Virgin Australia is expected to update the market on Wednesday surrounding its current state of affairs as its debt investors, who have watched the $100 they paid for their bonds slide to $62, remain on tenterhooks.

The carrier is under the spotlight as the aviation industry remains in turmoil due to the coronavirus and the extent of the damage depends how long the health crisis continues.

Virgin Australia is buckling under adjusted net debt of $5bn when its market value is only $675m and it posted an $88.6m half-year loss. Its bonds slid to $62 on Tuesday morning before rebounding to $72 later in the day, only months after investors took up the offer.

Trading is slim in the Virgin bonds, which are listed here in Australia, with only 16,631 traded by Tuesday morning.

Yet some believe a bailout of the carrier by shareholders such as Singapore Airlines would occur before it would be allowed to collapse. Singapore Airlines has been tipped before to be keen to secure a stronger grip on Virgin Australia, and the situation could even be used as an opportunity to take more market share away from Qantas.

Investment bank UBS assisted Virgin Australia last year on its bond raising, which secured $325m to help pay for its $700m acquisition of the remaining 35 per cent stake in the Velocity frequent-flyer program that it did not own.

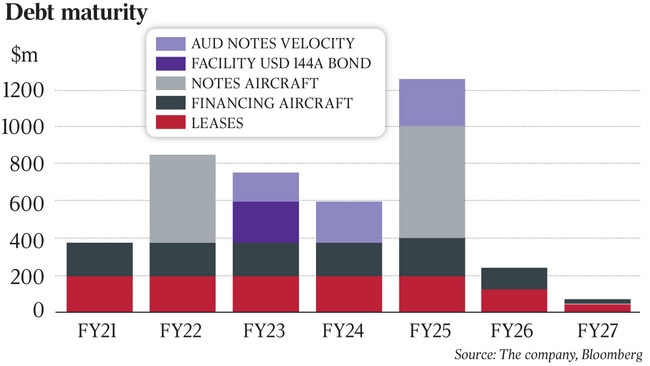

The challenge for Virgin remains the fixed costs it has for operational leases and asset finance on its aircraft, although some take comfort from its $900m deposit that it has at hand and that the lower oil price will mean falling fuel costs.

The payments for the leases need to be made even though international air travel is plummeting due to efforts to contain the spread of the coronavirus.

Meanwhile, on Tuesday, sources said the primary bond market was mostly closed, with spreads on oil-related stocks, such as Santos, blowing out.

The latest episode of panic selling following the oil price collapse and coronavirus fears is also likely to put the brakes on Emeco’s attempts to tap the Australian bond market. Emeco had been working with UBS here in Australia to secure up to about $350m through its retail broker network, as revealed by DataRoom. Documents obtained by the column revealed that retail investors were offered the opportunity to invest in Emeco bonds with a 6.5-7 per cent yield.

Another company that could suffer sharply from the turmoil is Speedcast, which has contracts with cruise ships and is already in distress, while junior miners and retailers could end up with a funding shortfall if the US debt markets shut, while travel groups are likely to be hard hit.

But sources in the market say large-scale redemptions are not yet occurring in the US debt market.

Add your comment to this story

Bain Capital zeroes in on Healthscope’s debt pile

Bain Capital has been sharpening its recapitalisation focus on Healthscope in recent weeks, according to sources.

Asian suitors fall by the wayside in $2bn goldmine auction

Indonesian suitors which had been closing in on the Ravenswood goldmine in Queensland are believed to have staged a retreat.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout