Is it time to reconsider investing in China?

Renewed interest in China is prompting a rethink by investors, but can your portfolio take the risk?

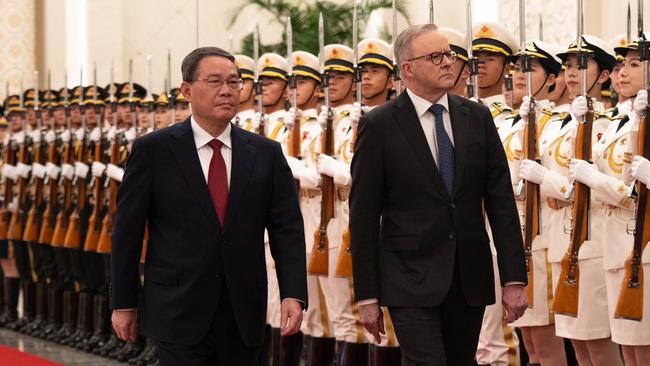

Prime Minister Anthony Albanese’s visit to China this week marks a new phase in diplomatic relations between the two nations.

It has also prompted renewed optimism among local investors, but is this new interest misplaced?

For active investors and self-managed super fund (SMSF) trustees who use a financial adviser for investment advice, a prudent approach may be best here.

The world’s most populist country after India and second biggest economy after the US, it has long been the engine room of global growth since paramount leader Deng Xiaoping seized power in the late 1970s and began to dismantle the “bamboo curtain” with a series of bold economic reforms.

His portentous 1980 speech where he outlined the “great tasks” facing China set the tone – and economic direction. In its wake, the economy grew exponentially. It’s estimated in the following decades 800 million people were lifted out of poverty.

Private enterprise flourished, with entrepreneurs happy to live by one of Deng’s more famous dicta, “to get rich is glorious”. In large part, China’s reforms were welcomed by the West – after all, as Australia can attest, the economic benefits were enormous.

But today, the optimistic assumption that China would integrate smoothly into the world economy is in tatters.

Under Xi Jinping, whose control over the communist party and state is absolute, China has embraced an aggressive foreign policy that directly challenges the US, and many of its Asian neighbours.

Just as significantly, its economy is spluttering – at best. A strong start to 2023 in the wake of China lifting Covid-19 restrictions has ground to a halt.

Exports are falling. Consumption, production and investment have slowed.

Researchers at investment houses Nomura, Morgan Stanley and Barclays have all trimmed their forecasts while unemployment has edged up, especially among the youth, although by how much is not known. China has stopped publishing the data. And the renminbi is trading at historic lows against the US dollar.

A recent RBA report highlighted the vulnerabilities in China‘s financial system due to the “sharp deterioration” in its property sector that accounts for about 30 per cent of GDP. With major property developers on the brink of collapse, there is ongoing speculation that their downfall could have a contagion effect across the economy.

Yet amid this gloom and doom, there are still analysts and fund managers seeing green shoots. Interestingly, the bellwether China Shanghai Composite Stock Market Index has changed little over the past year, up nearly 2 per cent, although the direction has been mostly south since May.

Investors and advisers continuing to see the China glass as half full aren’t necessarily wrong. Coherent arguments can be made for looking past Chana’s economic woes and the geopolitical threat it potentially poses to see a compelling long-term investment story.

Wenchang Ma, the Hong Kong-based portfolio manager at the $US158bn active global asset manager Ninety One, told a recent JANA conference that investors need to stop seeing China through a Western prism that ignores the systematic differences, and appreciate that growth is moving away from property to more sustainable economic drivers that will result in slower but long-term quality growth.

She cites factors such as a rising middle class driving consumption growth, the concerted push to achieve technology self-sufficiency, transition to renewable energy, state-owned enterprise reform and continuing integration with the global economy.

Her list does not stop there. R&D spending in catching up with developed countries, while on the international patent front, China’s applications make it the global leader. Ma is not alone. The global asset manager Foord, which has funds under management of $US6.3bn, is a strong advocate of the China story.

Portfolio manager Jing Cong Xue argues China is playing the long game of economic reform and resisting the impulse the pump prime the economy.

Although he concedes a rapidly worsening economy could weaken Beijing’s resolve, signs suggest they are prepared to accept short-term pain to tackle inefficiencies in the economy. For long-term investors, he argues this is exactly what they should want to see, a China taking some economic pain to allow new economic sectors such as renewable energy, EVs, e-commerce, gaming, online travel agencies and cloud computing to emerge.

A China that adopts this economic path and avoids loose monetary policy, property, and state-driven investment could then take the leap from a mid-level economy to a modern, productive economy. But what happens if these fund managers are wrong?

What if there is no respite from China’s well-documented economic woes of the past two years? The consequences for Australia’s economy, particularly the materials and financial sectors – about 50 per cent of our economy – are dire.

In addition, investors would seek a haven in the US dollar, further weakening the Australian dollar.

Can your portfolio withstand a plummeting Chinese economy?

The short answer is probably no, with many investors highly leveraged to real estate, materials, financials, and the Australian dollar.

So stress testing your portfolio across all market conditions is crucial, including understanding and analysing regional exposure – especially to China.

Jamie Nemstas is principal at Wattle Partners

Add your comment to this story

Buffett’s bank exit signals trouble for Australian investors

Top investors are selling, convinced record share prices for stocks including CBA are not justified by underlying profits.

Four small caps tipped to rally

Ophir Asset Management’s Aussie small cap fund returned 39 per cent last financial year. Here’s where they’re investing this year.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout