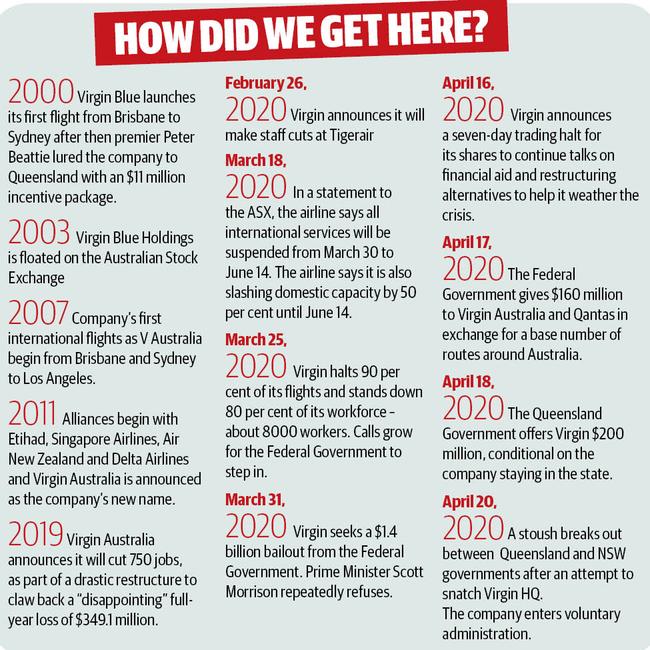

Virgin Australia goes into voluntary administration

Embattled carrier Virgin Australia has collapsed under a $5 billion debt pile and coronavirus travel restrictions after frantic negotiations failed to secure an 11th-hour buyout.

QLD News

Don't miss out on the headlines from QLD News. Followed categories will be added to My News.

VIRGIN Australia collapsed last night under a $5 billion debt pile and coronavirus travel restrictions after frantic negotiations failed to secure an 11th hour buyout.

Sources confirmed that the company had been placed in voluntary administration and appointed Deloitte to try to save Australia’s second-largest airline.

Terry McCrann: Virgin is dead no matter how much money you throw at it

Regional, tourism bosses alarmed by Virgin collapse

Coronavirus Qld: Virgin Australia boss comfortable with airline’s position

Virgin was expected to announce the move this morning after the stock market opened. But the announcement, set to rock Australia’s tourism industry, could pave the way for the Federal Government to inject funds into the troubled carrier if it is completely overhauled and equity value is wiped completely.

The company was put in a trading halt last Tuesday before moving into a voluntary suspension two days later.

It was unclear what the move would mean for the company’s 10,000 employees, creditors, frequent flyers and customers holding tickets.

Virgin Australian did not respond to requests for comment last night.

Deloitte administrators Vaughan Strawberry, John Greig and Richard Hughes will keep the airline flying and seek a path to viability after shedding debt and finding new owners.

It follows a series of crisis talks on a day that started with a glimmer of hope as Queensland and NSW looked set to enter a bidding war to secure the company’s headquarters and 5000 employees currently based at Bowen Hills.

Virgin had been seeking a $1.4 billion bailout from the Federal Government, with chief executive Paul Scurrah warning of “catastrophic” outcomes if the airline failed.

But the Government, which has committed almost $1.3 billion to the aviation industry during the coronavirus pandemic, refused to give Virgin a blank cheque from taxpayers.

It had also grown frustrated with what it believed were the company’s strong-arm tactics and bluffing, but up until yesterday morning remained confident a “market solution” would emerge.

Virgin had been reduced to flying just one daily return flight between Sydney and Melbourne during the coronavirus crisis.

But last week that increased to 64 weekly return services under a $165 million Federal Government package to keep key domestic routes, including to regional Queensland, operating.

The Queensland Government had launched a last-ditch attempt to save the airline, offering a $200 million rescue package.

Queensland Industry Minister Cameron Dick also opened the door yesterday to increasing that to stave off a push from NSW to relocate Virgin to the new Western Sydney Airport.

“We will stop at nothing to ensure the headquarters of Virgin remains in Queensland,” he said.

The Queensland Government declined to comment last night.

The Virgin board was believed to have held a crisis meeting yesterday after negotiations with the states failed to offer a solution.

Melbourne-based private equity firm BGH Capital is emerging as a strong contender to take over Virgin.

BGH declined to comment last night.

It is thought the firm is one of several interested in the airline, which analysts believe can be run profitably if it can jettison the more than $5 billion of debt it is servicing.

Virgin’s founder Sir Richard Branson sent an open letter to 70,000 staff globally saying he was “working day and night” to save his businesses but his airlines would need financial help as Virgin was in a “fight to survive”..

Originally published as Virgin Australia goes into voluntary administration

I used to sleep in a stable, now I’m a millionaire property tycoon

He grew up so poor he was once gifted nothing but a can of condensed milk for Christmas, but through 12-hour days, seven days a week Phil Murphy toiled away. WELCOME TO HIGH STEAKS

Elite Brisbane school’s shock swim club call amid coach’s legal stoush

The prestigious swim club of an elite school has been sensationally axed, just months after its sacked head coach took legal action.