There’s a cost of living crisis – but Aussies can’t stop spending

We’re in the middle of a financial crisis, yet Australians aren’t doing what they’re meant to in order to lower inflation – and it could be disastrous.

Business

Don't miss out on the headlines from Business. Followed categories will be added to My News.

As inflation continues its resurgence throughout the world, central banks are being turned to once more to fulfil their role as the chief driver of inflation fighting efforts.

While there is a strong argument to be made that tightening fiscal policy, aka cutting government spending or raising taxes could also play a major role in fighting inflation, it’s a level of political kryptonite almost no government is willing to touch with a fifty-foot pole.

But as central bankers prepare themselves for what could be a very long battle to tame inflationary pressures, it’s worth noting that there are factors that could undermine their efforts significantly and change the game dramatically.

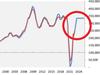

Consumer confidence has plummeted

When Australia rang in 2022, the ANZ-Roy Morgan Consumer Confidence Index had a four-week moving average of 107.5. While this was still well below the index average over the past 21 years, it was at least within shouting distance of levels that could be considered normal.

Want tips to help manage the rising cost of living? Read Compare Money's guide >

Since then, it has fallen by almost 25 per cent to sit at just 81.1. While this is above the levels recorded in the dark days of the early weeks of the pandemic’s impact on Australia, this level still represents an absolute collapse from levels that would have been considered anything approaching normal pre-pandemic.

It’s a similar story for Westpac’s Consumer Confidence Index. With the exception of the initial pandemic shock, it is recording its lowest level since the years following the 1990s recession.

Under more normal circumstances the relationship between consumer confidence and consumer spending is clear, if confidence falters so too in times does spending.

But that hasn’t happened this time, quite the opposite in fact. In year-on-year terms, retail sales are up 12.5 per cent, indicating that the appetite of Aussie consumers remains relatively robust in aggregate.

Feast and famine for Aussie households

Despite household spending in aggregate holding up extremely strongly, this perspective somewhat overlooks the challenges faced by many Aussie households as rising interest rates and falling inflation adjusted incomes continue to bite.

According to an October report from Foodbank Australia, 21 per cent of households are severely food insecure, with a further 12 per cent moderately food insecure.

The study defined ‘Severely food insecure’ as reports of multiple indications of disrupted eating patterns and reduced food intake. ‘Moderately food insecure’ was defined as reports of reduced quality, variety or desirability of diet, little or no indication of food intake.

When it comes to households putting aside cash for a rainy day, it’s a similarly concerning story for a sizeable number of Australians. According to a June survey from Canstar, roughly two-in-five people have no savings set aside for urgent or unexpected costs.

A thorn in the RBA’s side

Despite widespread reports of millions of Australians struggling with rising rates and the cost of living, there is precious little sign that the RBA’s efforts to tame inflation will be successful any time soon.

In the United States, there are clear signs that consumers are slowly running out of scope to keep up with the rising cost of living. For example, the personal savings rate in the US has fallen from a little over 9 per cent prior to the pandemic, to sit at just 3.1 per cent, within striking distance of all time lows.

The overall aggregate balance of US household savings continues to rise, however, it’s widely believed that this is largely driven by the wealthy continuing to amass cash, while low- and middle-income households are burning through their savings.

Meanwhile, in Australia, the household savings ratio is 8.7 per cent and remains significantly above the 7 per cent recorded prior to the pandemic. According to data from banking regulator APRA, the overall pile of household savings continues to grow rapidly.

In the United States, consumers turning to savings has supported activity within the economy for well over a year and helped to keep inflation high, despite the fact that the US experienced a technical recession during that period.

Turning to the plastic

In the US, consumers have turned to credit cards and other forms of revolving credit in order to keep up with the rising cost of living, adding over $US100 billion ($A146 billion) to balances in the past 12 months of data alone.

In Australia, we have recently seen a significant uptick in credit card spending, with September experiencing the largest seasonal expansion in credit card balances since records began in 1985, with households adding more than $205 million to their collective balances in net terms.

To put levels of Australian credit card debt into a more long-term perspective, the current level of outstanding credit card debt to GDP is less than half of what it was at its peak in 2008.

However, when you look deeper at the level of credit card balances that are actually accruing interest, rather than Australians cleverly playing the system for points or interest free periods, outstanding balances as a proportion of GDP falls to just 0.9 per cent.

The Outlook

Putting all these pieces of the puzzle together, it’s clear that if Australians want to keep up their spending there is more than enough savings and scope to grow credit card balances for them to do so.

This puts the RBA in a rather challenging position, if it can’t swiftly and sufficiently contain aggregate demand, inflation may remain higher for longer and necessitate higher interest rates.

While many households are being driven to the wall by rising costs, in our little corner of the world, inflationary pressures may remain high for as long as Australians choose to keep spending. With pandemic-driven demand still a major factor and some households doing better than ever, it could be quite some time before Australians reach that point.

Tarric Brooker is a freelance journalist and social commentator | @AvidCommentator

Originally published as There’s a cost of living crisis – but Aussies can’t stop spending

Telstra under fire over China ‘sabotage’ fears

Tensions were high at Telstra’s annual general meeting, with shareholders urging the board to address fears Australia’s mobile network could be sabotaged.

‘Fiddling’: Surcharge crackdown lashed

A crackdown on card surcharges has been criticised as “fiddling around the edges while Rome burns”.