Mortgage-backed securities defy homes slump

A housing market slump and emerging pockets of borrower stress have not deterred lenders from the securitisation market.

A housing market slump and emerging pockets of borrower stress this year have not deterred banks and other lenders from the securitisation market or their plans for future activity.

That is the main finding of The 2019 Australian Securitisation Issuer Reportthat conducted two stages of research across 55 issuers of the securities.

The report is being jointly released by Perpetual and The Australian Securitisation Forum (ASF), which counts the big four banks, AMP and Credit Union Australia among its members.

Securitisation is an important funding source for banks and other lenders as they can package mortgages and other loans and sell them in tranches as tradeable debt securities.

The report found that despite a marked slowdown in housing credit growth, 46 per cent of respondents said they would be likely to increase their securitisation issuance in the next two years, while 49 per cent said it would roughly stay the same.

“The market is very stable and resilient,” Perpetual Corporate Trust group executive Richard McCarthy said.

“The housing market is a concern obviously, but there is a view from the market that we are getting close to the bottom.”

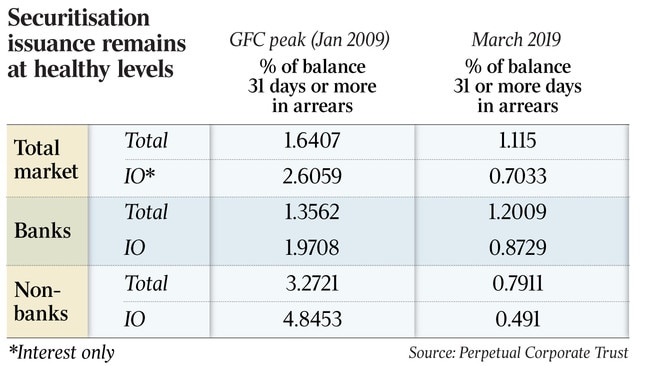

Mr McCarthy said the data for securitised prime home loans was “performing well” and arrears levels across mortgages and interest-only home loans remained at low levels.

He pointed out that lenders outside the banks were seeing a better arrears experience.

“The non-banks are outperforming the banks. There has been a significant improvement in the non-bank sector,” Mr McCarthy said.

Perpetual’s data shows non-banks have about 0.8 per cent of home loans in arrears, by 30 days to more than 90 days, compared to 1.2 per cent for the banks.

On Monday, Commonwealth Bank’s March quarter update reignited debate over asset quality when it reported a $100 million rise in impaired home loans, as broader troubled and impaired loans climbed over the three months to the end of March.

Locally, securitisation deals froze during the fallout from the global financial crisis with many issuers fleeing the market for several years. The Australian market is dominated by issuance of residential mortgage-backed securities, or RMBS.

Industry data shows that while 2017 was a post-GFC high for RMBS transactions at more than $35 billion, that dropped to about $26bn last year. Already this year RMBS deals have been launched by ME Bank, Firstmac, Pepper Group and La Trobe Financial.

Mr McCarthy said the securitisation industry was working to broaden its investor base globally and had made huge strides in Asia.

New asset classes and a spate of new digital banks and fintech lenders would also help the local market, he added.

The report highlighted that the main challenges for issuers were the macroeconomic and housing outlook, the lack of a secondary market and the impact of regulatory changes on securitisation markets.

ASF chief Chris Dalton is confident the federal government’s $2bn securitisation fund will be a positive for the industry and also “play a role” in growing sources of funding for the small business sector. He also sees innovation playing a part in the industry over the next three to four years.

The report found that almost two-thirds of respondents neither agreed nor disagreed that the Hayne royal commission would lead to positive outcomes for securitisation.

Still on regulation, Australian companies looking to Europe are being mindful of new regulations.

Last year new rules were introduced, which apply to issuance completed after January 1, 2019, aimed at creating simple, transparent and standardised (STS) securitisations.

The rules aim to re-establish a “safe securitisation” market in Europe following the GFC.

No surrender: Wilson-Bolton war in its final stages

The long-running conflict between Geoff Wilson and Nick Bolton must be amongst the most expensive and all-consuming in Australian financial services in recent decades.

Keep up: How CEOs are navigating the Trump frenzy

Some of Donald Trump’s biggest calls are sending financial as well as strategic shockwaves through business. And they’re all unfolding in real time.