China ‘stabilising’ after a year of reforms

The head of China global markets at UBS, Thomas Fang, tells why he is cautiously optimistic about the outlook for China’s economy and markets in 2022.

Thomas Fang is cautiously optimistic about the outlook for China’s economy and markets in 2022.

Regulatory change is now somewhat expected and a lower growth rate will be partly a result of efforts to deleverage and reorientate the economy to lessen systemic risk and meet its goals.

Still, it was challenging for investors to understand and accept the regulatory changes behind last year’s underperformance of sharemarkets in Hong Kong and the mainland.

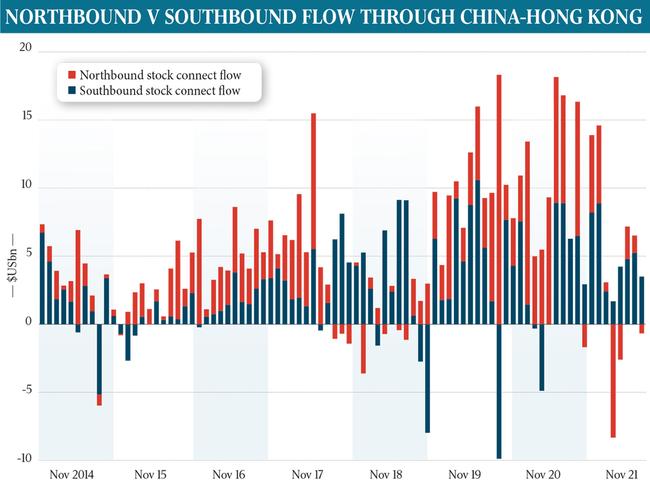

While the MSCI World Index of developed markets rose a massive 20 per cent last year, China’s Shanghai Composite rose just 4.8 per cent and the Hang Seng Index dived 14 per cent as Hong-Kong listed shares of mainland and US-listed companies were pummelled.

“I think there’s some comfort in terms of the risk premiums priced in,” said Mr Fang, who is the head of China global markets at UBS.

Indeed there have been changes to China’s regulations in the past year or so, starting with its financial sector in late 2020, and followed by others such as property, gaming, tutoring and so on. They covered issues including antitrust, data security, carbon neutrality and common prosperity.

“Our clients and regulators have focused on the response from international investors and overall there’s a general sense of stabilising on the regulatory front,” Mr Fang said.

“The direction of policy in regard to those four subjects will continue, but the pace of change will probably be more understandable or expected by the international investment communities.”

He feels regulators understand the need to “provide transparency and give international investors a little bit more lead time, so that they understand the rationale and the pace of those regulations”.

Quarantining in China last month before visiting clients, colleagues and regulators ahead of the UBS Greater China conference, which will be held entirely virtually this month for the first time, Mr Fang didn’t rule out changes which “certain investors take as a surprise, because the direction of those regulations – whether antitrust, common prosperity and so on – that’s here to stay.”

In August, China released a five-year plan calling for greater regulation of its economy.

Chinese authorities will work to make new rules on national security, technology and monopolies, while strengthening enforcement in food and drugs, big data and artificial intelligence, according to a joint document from the State Council and the Chinese Communist Party’s Central Committee.

As for when the next round of regulatory changes might occur, Mr Fang is focusing on the National People’s Conference and the Chinese People’s Political Consultative Conference in March.

But trimming the nation’s growth rate may be the price it pays for lessening systemic risk.

After a deceleration in China’s economy following a very strong first quarter, the consensus sees 8 per cent annual GDP growth for 2021 and close to 5 per cent in 2022 amid uncertainty around China’s property sector and segments of consumption. Base comparisons will be challenging and as the global economy reopens, demand may shift more from goods to services, according to Mr Fang.

“So overall China is really slowing down after a period of “first in, first out” regarding the Covid-19 pandemic, and the focus is on the extent to which policy makers can be accommodating,” he said.

In that way, a slightly scary period for markets in 2021 could yield a more sustainable outlook.

“Overall the regulatory dynamic will continue with some of the new directions,” he said.

“It is relatively well priced in terms of risk premiums, but we need to focus on the next round of actions.”

To be sure, there remains a lot of uncertainty about the outlook for China’s property sector after the near collapse of what was once China’s biggest property developer, China Evergrande.

That’s notwithstanding the fact that China’s real estate sector is relatively fragmented and has not seen the collateralisation of housing debt seen in the US in the lead-up to the subprime loan crisis.

“I don’t see China’s property sector as a systematic risk at this point,” Mr Fang said.

But he argued that the high-financing cost models of the primarily privately owned property companies – their old business models – will no longer be sustainable. “I think from the top, Chinese leaders are of the view that this should not be a sector that continues to be the key driver of economic growth, and we should not have too much speculation.

“What it will probably lead to is more state-owned property companies with lower leverage, lower financing cost and in many ways, lower profitability.

“The good part is, the overall demand for property in China, especially in the top-tier cities, continues to be healthy, whereas in some of the US subprime issues, other than regulation and de-leveraging, it is really the demand side having that issue of weakness.

“In Shenzhen, my team members, working for a global institution like UBS, need to pay a 70 per cent down-payment to get their new property when they have their second child,” Mr Fang said.

“So there’s strong demand and also not that much leverage and overall I think that going forward there will be limited room for highly leveraged property companies.”

Mr Fang does not see much risk of Chinese policymakers’ incremental stimulus causing inflation to take off.

“China set a relatively low target of ‘above 6 per cent’ GDP at the start of the year. After a few quarters, the target will easily be reached, so there are not that many accommodating policies,” he noted.

“As a country, China actually deleveraged about 8 percentage points while the rest of the world was stimulating during the pandemic.

“So far it seems as though inflation in China is manageable and well under control. So we are expecting both monetary and fiscal policy to be more accommodating.”

With a relatively strong US dollar, exporting strength and relatively tighter monetary policy this year, the yuan has appreciated further, so China’s inflation has naturally been under control.

“So our view is the overall economy will probably hit the bottom in terms of GDP in the first quarter of 2022 and we expect it to pick up from the second quarter onwards on the back of more accommodating fiscal and monetary policies,” he said.

“Also the overall zero-tolerance Covid policy before the Winter Olympics, cold weather and the March key events for the government in Beijing will be behind us.

“China may be a little more open from a Covid perspective after this time.”

It’s his second year of quarantining in China before his annual trip, and Mr Fang said the three-week quarantine requirements this time had been much stricter than last year.

“You can see how the influence of the zero-tolerance policy has been definitely weighing on China’s growth from the tourist sector and obviously hotels and airlines as well as the general consumption,” he said.

“Along with the push for carbon neutrality goals, property slowdown and seasonal pressure on air quality in northern China, the zero-tolerance policy has been a drag on the economy in late 2021.

As for the new drivers of China’s growth that are likely to emerge, the major contributor that needs to keep growing is clearly the consumer sector.

“In many ways, some of the measures like ‘common prosperity’ are trying to address that, so that you have that growth of the middle-income class in general,” he said. China’s annual income per capital is only about $US9000 versus about $US66,000 in the West.

Mr Fang sees scope for more growth from hi-tech industries.

He also feels China is well placed to develop the necessary infrastructure and economic ecosystems.

More Coverage

Add your comment to this story

IDA ‘to fast track $50bn investment’

The new Investment Delivery Authority will accelerate approvals for projects valued at more than $1bn, including advanced technologies and energy.

‘Boring’ budget to lay foundations for repair

Don’t expect many sweeteners in the Crisafulli government’s first budget on Tuesday, with LNP Treasurer David Janetzki planning to unveil the foundations for debt repair.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout