Station masters join forces to save Ten Network

TEN Network’s ballooning debt would be paid off under a rescue plan being considered by two of its billionaire shareholders.

Business

Don't miss out on the headlines from Business. Followed categories will be added to My News.

TEN Network’s ballooning debt would be paid off under a rescue plan being considered by two of its billionaire shareholders.

And the broadcaster’s loan guarantee would be removed over an “appropriate period”, ensuring it has time to find its feet in an increasingly competitive television market.

Rita Panahi: Poor programming to blame for Channel Ten woes

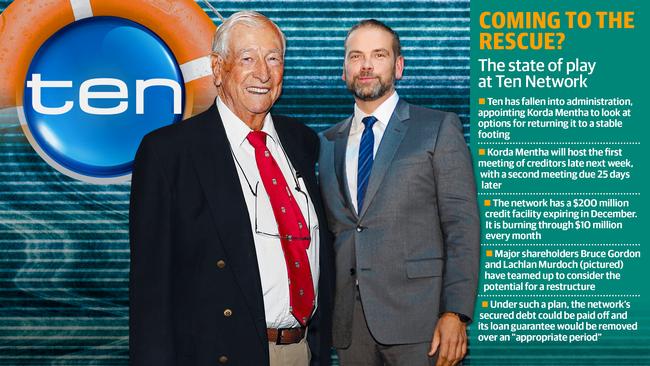

TEN NETWORK FALLS INTO ADMINISTRATION

TEN SHOWS NEED FOR MEDIA REFORM: FIFIELD

The battle plan is proposed in documents lodged with the Australian Securities Exchange by Lachlan Murdoch and Bruce Gordon, the owner of regional broadcaster Win Corporation. The duo appear poised to throw Ten a lifeline after it tumbled into administration yesterday.

Mr Murdoch and Mr Gordon, who control a combined 22 per cent of Ten, have teamed up to explore a restructure. The papers lodged at the stock exchange reveal the pair’s investment companies have agreed to “work together exclusively” on a restructure proposal.

Mr Murdoch holds a 7.7 per cent stake in Ten through his investment vehicle, Illyria; Mr Gordon’s 15 per cent is through his equivalent firm, Birketu.

The documents acknowledge the potential for deep losses if Ten were to collapse.

James Packer, Mr Gordon and Mr Murdoch, the co-chair of Herald Sun publisher News Corp, guarantee a $200 million debt facility Ten has with the Commonwealth Bank that is due to expire in December.

“In the event of a default by Ten ... there is a risk of Birketu and Illyria each being exposed to significant liability under their respective guarantees together with a complete loss of their respective investments in Ten’s equity,” the papers say.

They say it “may be in the parties’ respective commercial interest” to consider a restructure where Ten’s secured debt was repaid and its loan guarantee was eventually removed.

Ten fell into administration yesterday only days after the trio of key backers elected not to guarantee a new $250 million loan. Korda Mentha has been appointed administrator and says it will work closely with management, employees, suppliers and content partners.

“During this period, the administrators intend to continue operations as much as possible on a business as usual basis,” Ten said in a statement.

The first meeting of creditors will be held at the end of next week, with a date announced today or tomorrow. A committee representing those owed cash will be formed at the meeting.

While Ten had only drawn down $45.5 million from the $200 million credit facility at the end of its first half — as of February 28 — it is now ploughing through an extra $10 million a month.

Korda Mentha will table its first report on the group’s prospects at the second meeting of creditors, 25 days after the first meeting.

While options include putting the network into liquidation, insiders say the likely scenario is Ten and its creditors agree to a so-called deed of company arrangement. That would clear the way for a recapitalisation or sale.

Korda Mentha will also lobby federal politicians to pass the government’s media reform bill through the Senate, Business Daily believes.

That would mean the rule barring a company from owning a newspaper, TV station and radio station in a single market was axed. The proposal has met opposition from Labor and The Greens despite the rise of international rivals such as Netflix and Amazon Prime.

How the NBN has delivered just in time

The NBN has delivered, and it has done so in what can only be described as the ultimate — the hit-the-ground running immediate — stress test, rites Terry McCrann.

Sydney airport the wrong place at the wrong time

Sydney Airport has some of the sweetest acreage in Australia but when passengers numbers have dwindled from 9 million in the March quarter to 400,000 in the June quarter, that doesn’t count for much, writes Terry McCrann.