Super caps and mortgage buffers spell double trouble for property

Homebuyers and investors face new roadblocks in the residential market as government policies reduce the supply of new stock.

Business

Don't miss out on the headlines from Business. Followed categories will be added to My News.

Just as the rental crisis is set to deepen thanks to a looming cap on superannuation, the banking regulator has sidestepped a chance to alleviate pressure in the property market.

The Australian Prudential Regulation Authority has refused to budge and will continue to insist that banks add 3 per cent on top of the prevailing interest rate when assessing mortgage applications. The announcement comes despite industry calls for a review of pandemic era ‘serviceability buffers’.

The move to effectively extend the buffer rules will keep potential owner-occupiers out of the market, while the government’s plan to cap money held in super at $3m is set to drive Self Managed Super funds away from residential property investment.

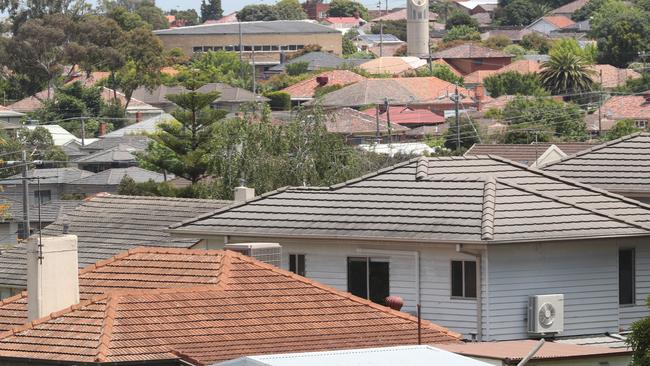

It’s an unfortunate combination for renters just as residential vacancy rates have got worse. With recent industry data showing the major cities are now back at 1 per cent vacancy rates, we face the tightest market seen in decades, with asking prices are rising by 30 per cent a year.

Yet, even with falling property values, there are few signs of bargain hunters in residential property due to mounting uncertainties – many of them linked to changing government policy.

There is an estimated $48bn worth of residential property held by Self Managed Super Funds, but the government’s plan to impose a cap at $3m – against earlier suggestions of $5m – is set to destabilise the market, with fears of forced sales.

The outgoing chief executive of the SMSF Association, John Maroney, is hoping the government will move towards a tax change rather than a hard cap in the weeks ahead.

“If there must be a change we would prefer a tax change instead of a rule where property must be removed from the super system – nobody should be forced to sell property, especially in difficult markets,” he said.

An alternative to the hard cap would be a lifting of the tax rate paid by individuals who have more than $1.7m in super from the current rate of 15 per cent. Such a change would introduce a third tax rate inside the super system – zero for amounts up to $1.7m, 15 per cent up to $3m, and a new higher figure over that level.

Meanwhile, in its latest information paper published on Monday, APRA chairman John Lonsdale said current buffers “remained appropriate given the potential for domestic and global economic conditions to deteriorate”.

While the regulator can always justify its current call as an insurance for the broader financial system, many in the market have argued that interest rates are set to peak near 4 per cent. In other words the market is indicating rates have less than 1 per cent extra to go from where they are today. However, the prudential regulator still insists that lenders work on the basis there is an extra 3 per cent still to go.

According to the Canstar group, APRA’s elevation of mortgage buffers to 3 per cent from the former 2.5 per cent in 2021 “means the average new homebuyer misses out on $21,000 in borrowing power”.

The problem for anyone exposed to residential property as either a potential owner-occupier or renter is where will new supply of housing stock come from? The reluctance of private investors to enter the residential market is matched by developers who are not building enough to match market demand.

The latest figures from global real estate group Jones Lang LaSalle show that residential developers have been abandoning or deferring plans over the last quarter, with the number of apartment projects approved across the market actually dropping in the three months to December.

No wonder the clearance rates for commercial property just are miles ahead of residential. Commercial property clearance rates are close to 100 per cent, residential clearance rates are struggling to get to 70 per cent.

More Coverage

Originally published as Super caps and mortgage buffers spell double trouble for property

Amid Super Retail ‘affair’, a CEO exerts his power uninterrupted

As workplace gossip swelled, an alleged affair with the CEO conferred power to his exec lover, court documents released this week claim, and fostered a fear of speaking up.

Farm sector CEO steps down after eight years

A well-known farm sector chief executive says he’s focusing on a “strong and good dismount” as he makes moves to step down from the job after eight years.