Uncertain times ahead for Australian house prices as boom sparks concern among the big banks

House prices across Australia continue to soar to insane levels despite lockdowns, and unlikely voices are warning it’s out of control.

At the start of the coronavirus pandemic, as the world teetered on the edge of unprecedented uncertainty, economists issued a dire prediction for Australia’s housing market.

It would experience huge losses unlike anything we’ve seen in modern history, with estimates ranging from a 10 per cent slump right up to a devastating 30 per cent collapse.

And yet, despite mass job losses, widespread lockdowns, the shuttering of the economy and a resulting recession, and the disruption of trade, those forecasts never eventuated.

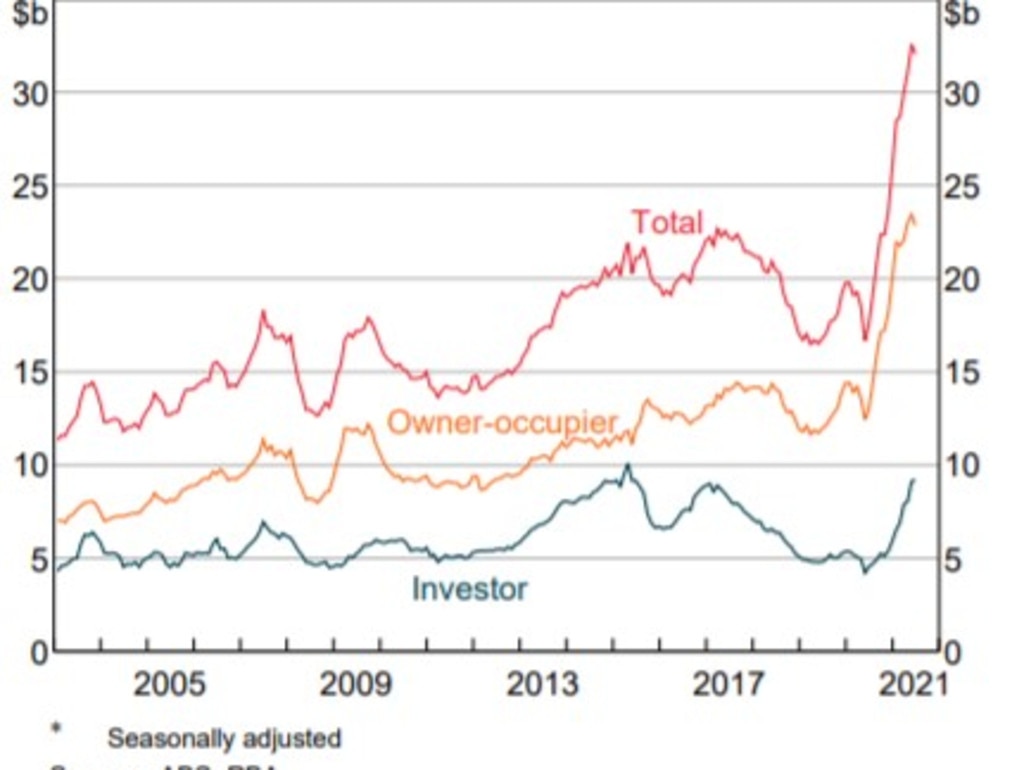

In fact, median housing values across Australia have surged 15.8 per cent over the first eight months of 2021, and are 18.4 per cent up over the past year.

Prices are higher than they were before anyone knew what Covid-19 was and have grown at the fastest annual pace since 1989.

“In dollar terms, the annual increase in national dwelling values equates to approximately $103,400, or $1990 per week,” CoreLogic research director Tim Lawless said.

Apart from those trying to get on the property ladder and struggling, most other players in the market would be celebrating the historic upward movement of the market … right?

This week, an unlikely voice joined the growing chorus of concern over the continuing boom, which has continued during lockdowns in the two biggest markets of Sydney and Melbourne.

Commonwealth Bank chief executive Matt Comyn said he’s growing “increasingly concerned” by the rapid growth of prices in virtually every city, as well as across major regional areas.

Despite being the nation’s largest bank and biggest lender of loans for home purchases, meaning it’s raking in the cash, Mr Comyn told a parliamentary hearing the bank wanted to see steps taken to “take some of the heat out of the housing market”.

Prices still growing, but slowing

National housing values road again by 1.5 per cent in the month of August, with the largest market of Sydney up 1.8 per cent, CoreLogic’s index reported.

That rate of growth for the New South Wales capital is despite the city being in an extended period of lockdown, with property inspections only available by appointment and limited to one person at a time, and auctions conducted online only.

Similarly, in Melbourne, also in the midst of yet another lockdown, prices still rose by 1.2 per cent – a modest increase, but in the context of the covid landscape, impressive nonetheless.

“In the significant period of lockdown in Sydney, Melbourne, we have seen big falls in consumer and business confidence, as you would expect,” Mr Comyn said on Thursday.

“I’m not seeing much of a slowdown in terms of (mortgage) applications and funding. You can see the market is still very active.”

Elsewhere, the strongest gains in August were seen in Hobart, up 2.3 per cent, Canberra, up 2.2 per cent and Brisbane, up 2.0 per cent.

“Australian housing values continued to record a broadbased rise despite the disruption from lockdowns,” Mr Lawless said.

However, the August results provide further signs that the rate of price growth is starting to slow after moving through a peak in March, he said.

“At that time, national home values had risen 2.8 per cent in a month, led by Sydney where dwelling values were up 3.7 per cent.”

That slowing over the past several months probably has more to do with affordability than it does Covid-19 restrictions or significant uncertainty.

“Housing prices have risen almost 11 times faster than wages growth over the past year, creating a more significant barrier to entry for those who don’t yet own a home,” Mr Lawless said.

“Lockdowns are having a clear impact on consumer sentiment, however to date the restrictions have resulted in falling advertised listings and, to a lesser extent, fewer home sales, with less impact on price growth momentum.

“It’s likely the ongoing shortage of properties available for purchase is central to the upwards pressure on housing values.”

Despite lockdowns and restrictions on the real estate industry, auction clearance rates – that is, the proportion of listings to sell under the hammer – remains high.

According to CoreLogic, 1835 homes were taken to auction across each capital city last weekend, up strongly on the previous week and almost double the number the same time 12 months ago.

The national auction clearance rate was 74 per cent, while Sydney led the individual market charge with a 82 per cent result.

Volumes are low though, especially in Melbourne where 56 per cent of the 560-odd properties that went under the hammer sold successfully, indicating many sellers are sitting tight at the moment.

A sign of trouble ahead

The head of a big four bank talking down house price growth and even calling for measures to slow it down is obviously significant.

And it’s an indication of what could lie ahead for the real estate sector – a critically important pillar of the economy – if things continue unabated.

Speaking on Thursday at a parliamentary hearing, Mr Comyn was asked about residential property price growth when he said: “We think it would be important to take some modest steps sooner rather than later to take some of the heat out of the housing market.

“I think it would be prudent to act sooner rather than later.”

What’s just occurred – an almost 20 per cent explosion in national house prices – isn’t what’s giving him cause for pause though.

“I am not concerned about the period just gone. But in terms of increasing housing debt and increasing house prices we are increasingly concerned.”

Also appearing at the parliamentary hearing was ANZ boss Shayne Elliott, who also expressed his concern about Aussies who might be biting off more than they can chew.

“There has been an increase in the number of people who are taking on more debt relative to their income,” Mr Elliott said.

“We’re taking more time to be careful, to ask more questions, to really assess whether people have the capacity to take on the debt they would like (and) we’ve lost a bit of market share because of it.”

The Reserve Bank has also indicated its growing unease, saying ever-higher house prices and subsequent household debt is seeing “risks to financial stability … building”.

In a speech this week, RBA assistant governor Michelle Bullock, who’s in charge of monitoring the nation’s fiscal stability, said the level of debt homeowners enter into is enormous thanks to house prices.

That means, a major event like an employment downturn might be worse-felt as a result.

“For example, in a recession in which a large number of indebted households suffer reduced income, from say a loss of employment or reduced hours, they might choose to reduce their consumption,” Ms Bullock said.

“It may be just precautionary. But if households are constrained, in the sense that they don’t have a great deal of income left after meeting their debt servicing requirements and the basics of their lifestyle, they are more likely to reduce consumption.

“This will amplify the initial impact of the economic shock.”

She said the RBA was constantly assessing whether intervention is needed to address the risk.

“Even though the banks have strong balance sheets and lending standards are being maintained, there is a risk that, in this environment, households will become increasingly indebted,” Ms Bullock said.

“A high level of debt could pose risks to the economy in the event of a shock to household incomes or a sharp decline in housing prices. It is these macro-financial risks that warrant close watching.”

CBA taking proactive steps

Another bombshell dropped by Mr Comyn on Thursday was that his bank had lifted its serviceability floor in its own attempt to cool the market.

That means, the rate at which a bank tests a person’s ability to continue repaying their mortgage if interest rates rise has been brought up for Commonwealth Bank customers.

Currently, the official interest rate in Australia is at an all-time low of 0.10 per cent, making the cost of borrowing money extremely cheap.

Those low borrowing rates are contributing to the rush on property, as well as a quicker-than-expected rebounding of consumer confidence, the FOMO (fear of missing out) factor, and pent-up demand.

While there’s no immediate indication that rates will begin an upward climb, they will eventually.

“I think we all would have our share of concern about making sure that Australia’s households are in a strong position to continue to repay, but also support broader consumption in the economy in the second half of this decade if interest rates are rising, and if potentially they would rise more quickly,” Mr Comyn said.

For now, few people are losing out as a result of skyrocketing prices in virtually every part of the country — except one significant group.

Younger Australians are facing conditions that “make it harder to enter into the housing market”, Mr Elliott said.

Being completely priced out will lead to long-term economic disparity in the future, he warned.

ASX lifts despite US, China turmoil

A surge in technology and real estate stocks helped drive the ASX 200 higher, despite fears of a slowing US and Chinese economy.

Why Aussies could spend more on mortgages

Struggling mortgage holders will get a rate cut in May, but are now tipped to get less over the rest of 2025, an industry expert warns.

‘Savage cuts’: Coalition’s costings slammed

With just two sleeps to go until the federal election, the Coalition has finally released its costings, drawing fire from Jim Chalmers.