Regional housing market remains red hot, with prices more than doubling capital city gains

Fierce demand for housing in the regions continues unabated, with prices in one highly popular ‘lifestyle’ market streaking ahead.

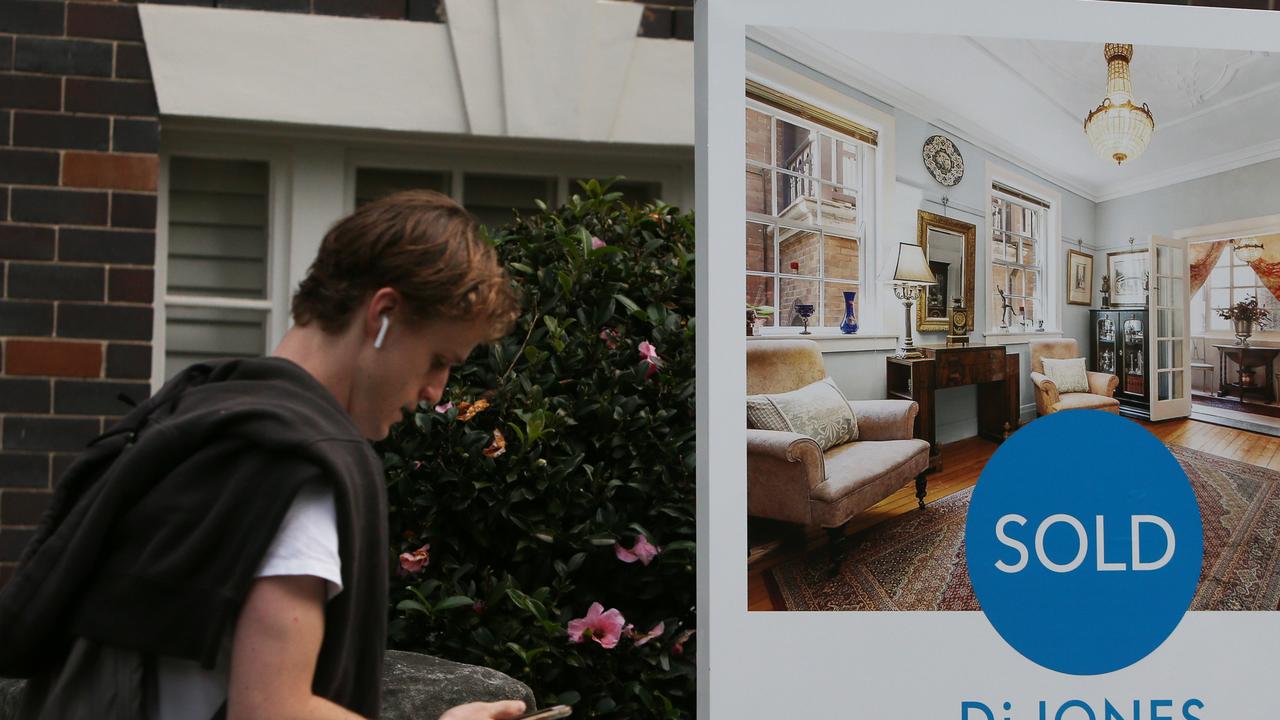

Australia’s regional housing market has far outpaced price growth across capital cities in the past 12 months, with values more than doubling.

CoreLogic quarterly data on country areas released on Tuesday shows residential property prices jumped 13 per cent compared with a 6.4 per cent gain in capital cities.

The group analysed the 25 biggest non-capital city markets and gave Richmond-Tweed in NSW the top gong for gains across both houses and units, with 21.9 per cent and 15.5 per cent annual growth respectively.

The worst performer across both markets was Bunbury in Western Australia, where house prices rose just 3 per cent, while unit values declined 4.4 per cent over the year.

The South West region town, however, had the highest change in sales volumes, up a whopping 51.4 per cent.

CoreLogic research director Tim Lawless said the strong demand for regional property through the COVID-19 era could partly be explained by the popularity of remote and flexible working arrangements and also the heightened desire for lifestyle-oriented dwellings and holiday homes.

“No doubt the more affordable housing options across many of Australia’s regional markets is another incentive; in April there was a $247,400 difference between the median value of capital city dwellings and regional dwellings,” Mr Lawless said.

On the lifestyle trend, he said it was no surprise to see the Richmond-Tweed area topping the list for capital gains given the region included high-profile beachside destinations such as Byron Bay, Suffolk Park and Lennox Heads as well as popular hinterland villages such as Bangalow.

“The median house value across the Byron council area is now $1.4m, which is higher than Greater Sydney’s median of $1.147 million,” Mr Lawless noted.

He said the outlook for regional housing markets was buoyant amid ongoing higher than average levels of demand, especially markets close enough to capital cities to provide a commuting option and those popular with “sea and tree changers”.

While surging property values were good news for homeowners, affordability was being stretched for those who don’t own a roof over their head, Mr Lawless also noted.

“Long-time locals whose incomes are unlikely to be rising at anywhere near the pace of house price appreciation may be forced to seek out housing options further afield,” he said.

The Reserve Bank is keeping a keen eye on the housing market and lending standards, with governor Philip Lowe saying in March he would be worried if Australians started “borrowing ridiculous amounts of money” in a speculative way.

That concern appears to be well founded, with recent data showing investors are returning to the market after sitting on the sidelines last year and a decrepit, one-bedroom house in Sydney selling for an "absurd" $1.62m on Saturday.

The federal government’s proposal to repeal safe lending laws, which came before the Senate last week, is being staunchly opposed by consumer groups, who worry it could push home ownership out of reach for many more Australians.

Heartbreaking personal stories are flowing from the rental market, where the end of the COVID-19 moratorium on evictions and rent increases prompted landlords to sell their properties to cash in on sky-high prices.

Many tenants turfed out or slugged with jacked-up rents have been forced to couch surf or take other desperate measures.

“We’re getting thousands of calls a month with people absolutely desperate to find a home,” Tony Pietropiccolo, chief executive of West Australian social services provider Centrecare, recently said.

“We cannot keep up.”

How Aus suburb is reaping Block’s rewards

This Aussie town is benefiting from The Block, with the reno series injecting almost $8 million into the area.

$114m land deal to reshape inner Melbourne

A Malaysian property giant has laid out a massive nine-figure sum for a vacant Carlton block, and experts believe more Asian capital is on its way.

Ocean views for a fraction of the cost of vacant land in the city

Vacant lots with ocean views start from $495,000 in this tourist town - a fraction of the cost of an average patch of dirt in Sydney or Brisbane. Find out where and see the house designs.