failure to secure growth sufficient to witness demand for labour spill into wages – into real wage growth,” Keating says.

“Instead, the RBA pursued a cautionary policy against nascent inflation while, at the same time, Australia and the world navigated the continuing phenomenon of deflation. This conservative policy overvalued the exchange rate, suppressing economic activity and with it, an underutilisation of labour which effectively nailed wage growth.”

Blueprint Institute chief economist, assistant professor of economics at George Washington University and former Treasury official Steven Hamilton is brutal in his assessment.

“If one of my employees had failed to achieve his KPI for half a decade, I would long since have sacked him. Any excuse he had might be credible if Lowe had actually tried,” he says. “The governor’s apparent obsession with ‘financial stability’ - house prices - yielded an overly hawkish monetary policy regime responsible for the loss of perhaps hundreds of thousands of jobs.”

Blueprint Institute chief economist Steven Hamilton.

Research by former RBA economist Zac Gross, who lectures in economics at Monash University, suggests the failure of the bank to hit its inflation target cost the country the equivalent of 2.5 per cent of GDP and an extra 90,000 jobs.

He noted between February 2016 and May 2019, the bank cut interest rates just twice across 37 separate board meetings despite core inflation being below the RBA’s own target the entire period.

The inflation headache

The Reserve Bank’s inflation target was borne out of the lived experiences of the 1970s when soaring inflation accompanied high unemployment.

Between 1975 and 1980, inflation reached a high of 17.7 per cent and never got below 7.6 per cent. Unemployment, which had been below 3 per cent for years, more than doubled to 6 per cent through the period. Central banks around the world reacted by focusing their attention on reducing inflation. By 2007, the war on inflation had been “won”.

The problem for the Reserve Bank, and central banks everywhere, is that inflation has been too low since the global financial crisis, which started in 2008. While out-of-control inflation is a devastating economic problem, the absence of inflation can also be a major economic headache.

AMP Capital chief economist Shane Oliver, one of the few economists to predict the bank would start cutting rates in 2019 even as the RBA was signalling they would go up, says there were major economic repercussions from ongoing monetary policy failure.

“If it continues to underperform, it means ongoing low wages growth ... it means people stuck with larger mortgages that will take longer to pay off, meaning more people using their superannuation to pay off those mortgages,” he says.

It’s a particular risk for Australia, which has some of the highest household debt in the developed world. Almost all of that debt is tied to super-sized mortgages. A person taking out an average mortgage can reasonably expect the relative size of their repayments to fall over time. That’s due to the repayments making up a smaller proportion of their take-home pay, which should increase as wages lift, pushed along by inflation.

But if wages only grow marginally, the mortgage repayments weigh on that person’s finances for longer. And while Australians have increased their debt holdings, wages growth has virtually come to a standstill.

Work by the independent Grattan Institute shows average full-time wages rose by 4.7 per cent a year between 2000 and 2012. Between 2012 and 2020, this had fallen to 3 per cent a year.

Brendan Coates of the Grattan Institute believes the RBA’s commitment to “financial stability” in 2016 was a major mistake.

Former Treasury and World Bank official Brendan Coates, who is Grattan’s household finances program director, says the nation’s macroeconomic policy framework was under strain even before the COVID pandemic.

“Both unemployment and under-employment were substantially higher than they could have been, and hence the pace of wage rises for Australian workers has slowed,” he says.

“Our research suggests that Australia’s poor macroeconomic performance pre-COVID accounts for at least half the slowdown in wages growth seen since 2012.”

The RBA’s ‘financial stability’ commitment

On top of the RBA’s charter and its inflation target is an agreement between the Treasurer of the day and the bank’s governor, called the statement on the conduct of monetary policy.

In 2016, when Dr Lowe became governor, he and then-treasurer Scott Morrison signed an updated statement that included an overt commitment towards “financial stability” as well as the 2-3 per cent inflation target.

Coates is among many who believe the inclusion of financial stability was a major mistake, which was not properly understood by the government at the time. He argues it forced the bank into trading off the economy’s overall performance against unquantified concerns about the banking sector.

“Fear of financial instability appears to have led the bank to keep interest rates higher than the inflation outlook alone justified, with disastrous results,” he says.

Policies put in place during COVID aimed at the property market, including record-low interest rates, have contributed to an explosion in debt for first-time buyers.

The average new loan for a first-time buyer in NSW has climbed from $430,000 in January 2019 to $522,500 this January. In Victoria, it has climbed to $451,000 from $390,000.

University of Melbourne economist Chris Edmonds, who worked at the RBA in the late 1990s, says the central bank’s failure to meet its inflation target has real-world implications for all Australians. If inflation averaged 1.5 per cent rather than 2.5 per cent for a decade, the overall price levels in the economy would be 12 per cent lower than otherwise.

“The real burden of household debt is increased by 12 per cent relative to a world where the RBA delivered 2.5 per cent inflation,” he estimates.

Another criticism is that by holding interest rates too high for too long, the economy was in a softer position than it should have been when last summer’s fires hit and then the pandemic. A stronger economy may not have needed as much fiscal support to get through the recession.

Peter Tulip, who left the bank last year and is now the chief economist at the Centre for Independent Studies, says the pre-virus position of the RBA was clearly a policy mistake.

“We went into the pandemic in the wrong place. Unemployment at around 5.5 per cent was too high. If we had unemployment around 4 per cent then the situation would have been different,” he said. “[The RBA] has failed in its objectives. It’s right that different central banks have had similar issues and that’s a legitimate concern that they have failed just like their peers.

“If the objective was to not stuff up just as much as their peers then that’s a strange definition of success.”

One of the nation’s most well-known economists, Ross Garnaut, is just as blunt. He says the “dog days” of economic performance between 2013 and 2019 was due in part to interest rates being held too high for too long.

“Low-income people have been hurt most by wrong policy settings,” he says.

Did we need negative rates?

Independent economist Saul Eslake agrees the bank had “clearly” failed to meet its inflation target, but adds critics of the RBA fail to recognise the major problems it faced trying to meet that target.

He says the bank’s failure to cut interest rates further during the pre-virus period was driven by four other factors - the problems other central banks were having with the same issues, a failure of the entire economics profession’s understanding of emerging global issues, the impact of fiscal policy and a jump in asset prices (like houses) partly fuelled by government policy.

“In the aftermath of the global financial crisis, central banks have reached the limits of what they can do,” he says.

Saul Eslake says “central banks have reached the limits of what they can do”.Credit: Louise Kennerley

Research by the Grattan Institute backs the claim all major central banks have struggled to meet their inflation targets over the past decade, but only Japan has done worse than Australia.

Others such as the euro-area, New Zealand, the United States and Canada have all been much closer for longer to their inflation targets than the RBA.

Ahead of the pandemic recession, the bank fiercely resisted an option adopted by many central banks overseas to take official interest rates negative. Mr Eslake says negative rates were a “dopey idea” that the RBA was right to resist.

“Those central banks that had negative rates going into the recession haven’t cut their rates any further. If you thought negative rates were the right idea, why wouldn’t you go further?” he said.

But research by the International Monetary Fund earlier this year found negative rates had worked in stimulating inflation in countries such as Denmark, Japan, and Switzerland.

“Negative interest rate policies have proven their ability to stimulate inflation and output by roughly as much as comparable conventional interest rate cuts or other unconventional monetary policies,” the research found.

“They also led to lower money-market rates, long-term yields and bank rates.”

One concern about negative rates is that depositors will rush to take their money out of a bank for fear of seeing their savings disappear. But the IMF research found this has not occurred, for both corporate deposits and mum-and-dad savings.

“Bank lending volumes have generally increased. And since banks nor their customers have markedly shifted to cash, interest rates can probably become even more negative before that happens,” it found.

While the Reserve Bank has pressed back against critics, it has admitted there were policy alternatives. During his exchange with MPs back in 2019, Dr Lowe conceded “other people might have made different decisions”.

“Part of the reason that we decided not to lower interest rates during that time, to get inflation up a bit more quickly, was the judgement that ... it would encourage more borrowing and higher housing prices in an environment where there was already a lot of exuberance in the housing market,” he said.

Former RBA board member and Keating economics adviser John Edwards, says the bank’s struggle to meet its inflation target had been offset by exceptional jobs growth.

“The last downturn was 29 years ago, so I think we should be pretty happy with how monetary policy has worked over that period,” he says. “We can have an argument about whether the bank should have cut lower or faster, but it probably wouldn’t have made much difference.”

Bernie Fraser, the former RBA governor who instituted the inflation target that has guided the RBA since the early 1990s, says critics were ignoring how well the bank has performed.

“We had 30 years of consecutive growth with the Reserve Bank a key reason for that,” he says. “It’s really held the country together over that 30 years, it’s a Winx-like performance over 30 years with sustainable economic growth.”

Mr Fraser says while the bank had under-shot its inflation target over recent years that had to be weighed against the continued growth in the economy and strong jobs creation.

Former Reserve Bank governor Bernie Fraser says the RBA is a key reason for 30 years of consecutive economic growth.Credit: Alex Ellinghausen

Complicating the RBA’s efforts was fiscal policy, with Mr Fraser noting fiscal and monetary policy had “got out of kilter” during the pre-global financial crisis mining boom.

“The government was pushing money out through tax cuts to households and businesses. Some of it went into the Future Fund but a hell of a lot of it went to individuals and companies,” he says.

“That meant the Reserve Bank had to tidy up after them. We saw that as the bank lifted interest rates to keep a lid on inflation. The bank really held the show together.”

Fiscal policy headwinds

The problems that confronted the bank before the pandemic are likely to return in the post-pandemic world.

The RBA has official interest rates at a record low of 0.1 per cent and is now engaged in a quantitative easing program that includes purchasing at least $200 billion worth of state and federal government debt.

In recognition of the pre-pandemic issues, Dr Lowe has made clear the bank will hold interest rates at their current level until unemployment is around 4 per cent, wages are growing strongly and inflation is within its target band.

Dr Lowe has said rates could stay at 0.1 per cent until 2024, while some private-sector economists believe it could be years longer before wages and unemployment are at the levels sought by the RBA.

But the bank’s plan to keep exceptionally loose monetary policy faces headwinds from the Morrison government and its own plan for fiscal policy.

Treasurer Josh Frydenberg wants to lower the budget deficit, a move many economists argue against.Credit: Dominic Lorrimer

Treasurer Josh Frydenberg has promised that once unemployment is “comfortably” below 6 per cent then the government will make a deliberate shift to “stabilising gross and net debt as a share of the economy”.

Internally, this is seen as a plan to start spending cuts once the jobless rate is around 5.5 per cent.

The gap between the RBA’s desired unemployment rate of 4 per cent and the government’s plan to start tightening fiscal policy at a 5.5 per cent jobless rate translates into about 350,000 people. That does not include the hundreds of thousands of under-employed people who want more hours of work every week.

Mr Eslake says with interest rates so low, the federal government should use its balance sheet to boost economic activity so the RBA can prepare itself for the next inevitable downturn.

“For the next 5 years we ought not to rebuild our fiscal buffers. We need the Reserve Bank to rebuild our monetary policy buffers so that it can respond to a future shock,” he says.

“Instead of Josh Frydenberg saying that he will start budget repair when the unemployment rate is under 6 per cent, he should say it won’t start until unemployment’s under 5 per cent.”

Even now, one of the first questions asked in RBA board meetings is “what’s going on with fiscal policy?” .

Mr Fraser says with official interest rates at zero, the traditional weapon of central banks to grow the economy had been neutered. This meant far more economic heavy lifting had to be done by governments.

“Monetary policy is very broad, it can’t be aimed at particular regions or industries or people. But fiscal policy can,” he said.

“There’s more of a burden on fiscal policy now than on monetary policy.”

Several experts say the bank’s efforts through 2016 to 2019 were undermined by the governments of Malcolm Turnbull and then Scott Morrison as they sought to slash the budget deficit.

In 2015-16, the deficit was $39.6 billion. Two years later it was down to $10.1 billion while in 2018-19 there was a shortfall of just $700 million - within touching distance of the first budget surplus in more than a decade. By any measure, this was a tightening of fiscal policy. But it’s nothing compared to what the government is planning.

This year’s budget deficit is, given strong iron ore prices, likely to fall well short of the forecast $197.7 billion but by any measure, it will be the largest ever recorded by the federal government. Next financial year’s deficit is forecast to be $112 billion before edging down to $84.4 billion the year after.

It’s the largest deficit reduction on record. It would surpass the contraction in government spending at the end of World War II which led to a mild recession. But with the RBA unable to lower interest rates to cushion the impact of tighter fiscal policy, there is real concern a government rushing to reduce spending could induce its own economic downturn.

Dr Edwards says the smaller budget deficit will be a major issue.

“My rule of thumb is that if the deficit is falling, either in dollar terms or as a share of GDP, then fiscal policy is contractionary. Treasury might be reluctant to admit that but it is true,” he says.

Former board member and respected economist Warwick McKibbin says government failure left the RBA to do too much. He says while the bank talked extensively about ways to boost productivity it was outside the RBA’s control. It was an issue clearly within the remit of government.

Economist Warwick McKibbin.Credit: Louie Douvis

Dr McKibbin, well known for his work on climate policy, says without faster nominal economic growth debts accrued dealing with the coronavirus recession will never be repaid. He advocates a major investment in climate-related infrastructure.

“You need everything to work together. If you target inflation you won’t get the growth,” he says. “It’s not just the Reserve Bank, it’s also fiscal policy. A central bank just printing money doesn’t get the economy really growing.

“You need something that is real. And that’s where infrastructure around climate change really could make an economic difference.”

Mr Keating, who came under criticism as prime minister for the government’s relatively slow response to the 1990-91 recession, warned against premature fiscal policy tightening.

“If people have learned anything from this episode it is of the limitation of monetary policy,” he says.

Read more of this series here: