AMP reaps $100m in zombie super account fees

Scandal-plagued AMP is reaping more than $100m in fees every year from 1.1 million zombie superannuation accounts.

Scandal-plagued wealth company AMP is reaping more than $100 million in fees every year from 1.1 million zombie superannuation accounts, as part of a broader $2.6 billion nest-egg gouge.

With Labor stalling government moves to return more than $6.6bn in savings to Australians, The Australian can reveal that major funds in the $2.7 trillion superannuation sector are holding on to high rates of lost and forgotten member accounts that are vulnerable to having their balances eroded by excessive fees.

The Morrison government will use this month’s parliamentary sitting weeks to try to ram through legislation that was announced in last year’s federal budget that would hand the Australian Taxation Office the power to claw back inactive accounts with less than $6000 and return savings to super customers.

The Protecting Your Super package has been thwarted amid intense lobbying by super funds for amendments.

Labor — under pressure from union and employer-backed industry super funds — has requested a series of amendments to the legislation, amid concerns workers in high-risk industries may be left uninsured.

The Productivity Commission estimates a third of all super accounts are unintended multiple accounts — a product of workers opting for an employer’s default super manager through the enterprise bargaining system when they sign up to a new job.

These multiple accounts are often unwanted and unneeded, but they come at a cost of $2.6bn a year in fees.

Of the 25 million accounts in the system, 7.8 million are inactive accounts.

Josh Frydenberg said if Labor was serious about improving retirement savings, it would “stop prioritising their vested interest and instead support these measures”. He said the Productivity Commission had described them as “must-have” reforms. “The Labor Party need to explain why they are opposed to changes that would see, on average, an additional $2000 in the superannuation accounts of Australian members in the first year of the policy,” the Treasurer said.

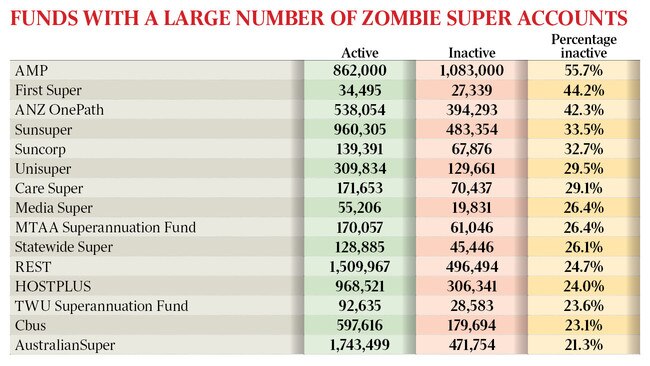

Of the nearly two million customer accounts managed by wealth giant AMP, 56 per cent are considered inactive by the Australian Prudential Regulation Authority, meaning they have not received any contributions in at least two years.

Because the fund charges an annual membership fee of $91, along with percentage-based fees on the amount of savings in the accounts, AMP is generating at least $100m in revenue from idle accounts each year.

An AMP spokesman said it supported legislative efforts to reduce inactive accounts, but it was not possible to draw accurate comparisons from the APRA data. AMP said many inactive accounts received a “capital guarantee” and it was “often in members’ best interests to maintain these accounts, given the future benefit they will provide”.

Union and employer-backed industry fund First Super, which The Australian revealed this week was under pressure to merge with a larger fund and did not sign up to an industry-wide code of practice to limit insurance fees, has 44 per cent of its 60,000-strong membership in inactive accounts.

Each First Super member is charged a flat $78 fee and a series of asset-based charges.

First Super did not respond to requests for comment.

The government has refrained from putting the legislation to a vote in the Senate as it could not secure support for the package without several amendments demanded by the opposition.

Labor and industry funds are concerned the government would benefit from the proposed laws by accounting for the claimed assets in the budget bottom line.

The ALP wants the ATO to consolidate an account within 28 days and remove the requirement that ATO-held accounts be larger than $6000 before they are reunited with their member. Its financial services spokesman, Clare O’Neil, said: “While we support the objective of the bill to protect members’ superannuation savings from erosion by fees and charges, there are significant gaps in the government proposal.”

Many smaller funds also rely on inactive accounts to subsidise their active members, whose fees would have to rise if they lost the zombie accounts. If the ATO claimed the accounts, it could threaten the business model of several funds.

In order to stop workers being defaulted into multiple accounts, the Productivity Commission has proposed unshackling the super system from the industrial relations model. This would allowing workers to choose from a list of the 10 best funds in Australia into which they could then only be defaulted once. Members would be free to change fund in the future.

Vicki Doyle, chief executive of REST Super, where a quarter of the fund’s two million members are inactive, said the government’s definition of inactive — 13 continuous months without a super contribution — did not reflect maternity leave or casual work patterns. “While we support initiatives that reduce the erosion of members’ retirement savings, we believe the proposal to transfer inactive accounts to the ATO will be detrimental to REST members and many other working Australians,” she said.

MTAA, where 26 per cent of members are inactive, said: “While MTAA Super supports efforts to address this issue, we don’t believe the ATO is the best mechanism to achieve this.”

AustralianSuper, which has 21 per cent of its 2.2 million members in inactive accounts, this week changed its fee structure to ensure there was no cross-subsidisation of members in preparation for the legislation, which will also apply a 3 per cent fee cap on small accounts.

“AustralianSuper supports returning low and inactive accounts to the ATO and that they are then reunited with the main fund account as soon as possible to ensure that members don’t miss out on the benefits of compounding interest,” said AustralianSuper executive Paul Schroder.

Mr Schroder said the fund had consistently advocated this to government and other funds.

ANZ, which has 42 per cent of its OnePath members inactive, told the Productivity Commission it supported a situation where members would only have one superannuation account.

Statewide Super chief executive Richard Nunn, whose fund has 26 per cent of its accounts held by inactive members, said the company had a stricter definition of inactive than the one employed by APRA and has been proactively consolidating accounts. “We support the transfer of inactive members to the ATO, when we have exhausted all efforts to contact them. The ATO are in the best position to reunite lost members with their super,” Mr Nunn said.

A spokeswoman for SunSuper, where 34 per cent of members are inactive, said the fund was “broadly in favour” of the proposals around account consolidation. “However, we would like to see some more details about the reforms including the mechanism for consolidation, as well as the timeliness of funds being returned to members’ accounts.”

A third of SunSuper’s inactive accounts have a zero balance. “Twenty per cent of Sunsuper’s member base is a contingent workforce where many members tend to change funds when they change jobs. That is why we support the Productivity Commission’s recommendation that a consumer’s first default should be their last default. For this to work in consumers’ best interests, the current rules for allocating default accounts must be changed to protect individuals from poor products and to ensure system competitiveness, efficiency and fairness,” SunSuper said.

Cbus chief executive David Atkin said the fund supports “sensible and workable” attempts to reduce multiple accounts.

“While the current legislation could do more to improve retirement outcomes, we don’t object to the consolidation measures passing,” Mr Atkin said.

UniSuper brand manager Melissa Ladner said the fund supported measures which lead to account consolidation “when it’s of benefit to our members, perhaps through avoiding duplication of account fees or where inactive accounts provide insurance cover the member doesn’t need”.

More Coverage

Add your comment to this story

ASIC to pursue fiscal rogues

ASIC has vowed to test the law to its fullest in tackling financial crime and deterring future misconduct within the fiscal sector.

Bligh urges legal action to build trust

ABA chief Anna Bligh is urging the next government to introduce an industry reform bill within 100 days.

To join the conversation, please log in. Don't have an account? Register

Join the conversation, you are commenting as Logout