Australian shares deliver $560bn windfall, ASX 200 up 24pc for the year

The Australian sharemarket put in one of the biggest, broadest and most consistent financial year performances in a generation.

Business

Don't miss out on the headlines from Business. Followed categories will be added to My News.

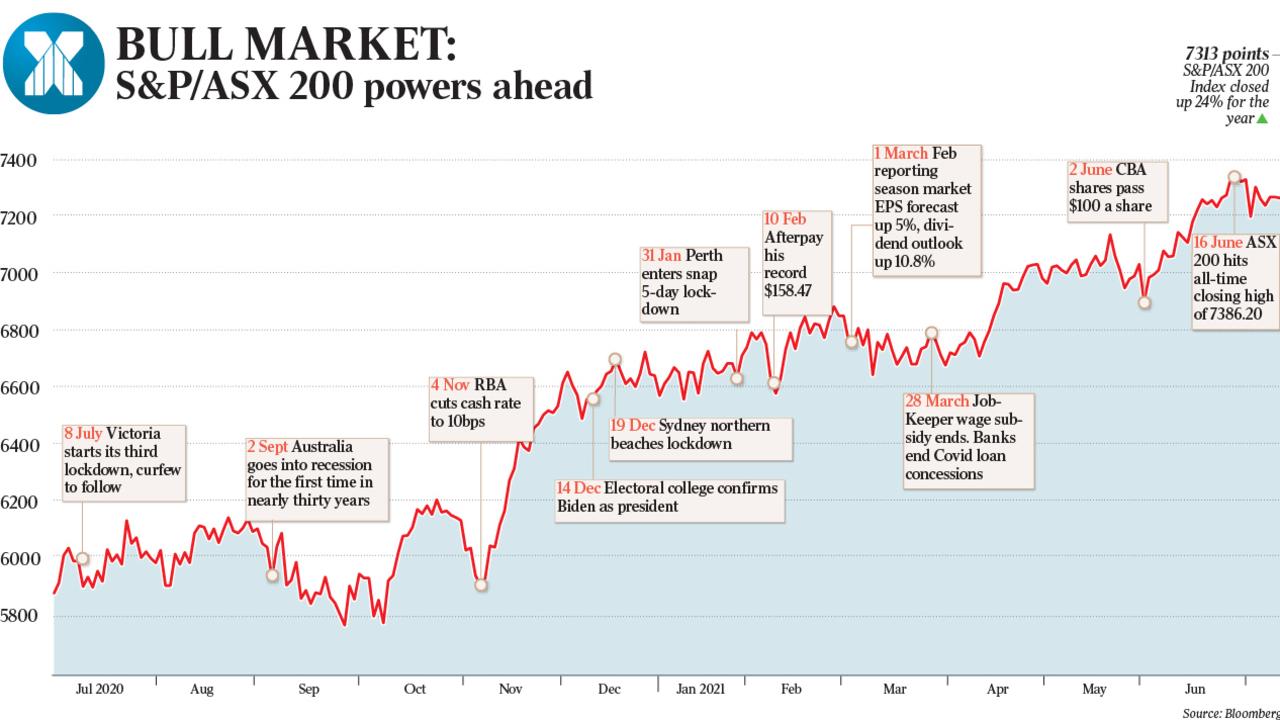

Australian shares roared to a 24 per cent surge over the past 12 months, delivering a $560bn windfall to investors, marking one of its biggest, broadest and most consistent financial year performances in a generation.

After diving 11.3 per cent in the 2020 financial year as the pandemic and lockdowns threatened economic growth and corporate profits, the local sharemarket built on its fastest-ever bull market, which began in March that year amid unprecedented monetary and fiscal policy stimulus.

The S&P/ASX 200 index’s jump in the 2021 financial year narrowly edged out a 23.7 per cent rise in the 2008 financial year to set its best financial year performance since the inception of the index used by financial professionals in 2000.

The broader All Ordinaries index rose 26.4 per cent, beating a 25.4 per cent lift before the global financial crisis. It was the best financial year gain for the All Ords since a 43 per cent rise in the 1987 financial year.

It was also the 10th-best rise in the All Ords since 1938.

And in a feat not seen before for the ASX 200, the benchmark rose in 11 out of the past 12 months.

“There have been just three times where we saw the ASX 200 up 10 of the past 12 months and looking back at those times it indicates the market ‘goes on with it’ – which is what I expect will happen with the ASX 200 over the balance of 2021,” said Bell Potters’ head of institutional sales and trading, Richard Coppleson.

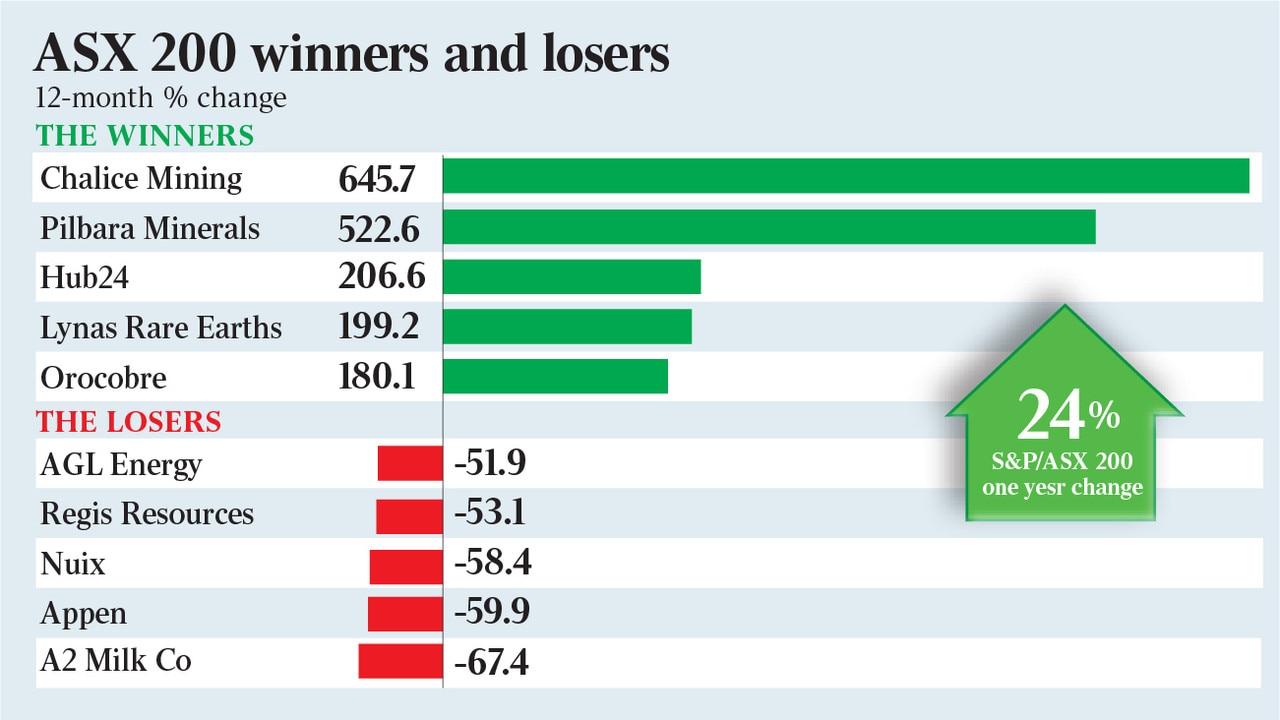

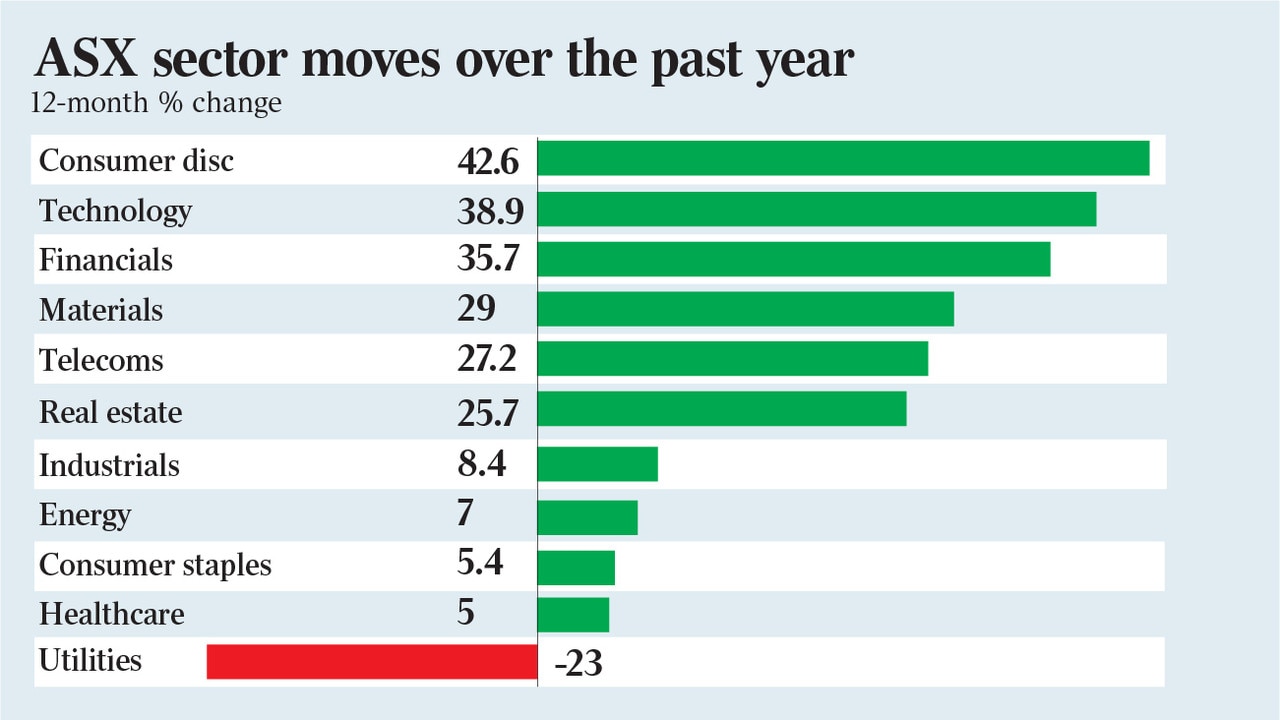

The rise was also remarkably broadbased with all sectors, bar utilities, finishing in the black.

The index also rose 2.1 per cent for the month of June despite the usual temptation for investors to lock in profits and book carry-forward losses on some of their worst stocks before the end of the financial year.

The June quarter rise of 7.7 per cent was the best since a 13.3 per cent rise in the December quarter.

Following its early 2020 fall from what was then a record high of 7197.2 points in February that year to an 8½-year low of 4402.5 points in March, the index surged as much as 68 per cent over the next 14 months, hitting a record high of 7406.2 points in May this year.

With vaccine breakthroughs occurring unexpectedly fast in the second half of 2020, the federal government unleashing a highly stimulatory budget on top of its massive JobKeeper wages subsidy that was extended until March, the Reserve Bank starting unconventional monetary policy – including yield-curve control and large-scale asset purchases – as well as near zero interest rates, and the US election outcome easing US political uncertainty and clearing the way for even greater US fiscal stimulus under President Joe Biden, the Australian market rode a wave of optimism globally.

Vastly better than expected corporate earnings in Australia for the second half of the 2020 calendar year and the first quarter of 2021 for the US then reinforced an accelerating recovery in cyclical sectors.

Surging commodity prices were another factor, with some analysts calling it the start of a new commodity “supercycle”.

Iron ore and copper hit record highs, coal prices surged even with China placing import bans on Australian coal and crude oil prices hit multi-year highs on a recovering demand outlook.

Banks took off as a booming local housing market lessened their bad debt provisions and asset sales paved the way for increased dividends and the restart of share buybacks in the months ahead.

All sectors except out-of-favour utilities rose, with the consumer discretionary, technology, materials, communications and real estate sectors outperforming the benchmark in the financial year.

The economic recovery that emerged in the second half of 2020 made for a tough year for the bond market, with Australia’s benchmark 10-year yield rising 66 basis points to 1.53 per cent.

The dollar rose from US69c to US75c, but retreated from a peak of US80.07c.

But while passive investors in the ASX 200 index would have made more than 28 per cent assuming dividends were reinvested, it was potentially challenging for active fund managers.

In the first half, the technology sector benefited from record-low interest rates, and stocks exposed to Covid-19 themes such as online shopping and working from home did well.

But the second half was dominated by financials, consumer discretionary and communications, while technology lost ground, although it bounced sharply in the final two months.

A marked divergence between the performance of “growth” and “cyclical” sectors during the financial year potentially made it difficult for active fund managers to outperform in both halves.

Hyperion Australian Growth, for example, returned 33.38 per cent net of fees for the 12 months to May 31, exceeding its benchmark by 4.67 per cent. But it underperformed its benchmark by 8.63 per cent in the final six months of that period. However, the fund will have benefited from a 27.4 per cent rise in the share price of its biggest shareholding – Afterpay – in the past month.

Hyperion Asset Management chief investment officer Mark Arnold says the high economic growth levels that have driven big gains in cyclical stocks this year are likely to be “temporary”.

“We think economic growth will normalise and return to a pretty difficult environment if you look out 12 months, and that’s a very good environment for our style of investing,” he said.

“So growth right now is abundant but in the medium term it will be scarce.”

His “top-down” view is that commodity prices are “artificially high” due to the effects of fiscal stimulus, economic reopening and supply chain disruption.

Some commodities are likely to fall “pretty dramatically” as demand shifts to services.

“As the global economy normalises and a lot of the government transfer payments drop out, that will reduce demand growth so we see downside risks for some of the cyclical areas of the market,” he said.

“We think the concentration of ‘old world’ businesses in the Australian sharemarket that are likely to be disrupted is not a good basis for the overall market going up.”

“We think you have to be selectively buying the businesses that are disrupting the rest and avoid those lower-quality businesses that are reliant on economic growth and are likely to be disrupted.”

“If you buy an index fund, you’re buying a whole lot of problems over the next few years as the economy slows and tech disruption really takes hold.”

Similarly, T. Rowe Price Australian equities head Randal Jenneke said strong economic growth this year was “already priced into Australian share prices”.

He noted that as a market heavily skewed towards value sectors, Australia underperformed global markets in 2020, but the vaccine rollout and policy stimulus underpinned “global reflation” in 2021, favouring Australia’s “high beta” to resources and the global business cycle.

But his view is that growth and inflation may peak in 2021.

“Our Australian equity portfolios are positioning for the return to favour of quality growth in 2022,” Mr Jenneke said.

“For 2022, our expectation is that local and global growth will likely begin to fade as fiscal stimulus begins to unwind, after being heavily front-loaded into the first half of this year.

“As a result, consensus earnings growth estimates will likely be trimmed and earnings momentum may turn negative. Under this scenario, value is unlikely to continue to outperform growth.

“We expect the value rotation trade to first fade and later reverse.”

Unlike some market strategists, Mr Jenneke sees limited scope for interest rates to move much higher given the historically high post-Covid levels of domestic household debt.

“In our view, it is not too soon to think of taking profit on some of the value positions that have done well, and to begin positioning Australian equity portfolios for the return to favour of quality growth in 2022,” he said.

“We note that stimulus as measured by the fiscal impulse is much less in 2021 than it was in 2020. In 2022 it is set to turn negative – the ‘fiscal cliff’ effect – subtracting from GDP growth in that year.”

“Under these conditions – a return to slower growth and sustained low interest rates – we believe growth stocks should return to favour.”

Originally published as Australian shares deliver $560bn windfall, ASX 200 up 24pc for the year

Environmental threat to 2030 energy goal: Acciona

Acciona has flicked the switch on the biggest wind farm in the southern hemisphere, but warns environmental rules remain the major obstacle for more renewables.

Big changes on the way for chastened ANZ

ANZ chief Shayne Elliott has vowed to make a significant number of changes to his bank’s policies and practices before the year’s end.

Why Regal’s Phil King is taking on the widowmaker trade

Is the hedge fund boss being brave or foolhardy by going where many have gone before and fortunes have been lost.

Prospero clients to get their cash back

Clients of shuttered foreign exchange trader Prospero Markets, whose managers were involved in a huge money laundering sting last year, look likely to get their money back.

Alliance bucks trend with record year and ‘better to come’

Just like Rex, Alliance Aviation saw the opportunity to expand its fleet during the Covid pandemic but while one airline failed spectacularly, the other soared to new heights.

Proxy firm charts Perpetual ‘risks’

Influential proxy group Ownership Matters says shareholders reject Perpetual’s remuneration report.