Billionaire Sam Bankman-Fried’s net worth vanishes after FTX and Alameda disaster

Sam Bankman-Fried, a 30-year-old crypto billionaire, has lost nearly his entire fortune and his empire is on the brink of collapse.

Companies

Don't miss out on the headlines from Companies. Followed categories will be added to My News.

Crypto wunderkind Sam Bankman-Fried’s net worth was $24.2 billion ($US15.6 billion) on Monday night when he went to bed. By the next day, his fortune was gutted by 94 per cent.

One of the richest people in the world, the 30-year-old, known as SBF, is now only worth $1.5 billion ($US1 billion) after suffering the biggest single-day collapse of a billionaire’s net worth in recent history. (Last year Elon Musk’s net worth plunged $US50 billion in two days but he remained the world’s richest person).

The bulk of SBF’s fortune was tied up in the cryptocurrency exchange he founded FTX, as well as his quantitative crypto trading firm Alameda Research.

The billionaire’s holdings of FTX were worth about $9.6 billion ($US6.2 billion) and $11.5 billion ($US7.4 billion) was tied up in Alameda.

Stream more business news live & on demand with Flash. 25+ news channels in 1 place. New to Flash? Try 1 month free. Offer available for a limited time only >

For weeks, there were rumours that FTX and Alameda were in trouble. Coindesk revealed that Alameda’s $22.7 billion ($US14.6 billion) balance sheet was full of the FTT token, a coin invented by FTX.

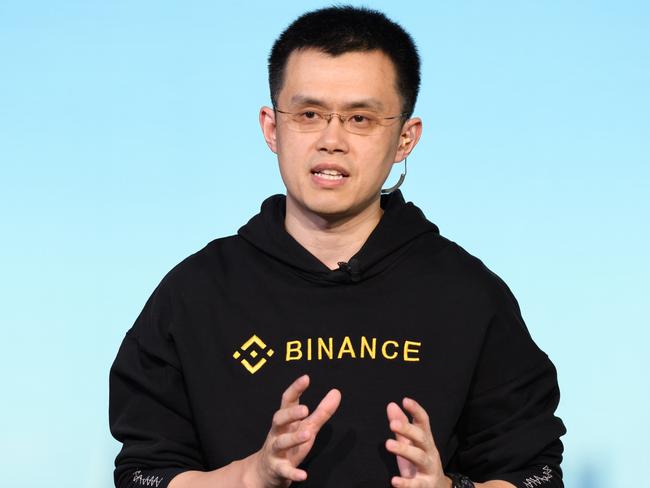

And throughout that, SBF had been involved in a public standoff with Changpeng “CZ” Zhao, the chief executive of Binance, a major crypto exchange. They had been trading barbs for months.

Then came the collapse. A year ago, FTT was worth $91.50. This morning it was selling for just $4.21.

Shockwaves sent through the crypto world

On November 7, CZ announced his firm was liquidating its FTT holdings, giving weight to rumours about the financial wellbeing of Alameda and FTX. He cited “recent revelations that have come to light” and said it was not a “move against a competitor”.

As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash (BUSD and FTT). Due to recent revelations that have came to light, we have decided to liquidate any remaining FTT on our books. 1/4

— CZ 🔶 Binance (@cz_binance) November 6, 2022

FTX then revealed it was suffering “liquidity” problems, an announcement that shocked the crypto world. SBF revealed that Binance may save FTX from insolvency.

SBF had phoned CZ, urgently requesting help – he needed emergency funding due to customer withdrawals in recent days. The requests had sparked a liquidity squeeze.

And at first it seemed like Binance would be the white knight.

“Things have come full circle, and FTX.com’s first, and last, investors are the same: We have come to an agreement on a strategic transaction with Binance for FTX.com (pending DD etc.) [due diligence],” SBF wrote on Twitter on Tuesday.

“Our teams are working on clearing out the withdrawal backlog as is. This will clear out liquidity crunches; all assets will be covered 1:1. This is one of the main reasons we’ve asked Binance to come in. It may take a bit to settle etc. We apologise for that.”

He thanked CZ for doing an “incredible job of building out the global crypto ecosystem” and tried to dispel “rumours in media of conflict” between the exchanges.

But the proposed deal broke down today. And to rub salt into FTX’s wounds, it was revealed that the US Securities and Exchange Commission is looking into whether the platform mishandled customer funds as well as the firm’s relationship to other companies. The Commodity Futures Trading Commission is also probing FTX.

Meanwhile, concerns remain about the order of events leading to FTX’s current woes.

CNBC reporter Ryan Browne wrote: “So just to be clear … Binance’s CEO raises doubts over the financial health of Alameda/FTX, thus causing investor panic around FTX leading a tonne of investors to move their funds out, only to then … buy the company outright?”

CZ publicly shared a letter he sent the Binance team, stating he “did not master plan this or anything related to it”.

“It was less than 24 hours ago that SBF called me. And before that, I had very little knowledge of the internal state of things at FTX. I could do some mental calculations with our revenues to guess theirs, but it would never be accurate. I was surprised when he wanted to talk. My first reaction was, he wants to do an OTC deal … but here we are.”

Binance revealed at 8am today it would not go through with the deal.

“As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of [FTX],” Binance wrote on Twitter.

CZ later followed up by writing: “Sad day. Tried, but [crying emoji].”

The future doesn’t look bright for FTX. SBF told investors today that the company needs $6.2 billion ($US4 billion) to remain solvent and is facing a shortfall of $12.4 billion ($US8 billion).

The company is urgently seeking financing in the form of debt, equity or a combination of both.

‘I f***ed up,” SBF reportedly told investors on the call.

More Coverage

Originally published as Billionaire Sam Bankman-Fried’s net worth vanishes after FTX and Alameda disaster

Is Trump driving US tourism off a cliff?

Flight Centre has blamed US policy changes for wiping up to $105m from its full-year profits. So is Donald Trump changing the way we travel?

‘Locked in’: Major bank’s big rate cut call

Households will get a rate cut in May regardless of April’s inflation reading, one major bank’s chief economist has boldly declared.