First home or investment property: Which is better for buyers?

House prices are rising at the fastest rate since the late 1980s. But it might only be the first stage of the rocket that is the nation’s property boom.

When the pandemic first arrived on our shores back in March last year, the mood within the property market rapidly deteriorated.

In just weeks, a bullish market had been flipped on its head, with widespread reports of properties being sold for significantly below asking prices.

Then came the predictions of big losses for property owners, as housing analysts and the banks fired off forecasts of up to 32 per cent price falls in quick succession.

Now as we look back at those market conditions through the lens of prices rising at the fastest rate since the late 1980s, March 2020 seems like a completely different world.

Since the start of the year, property prices in the nation’s five largest capital cities have risen by a whopping 9.5 per cent, with Sydney leading the way with prices rising by 11.9 per cent.

RELATED: ‘56% increase’: Scary mortgage prediction

For the 66 per cent of households who own their home outright or have a mortgage, this has resulted in arguably the largest boost to household net wealth in such a short period of time in Australian history.

But as some of these lucky Australians enjoy their large capital gains, for those who don’t own their own home, things are quite a bit different.

According to a report from Domain, potential homebuyers have seen the required size of home deposits skyrocket since the start of the year.

“Anyone in Sydney who had saved a 20 per cent deposit on the median house price in December but did not manage to buy a home needs to have saved an extra $20,614 since then (to March 31st) to keep their deposit at 20 per cent of the current median house price.”

While Sydney is certainly an outlier, between January 1 and March 31, the required deposit (20 per cent) to buy a median house rose by $9706.

It’s important to keep in mind that these required savings actually get prospective home buyers no closer to their dream of property ownership than they were before. Instead, they merely maintain the purchasing power their deposits had previously before prices took off.

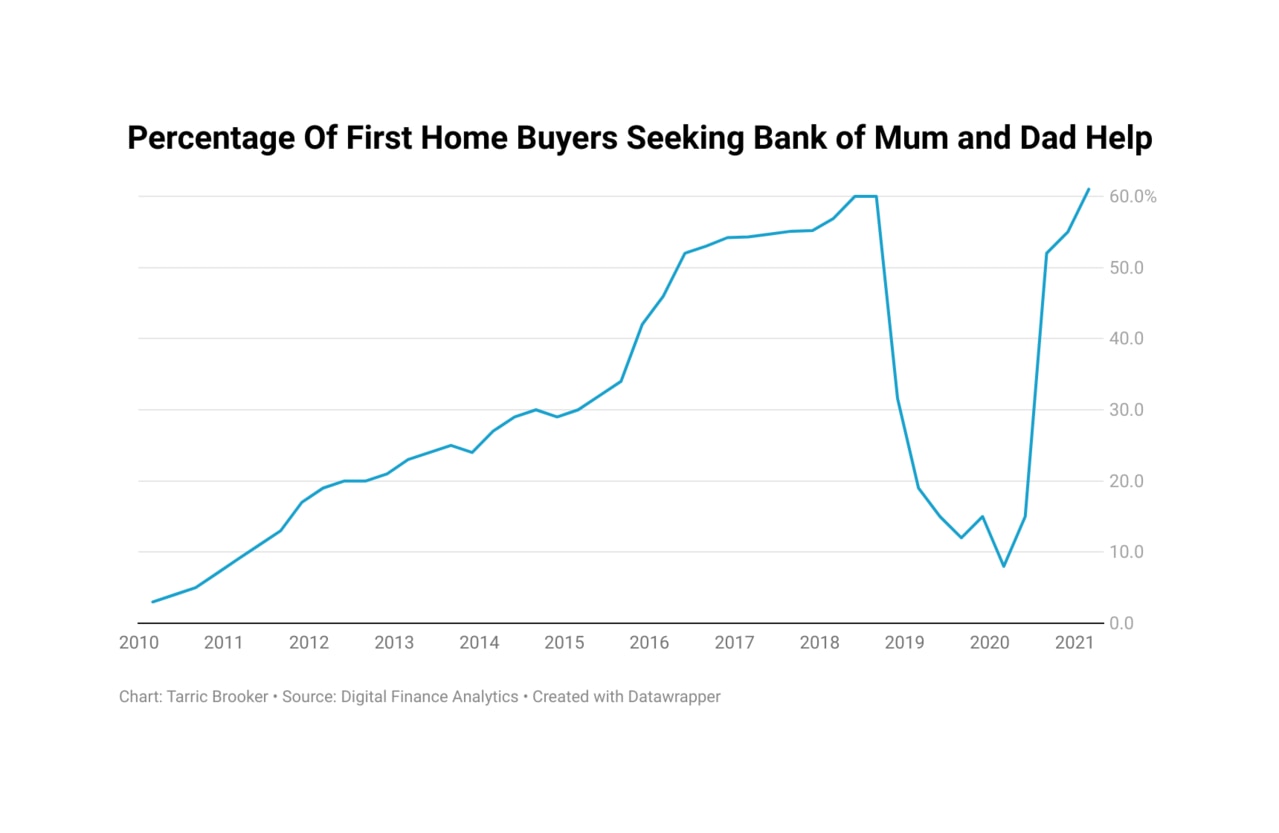

As prices continued to get away from prospective first homebuyers, many looked to their parents for help getting into the market.

According to figures from research firm Digital Finance Analytics (DFA), the number of first home buyers seeking help from their parents rose from 8 per cent in the first quarter of last year, to more than 60 per cent by March 2021.

RELATED: Aussies facing huge house price rise

The average assistance being provided isn’t exactly just parents providing a bit of a top up to their adult children’s deposit either.

As of March, the average amount of assistance parents were providing their first homebuyer children for their deposits was almost $90,000.

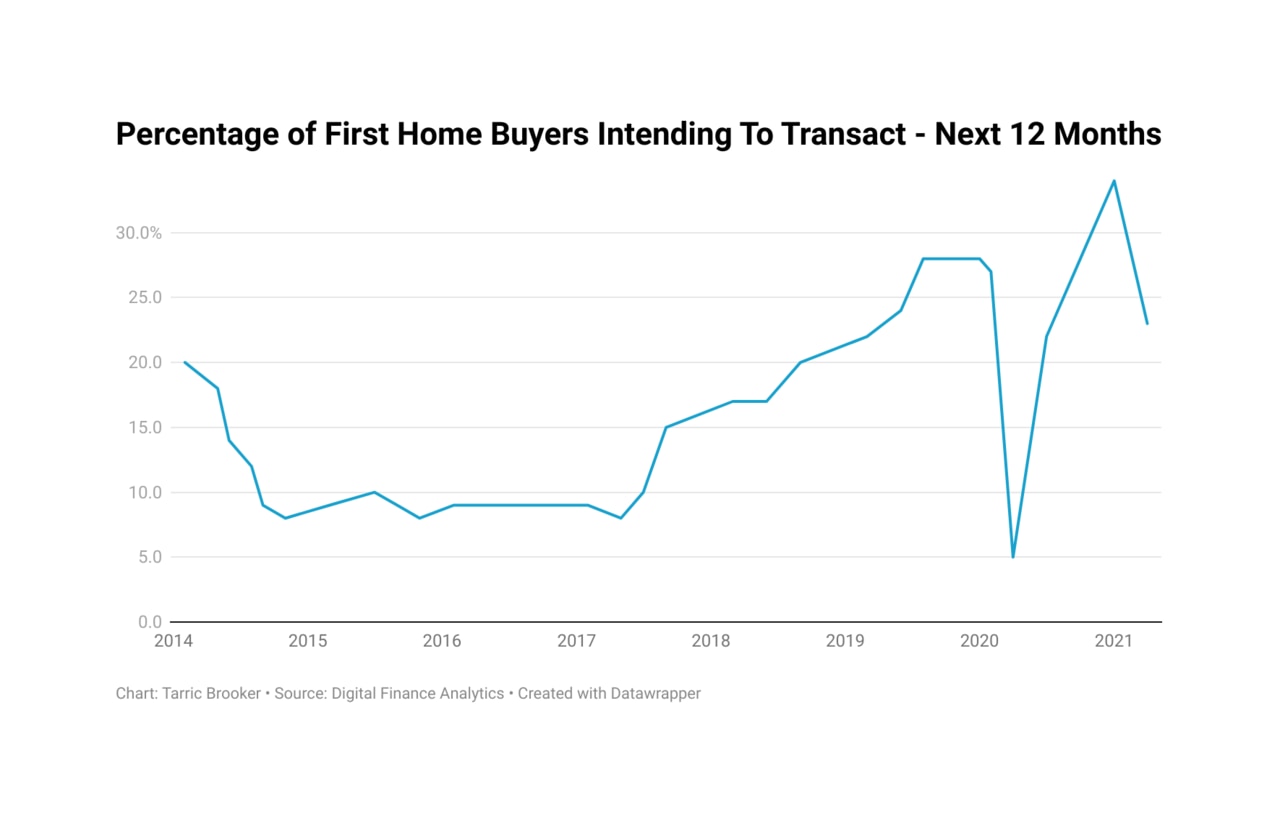

Despite a relatively strong increase in prices up until the end of the last year, first home buyers were generally undeterred by this additional hurdle to get into the market.

Figures from DFA show that a record high 34 per cent of prospective first home buyers were looking to get into the market in the next 12 months at the start of this year.

This has since fallen to 23 per cent in the largest one month non-Covid related move in the index since records began in 2013.

RELATED: Key to buying in a housing boom

With deposit requirements setting off for the stratosphere and prices rocketing out of the reach of many prospective first home buyers, it’s perhaps unsurprising that so many have chosen to give up on trying to buy a home, at least for now.

In decades long past, this may have started to put the brakes on a housing boom, as prospective buyers leave the market and price growth begins to slow down as a result.

In the United States, rising prices have already resulted in the single largest monthly drop in home buying intentions in the 54 years records have been kept.

But like the theme of so many finance industry presentations and backyard BBQ conversations, Australia really is different.

Through the forces of negative gearing and a growing perception that the government will not allow prices to fall significantly, we may be seeing only the first stage of the rocket that is the nation’s current property price boom.

In the words of property research company SQM Research’s managing director Louis Christopher:

“They [the federal government] will never let a housing crash happen in this country.”

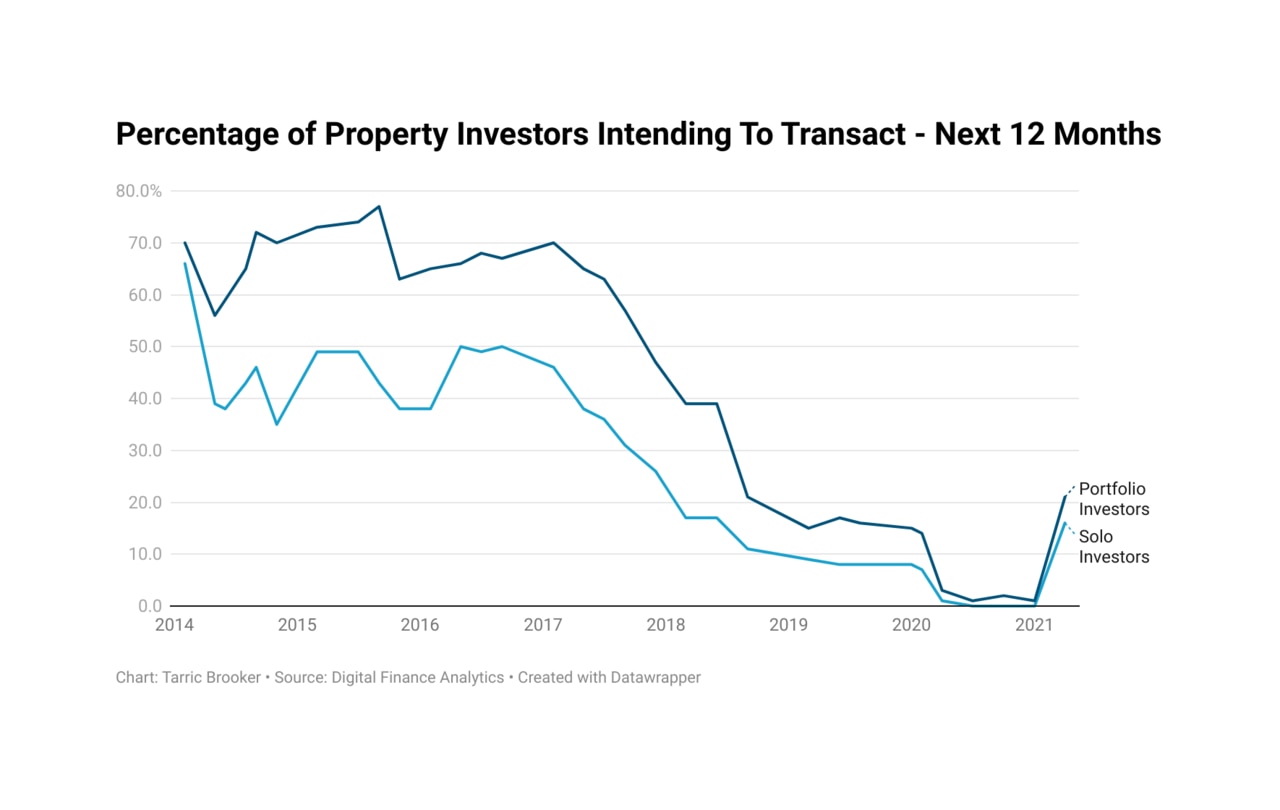

As the number of first home buyers priced out of the market continues to rise, the capital gains potentially on offer has seen the number of investors looking to get into the market or buy more properties has set off like a rocket.

When surveyed in January, few property investors were looking to transact, with just 1 per cent of those DFA defines as “portfolio investors” stating they intended to buy in the next 12 months.

By the time April came around, the situation had been completely transformed by the hottest property market since the late 1980s.

In April, 16 per cent of solo investors and 21 per cent of portfolio were now suddenly looking to get into the market.

RELATED: Property advice young Aussies are ignoring

To put these figures into perspective without the distortions from the pandemic, in February 2020 just 7 per cent of solo investors and 14 per cent of portfolio investors were intending to buy a property in the next 12 months.

While rocketing prices are disastrous for first home buyers who increasingly find themselves priced out of the market in greater and greater numbers, for property investors, rising prices are having completely the opposite effect.

Rising prices are an incentive to get into the market, to take advantage of what they hope will be yet another long-term period of very strong housing price growth.

Where the housing market will find itself in the long term is anyone’s guess, as concerning signs of weakness begin to emerge in the global economic recovery.

But in the short term, there are two things we know with relative certainty.

Investors will likely once again get into the market to chase capital growth, in what is perceived as the nation’s safest asset, and first home buyers will continue to be priced out of the market.

Tarric Brooker is a freelance journalist and social commentator | @AvidCommentator

Roosters star’s $2.5m pre-marriage play

Sydney Roosters star Angus Crichton is rolling the dice on a $2.5m play ahead of his marriage to Chloe Esegbona next month.

‘Gone straight away’: all cashed up and nowhere to buy

Interstate migrants may find housing markets a shock when they cross borders, with record price levels beginning to lock out even cashed up buyers.

Inside creepy abandoned 400yo estate

A historic mansion has been given a new lease of life after being left abandoned and rotting for decades.