$124m collapse of Remi Capital described as ‘catastrophic’ by the liquidator

More than 300 investors around Australia and the world are likely to get less than 10 per cent of their money back after they tipped in between $50k and $5m.

Companies

Don't miss out on the headlines from Companies. Followed categories will be added to My News.

More than 300 investors impacted by the collapse of an Australian investment firm may have claims worth an estimated $126 million against the company’s directors if it is put into liquidation, a creditor’s report filed with ASIC has revealed.

The company called Remi Capital may have been insolvent since its launch in 2018 and had no income generating assets, according to the report, despite promising “mum and dad” investors big returns.

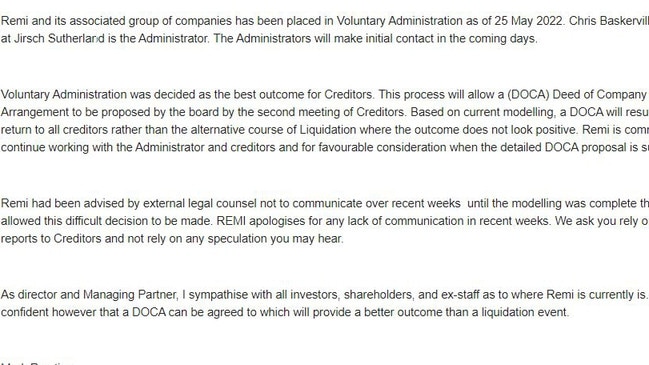

Remi Capital was placed into voluntary administration on May 25, with Chris Baskerville from specialist insolvency firm Jirsch Sutherland appointed as administrator.

The most recent creditor’s report detailed outstanding debts from the company amounting to $124 million.

Preliminary investigations outlined in the report showed creditors may have claims worth $123 million for insolvent trading, over $700,000 for “unfair preference payments” and $2.2 million for “unreasonable director-related transactions”.

“It would be very unrealistic for a liquidator to collect $123 million in insolvency trading claims from two directors but I think that’s the value we are likely to have,” Mr Baskerville told news.com.au.

“It should be noted in my report there were no real property assets in the name of (Remi’s directors) Peter Terrill or Mark Prestige that we could identify directly in their name, so in other words these men appear to be men of straw.

“But that doesn’t mean they don’t have assets, its just not in their direct name.”

Stream more business news live & on demand with Flash. 25+ news channels in 1 place. New to Flash? Try 1 month free. Offer ends 31 October, 2022 >

The company and its investors

Peter Terrill founded the company, which is formerly known as C2 Capital, in 2018.

But he left the organisation “by an exit deed” at the start of March 2021 after “unrest from investors and staff”, the report said.

In July 2021, a number of the companies went through a formal name change and rebranding to Remi.

“This shift in branding was as a result of poor public perception of the C2 brand following a number of news articles published about the group and its former director, Mr Peter Terrill,” the report said.

Remi Capital’s parent company was put into liquidation by court order on June 9, but there are 11 companies within the group.

The report revealed that $141.8 million had been invested into the companies during their five years of operation, with $61.2 million still owed to 312 creditors.

There were 158 investors from Victoria, 77 from Queensland and 25 from NSW, as well as five overseas investors from Japan, New Zealand and South Africa.

One of the 312 investors impacted was a Melbourne dad of two, who had been left “shocked” and “heartbroken” after the Remi Capital collapse left $300,000 owed to his family.

The report outlined a number of different possibilities in terms of the amount of money investors may get back, but Mr Baskerville told news.com.au it was likely to be a less than 10 per cent return on average.

“We think the bulk of investors are mum and dads and (people with) self managed super funds and the minimum investment had to be $50,000,” Mr Baskerville previously told news.com.au.

“I think every one of those investors had to sign up to say that they were a sophisticated investor, so to get sophisticated investor status the regulations say you have to have a net income of around $250,000 or net assets of over $2 million.

“We do believe that there are a handful of investors that put in potentially around $1 million and $5 million, but that’s not the majority.

“We think that’s a reflection of a small minority of (investors) but it looks like high net wealth investors have put their money into the scheme.”

Losses spanned years

The creditor’s report found that all companies under Remi Capital Pty Ltd “suffered trading losses in each financial year analysed” except for one, with Mr Baskerville describing the situation as “catastrophic” to news.com.au.

The report added there was one company that reported profit in the 2021/22 financial year, although it derived 93 per cent of its income from inter-company income and state government Covid-19 hardship grants.

It also showed that the parent company has haemorrhaged money in the past four years.

Remi Capital, which is currently in liquidation, recorded a loss of $710,000 for the 2019 financial year and $2.34 million for the 2020 financial year.

This jumped to $4.82 million for the 2021 financial year and $4.44 million for the current financial year, showed the report.

“Based on the information available, the majority of the funds received from investors has been utilised to pay related party loans, operating expenses, salaries and payroll tax liabilities and interest expenses,” the report said in regards to Remi Capital Pty Ltd.

At the time of the administrator’s being appointed, there were five employees left with Remi, a huge drop from the 54 it had at one stage.

Yet, staff are owed a whopping $1.3 million from three of the companies for wages, superannuation, annual leave and redundancy.

The parent company Remi Capital owes its former employees the largest amount with $696,650.

Transactions under the failed companies

Mr Baskerville outlined that Jirsh Sutherland was investigating a series of transactions and deals leading up to the failure of the firm, the report said.

This included a number of property transactions that lead to losses for the company.

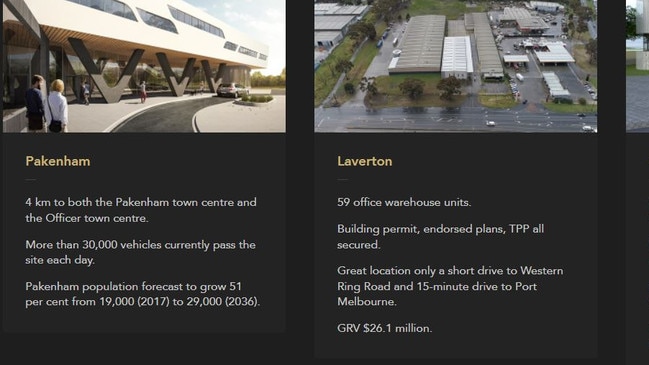

A property in Laverton North in Melbourne was purchased with money raised from investors for $11.05 million in December 2019 and was later sold in March 2021 for $8.5 million — a whopping loss of $2.55 million.

Another property located in Pakenham was bought in July 2018 for the purchase price of $6.5 million and later sold in April 2021 for $5.8 million, resulting in a loss of $700,000.

Another property was purchased by the companies in October 2019 for $9 million, but despite a report valuing it at $15 million, a sales campaign run in the months prior to the administrator’s appointment “resulted in a highest bid significantly lower” than $15 million, the creditor’s report revealed.

It also outlined preliminary investigations into unfair loans, which are “loans made to the company at any time prior to the date of our appointment, which have extortionate interest, or charges,” the report said.

“Based on our investigations to date, it is possible there are a number of potential claims

and our investigations are ongoing,” it added.

‘No longer licenced to provide the financial services’

Remi Capital had acquired a financial services licence in September 2019 from a company called Murphy Financial Solutions, which was renamed Remi Financial Services, one of the eleven companies under the group.

Then in March this year, Remi Financial Services was sold for $70,000 and renamed PLC Investment Services.

But the report said PLC Investment Services had not paid the full amount of the agreed sale price with $20,000 outstanding, due to claims that certain aspects of the agreement were not upheld by Remi Capital.

“The significance of this transfer is such that Remi Investment Services held the group’s Australian Financial Services Licence, as an Authorised Representative, used to promote their products and as such, from the date of the transfer, the companies were no longer licenced to provide the financial services specified in the license conditions,” the report added.

Investigations into the directors

The creditor’s report has listed Mr Terrill as the director of 14 other companies, including some that were part of the group that came under Remi Capital.

It appears that Remi’s founder and former director Peter Terrill may have set up a new business, called Zash Ventures, with the same methods of attracting investors as were used with Remi Capital, Mr Baskerville told news.com.au.

Of the other companies for which Mr Terrill was a director, one was in liquidation already and four others were related to Remi Capital, which was likely to be a “100 per cent shareholder of those entities”, Mr Baskerville said.

“We will enforces the rights over them as a shareholder and it could mean winding up those companies,” he told news.com.au.

Jirsh Sutherland also revealed it had lodged reports with ASIC reporting alleged offences committed by the director for each of the companies relating to failure to exercise due care and diligence, misuse of position, reckless or intentional dishonesty in failing to exercise duties in good faith or for proper purpose and insolvent trading.

News.com.au has reached out to Mr Terrill for comment but he did not respond.

Mr Prestige told news.com.au that he could not comment in time for publication.

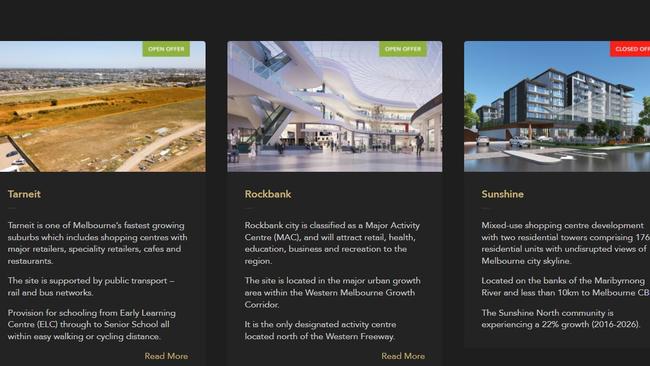

But he previously told a creditors meeting in a statement that after taking over from Mr Terrill he had succeeded in significantly reducing cash-burn, brought tax and financial reporting obligations up to date, reduced staff from 54 to 17 and had a planned exit from projects that were not aligned with the capabilities of Remi.

He added a new strategy had been developed with a focus on regional acquisitions that were more in line with the group’s capabilities and he had secured funding for the property projects in Rockbank and Tarneit through a preferred funder.

The report to creditor’s revealed that there was an estimated total insolvent trading claim of $123 million, although news.com.au is not suggesting that either director could be sued for that amount alone.

The report to creditor’s expressed a preliminary position that the companies had been trading while insolvent, potentially since inception and remained insolvent at all times up to the appointment of administrators.

The report also noted that the current and former directors had not been given an opportunity to present a defence to any insolvent trading claim.

News.com.au does not suggest the claims made by the administrators as part of the preliminary investigations into Remi Capital have been proven.

Originally published as $124m collapse of Remi Capital described as ‘catastrophic’ by the liquidator

Wild reason 18yo pastry king’s page vanished

A teenage pastry sensation has been left feeling “helpless” after his business’ account was banned while studying his HSC.

Dogs and cats cleared for takeoff on Virgin flights

The airline has cleared the final regulatory hurdle to allow beloved pets in cabins, which will be an Australian first for commercial passengers.