How will Australia fare in the global recession?

The world is in recession but what does this mean for Australia? Two big money mistakes have just been exposed.

ANALYSIS

That there is a global recession coming is no longer news. Typically, any growth under 2 per cent for the global economy is considered recessionary. Various nowcasting models already have us materially below that level.

The great post-Covid economic unwind is emanating from three main sources.

Energy shock

Europe is caught in a stagflationary energy shock. The unbelievable rises in electricity costs landing on Europe from restricted gas imports from Russia is simultaneously causing industry to reduce output, and tempting governments to keep spending amid very high inflation.

This nasty cocktail means the ECB is being forced to raise interest rates fast even as the economy craters.

Inflation and rate shock

The US economy has already had its inflation shock and is now slowing thanks to tearaway interest rate hikes that are crashing bond, equity and property markets all at once.

Covid-zero shock

China is barely growing as it wrestles with a zero-Covid policy that is inhibiting services activity and a property crash that is taking on historic dimensions.

Moreover, falling demand from the US and Europe is about to run upstream through global supply chains and land in China as a trade shock.

Of the three, the US is clearly better off. It is much closer to energy independence, and does not have a deflating housing bubble like China.

In fact, there is no clear economic imbalance in the US to adjust. Meaning it is unlikely to have any kind of systemic financial shock to make matters worse.

But the same cannot be said of China and Europe.

Chinese property is a $64 trillion market. The bust is not so much in prices as it is in construction volumes but that is still going to land on its banking system in due course.

Normally, any nation would be cutting interest rates furiously to stabilise the property market.

But China cannot because if it does then it might create another problem. The yuan is already crashing and if it drops far enough it will become a self-fulfilling prophecy of fleeing capital that lifts interest rates.

Europe, too, has its share of high-risk financial accidents. The new UK government has embarked on an experiment in what used to be called “voodoo economics”. That is, it is cutting taxes directly into very high inflation and a huge external deficit. Markets are already spooked and as the next chart shows, the pound has crashed to record lows.

If the tax cuts do not add much to demand but trash the budget deficit, which is the base case, then it is not beyond the realms of possibility that the UK will need an IMF bailout!

Then there is Italy, which has just elected a Neo-Fascist government to take on the EU. The range of possibilities here is scary too, from Italian bond defaults to the rupturing of support for the Ukraine War if energy prices do not come down.

The Lucky Country

So, where is the Lucky Country in all of this?

We should be sitting pretty. Our inflation crisis is smaller and would normally fade quickly. Despite big falls in some commodity prices, with more to come, our energy exports are booming and the falling currency is delivering even more income.

All things equal, we’d perhaps be facing a slowdown but probably avoid a recession.

However, we’ve rather cocked it up. The new Albanese government is delivering a double policy blow that means it is likely we will experience a recession.

The first mistake is the government’s refusal to confront the energy cartels that are bringing Europe’s energy shock back home to Australia. This can be easily fixed with domestic reservation of coal and gas at cheap prices, or an export levy applied to the same.

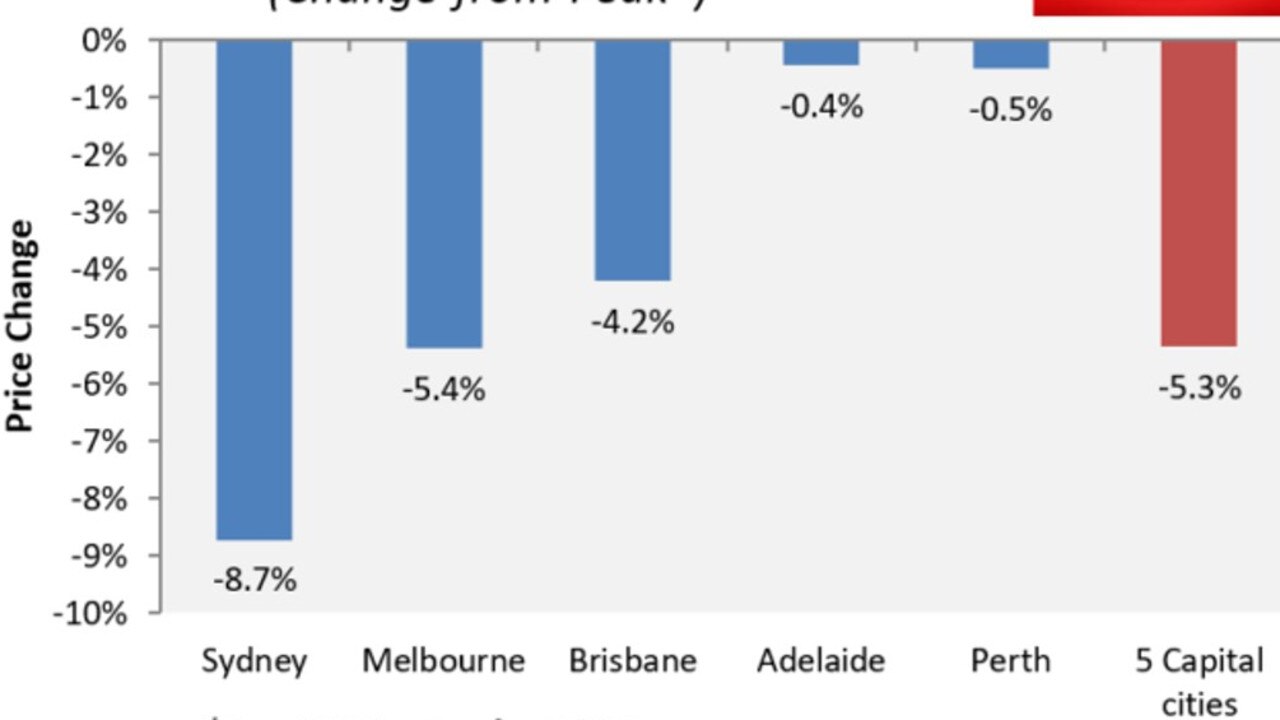

The failure to do so will add 5 per cent to our CPI over two years. This is crashing real incomes, and is a key reason why the RBA is hiking interest rates so fast which is, in turn, pulverising the property market.

Consumption will assuredly follow and where it goes, growth follows.

The second reason is that the Albanese government has restored mass immigration at the worst possible moment. Concerned about today’s tight labour market, the government has failed to see that next year it will naturally loosen amid the global recession.

A flood of cheap labour supply will cut the nascent wages rebound off at the knees, prolonging the real income shock.

Of course, it will also add some demand to the economy thus making it less likely that we’ll see a headline fall in GDP. But that should be little comfort for Australians themselves.

In per capita terms, a recession becomes more likely as each Australian shares national production among a larger number of people. It is the per capita measure that matters to individual standards of living.

What’s good for Canberra these days is rarely good for the rest of us.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geopolitics and economics portal. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review. MB Fund is underweight Australian iron ore miners.

ASX drops on banks and miners

Falling iron ore prices and profit taking on the major banks drove the ASX lower on Friday for the third straight trading day.

Warning ‘nervous’ RBA could hold rates

The Reserve Bank’s monetary policy board “clearly remains nervous about inflation”, with a major bank warning a rate cut is not a lock in August.

Plan to make Aussie workers $14k better off

Changing company taxes, making it easier for Australians to upskill or change roles and embracing new technology are just a few of the ways we can all be better off, a new report finds.